Councillor Dave Ward returns from Kosovo with lessons in development finance. He argues that allowing the land and development supply chain to share in the upside of apartment sales can lower the barriers to entry for smaller housebuilders.

I have just returned from Pristina, Kosovo where I got my new apartment ready for a summer rental to a couple of German students who are volunteering there for the summer and needed a place to stay.

As Chair of Planning at the London Borough of Merton, I am always interested in housing and planning policy, particularly around building new homes and it was very interesting to see and learn about the differences between the UK, specifically London, and Pristina.

Firstly, the scale is a lot smaller, Pristina is a city of nearly 150,000 people, just over eight per cent of the total 1.8 million population of Kosovo, and growing. This quite closely compares with London’s 7m people, roughly 10% of the total population of the UK.

So both cities are the centres of government, the financial sector, the media and the headquarters of many national and international businesses and other organisations. As in London this attracts a higher population as people come to the capital for work, which then leads to housing pressures.

Pristina is in the middle of a housebuilding boom. The block where I now live (for some of the year) is ten storeys, with roughly 60 apartments varying in size from small studios to three-bed apartments. It is one of at least eight similar blocks, either completed or under construction, just within a few hundred metres, in an attractive location just ten minutes walk from the city centre.

The most interesting thing I discovered about housebuilding in Pristina is they way it is financed which is very different from the UK. Typically a developer will find some land upon which a block could be built, purchase it from the original landowner, pay contractors to build the block, and suppliers for the materials, then when it is complete, sell or rent the homes and try to make a profit, just like here.

The difference is that the original landowner, contractors and suppliers are often paid, at the end of the project, in completed properties.

For example, the company which supplies the concrete struts which form the frame of the building might, instead of cash, upon completion of the project receive a floor, 6 or 8 properties which they can sell, keep or rent as they wish. The same for the building contractors, glaziers and anyone else involved in the project.

I was surprised at this and wanted to know more so, as I was due to meet the owner of the company which built the block I live in, I asked him about it.

His company usually funds around half of the construction costs of a new development in this way. It is kind of a loan, without interest, but it is more expensive. He estimates that building a new block of apartments would be 5 to 10 per cent cheaper if paid up-front in cash. This is a compensation for the contractors, for instance a building firm. They need to pay their workers, purchase the materials and do their work, paying up-front, on the promise of a number of properties upon completion, not knowing for certain what they will be worth at that stage. They are taking much of the risk, and therefore take a higher return.

This model is used widely in Kosovo and has been borrowed from nearby Turkey where this has been the norm for development for some time.

The practical implications of this are that housebuilding is slightly more expensive, but easier to do for those without huge amounts of up-front capital. So building is not dominated by large developers funded by the major banks or the very wealthy. A relatively small company, such as the family firm which built my block, can get into the housebuilding business and deliver new homes from very small beginnings.

Property prices and rental values in Pristina are, like London, higher than the rest of the country. They are much lower than London in actual terms, but also lower in relative terms compared to average income, wages and cost of living in Pristina. Housing is genuinely affordable for those on modest or low incomes.

To rent an apartment like mine – 2 bedrooms in the centre of town – a single person would need a salary around the middle range in Pristina. A couple sharing would find it more affordable. This is for a sought-after area near the centre of town. Move a few miles out, a bus ride from the centre and rents and prices become comfortably affordable for the lower paid.

Could this be replicated in full or in part in the UK? Could we open up housebuilding to smaller entrepreneurs, to housing associations, non-profit organisations, and to Local Authorities to build new housing, without the need for huge amounts of capital up front?

I think it is worth looking into.

Dave Ward

Dave is a Labour Councillor in the London Borough of Merton where he is Chair of the Planning Committee. He represents the ward of Colliers Wood.

Since 72 people lost their lives in the Grenfell tragedy on 14 June 2017, the cladding and building safety crisis has spiralled. Estimates vary as to how many households are affected. The End Our Cladding Scandal (EOCS) campaign believes that up to 11 million people are now caught up in the scandal. Luxury flats and social housing alike are affected. This article examines the impact of the cladding and building safety crisis on shared owners, and asks whether it lays bare fundamental flaws in the shared ownership model.

June 5th saw a National Day of Developer Protests outside new home sales offices, organised by local campaigners and supported by the national End Our Cladding Scandal (EOCS) campaign. The protests will be followed next month by a Leaseholders Together rally – planned in collaboration with the National Leasehold Campaign (NLC).

How long will it be before the spotlight shifts from developers to housing associations? How long before mass protests are taking place outside housing association offices and first-time buyer events?

What has gone so wrong that shared owners who placed trust in the promise of ‘affordable homes’ now face crippling bills? What are housing associations doing to support shared owners facing life-changing building safety remediation costs? Is it enough? What lessons may be learned, and what more can be done immediately to help shared owners and leaseholders in dire situations?

The Affordable Homes Promise: What’s Gone Wrong?

Schrödinger’s Flat

Shared ownership has been described as ‘Schrödinger’s flat’; it is simultaneously affordable and unaffordable. Housing associations define affordability by way of contrast to short-term costs of buying outright or renting, or accessibility of a mortgage deposit and loan. But these definitions oversimplify and distort understanding by failing to specify timescales of comparison, and by conveniently overlooking financial obligations imposed by leasehold contracts – such as indexed annual rent increases – and costs not referenced in lease terms, including lease extension. A rent that is often set initially as a percentage of the unsold share of the property, typically 3%.

Shared ownership is not ‘ownership’; it is an assured tenancy. And given that shared owners are liable for 100% of all maintenance and repair costs, on top of service and administration charges, and are now expected to pay for building safety remediation works too, it is clearly not ‘shared’ either.

The National Housing Federation chirpy marketing campaigns reassure first-time buyers shared ownership doesn’t mean sharing their home with a stranger but fail to explain clearly the risks arising from 100% liability for all costs. In fact, sponsored content encourages first-time buyers to believe ‘there’s no catch’. Not true! Something that the devastating cladding scandal has brought into stark relief. Problems for shared owners are complex and inter-related, full stop. Building safety issues massively compound inherent flaws and contradictions in the shared ownership model.

Staircasing rates were already dismally low: a mere 2.3% staircased to 100% in 2018-19. (It’s worth noting that this percentage is not analysed between staircasing to 100% to achieve full ‘ownership’, and a simultaneous sale and staircasing transaction undertaken purely in order to sell – a crucial distinction). The building safety crisis means any shared owners who planned to staircase to 100% are now likely to be unable to obtain mortgages to do so.

Shared owners who are unable to staircase to 100% have no statutory rights to lease extension. All things being equal, the cost of lease extension increases year on year. Particularly once the all-important 80-year threshold has been breached. And, in the absence of lease extension, shared owners’ homes will devalue dramatically over time (a separate issue from the nil valuations arising from building safety issues).

A significant number of shared owners will be trapped in negative equity situations as a direct consequence of building safety remediation charges. Those who purchased smaller shares, say 25%, are particularly disadvantaged. The people suffering the most severe financial distress may be those who had least to lose in the first place.

Going back to that £100,000 charge Irwell Valley Homes plan to levy on their shared owners… Although details remain sketchy, the Government has proposed a loan scheme capped at £50 monthly. At £50 per month, £100,000 would take 2,000 months, or 167 years to repay. Such charges are clearly a problem not just for this unfortunate generation of first-time home buyers, but for the next couple of generations too, perpetuating inequalities patently at odds with leveling up agendas.

How are Housing Associations Supporting Shared Owners?

Credit Loans

Some housing associations have obtained authorisation from the Financial Conduct Authority (FCA) to offer interest-free credit to shared owners where recharged building safety remediation costs are unaffordable. Although loans from housing associations have the advantage of being interest-free, unlike bank loans, this option raises a number of troubling questions.

The assured tenancy nature of shared ownership renders shared owners extremely vulnerable to repossession of their home in the event of mortgage or service charge arrears. Given the risks and unavoidable costs the current shared ownership model exposes shared owners to, what confidence can they have that housing associations and lenders have their best interests at heart? Why should they believe housing associations would be flexible as life circumstances change over the potentially life-long timespan of such loans? Additionally, housing associations that have already sold off freeholds may have tied their own hands regarding their ability to assist shared owners facing possession by lenders.

Such concerns are likely to be exacerbated by proposals to sell off shared ownership portfolios to institutional investors, whose primary motivation will be to maximise returns for their own shareholders and clients, not to act in the best interests of shared owners. This not only raises disturbing questions for the future of shared ownership, but also potentially stymies meaningful attempts to fix the broken housing market.

Buyback

Maureen Corcoran – a former board member of one of the largest housing associations in England, a member of the G15, and former Head of Housing in London for the Audit Commission – suggests that: ‘housing associations that sold these properties on a shared ownership basis could buy the shares back from anyone who is struggling and unable to move’. Housing associations counter that they do not have the financial means to do so at scale. Whilst some housing associations express commitment to do so in ‘exceptional circumstances’ it’s not at all clear what would constitute exceptional circumstances.

Where policies subtract the cost of any known or estimated remediation costs from the buyback valuation there may be little benefit of shared owners pursuing buyback as a way out of an impossible situation.

Back to back staircasing (a simultaneous staircasing and sale transaction) is sometimes required due to indexed annual rent increases (RPI plus 0.5%-2%). Where such increases have resulted in rent levels becoming more expensive than local private rents – or even specified rent on local new-build shared ownership properties – the property may become unattractive in the market place. Shared owners may have no other option but to eliminate the specified rent component, regardless of the erosion of any gain by the increased selling costs arising from the staircasing transaction.

Shared owners whose building doesn’t have a satisfactory EWS1 form face additional problems. Potential buyers are not currently able to obtain a mortgage due to nil valuations. To purchase a part share buyers have to meet affordability criteria; something that is highly unlikely to be the case if they are in a position to make a cash offer. Shared owners in this situation may have no alternative to back-to-back staircasing to 100% to facilitate a cash sale on the open market.

Confirmed or potential remediation costs will drastically reduce the purchase price. This is particularly problematic for shared owners whose housing association has a policy requiring shared owners to pay over to them any difference between the valuation and the purchase price.

Subletting

Subletting is generally prohibited on shared ownership properties. This is justified by housing associations on the basis that shared ownership properties are supposed to be the primary residence of the shared owner, and not a source of profit. Such an argument erroneously conflates ‘accidental landlords’ – who may need to relocate temporarily for a variety of reasons – with commercial for-profit operators. The no-gain requirement falls away once (if) a shared owner staircases to 100%, effectively penalising shared owners who can’t afford to staircase. Or, in the case of those whose buildings are found to have safety defects, are unable to staircase due to unavailability of mortgages.

The restriction on making a gain applies only to shared owners themselves and not to housing associations, who benefit from income streams generated from shared ownership homes; nor to institutional investors eyeing up shared ownership portfolios.

When exceptional permission to sublet is given it is on a ‘no gain’ basis; with no acknowledgement of the fact that in real life it is practically impossible for landlords to plan to break-even – not least due to the unpredictable nature of shared ownership service charges (including retrospective annual adjustments). Shared owners seeking to sublet rapidly discover they have taken on all the liabilities of home ownership, with none of the financial benefits and flexibility purchasing a home usually provides.

Are Housing Associations Doing Enough?

There are clear financial challenges for housing associations in addressing the building safety crisis. But growing vocal discontent across social media and elsewhere indicates that shared owners find it hard to accept how little housing associations are doing to support them now they are facing financial ruin. More than a few shared owners now regret the mistake of trusting persuasive marketing rhetoric.

Strong sector leadership is long overdue to protect shared owners from the worst consequences of a shared ownership model that has always exposed them to unlimited risk and costs regardless of affordability claims.

The following is intended to indicate some areas where the current offering could usefully be reviewed, by no means an exhaustive list.

Shared owners report that transparency and communication on building safety and related costs is poor. This is unacceptable and should be corrected as a matter of urgency.

“We know a bill is coming… Just not when, or how much…?”

A sector-wide review of whether current provision of expert financial advice and debt counselling adequately meets identified need.

A sector-wide published commitment to clearly identified policies to support shared owners facing building safety issues, including:

Not to initiate possession proceedings for shared owners in arrears due to building safety remediation charges (including waking watch and increased insurance premiums).

To waive marriage value on lease extensions (something MTVH have already committed to), and to calculate the premium on the percentage share held (where applicable) rather than total value.

Not to charge any difference arising between the valuation and the purchase price.

Work with mortgage lenders on whatever actions are required to facilitate access to consent to let or buy to let agreements.

Work with Government to remove, or apply considerable discretion on application of, restrictive and hard to justify restrictions on subletting, including no gain requirements and time limits.

Withdraw any shared ownership properties with potential building safety issues from the market unless it may be evidenced that there are no remediation cost consequences arising for first-time buyers.

Review marketing terminology to ensure buyers have full knowledge of exposure to long-term risks and costs. This information should include – but not be restricted to – building safety and defects, and associated costs and obligations. These should be simply, transparently and adequately explained to enable informed decision-making (in compliance with Consumer Protection from Unfair Trading Regulations 2008).

Review implications of cross-subsidy model for achievement of policy aims for shared ownership (affordability, fairness and transparency), and in relation to potential conflicts of interest.

What Lessons Can Be Learned?

The building safety crisis has bought into sharp focus a number of troubling aspects of the current shared ownership model:

a vast discrepancy between expectations created by marketing strategies and real-life outcomes;

adverse consequences of a policy and research focus on access to shared ownership rather than on performance of that tenure over the long-term and the success of exit strategies in achieving foot on the housing ladder policy aspirations;

adverse consequences of a policy and research focus on financial risks, costs and benefits arising for housing associations and mortgage lenders rather than those arising for first-time buyers;

lack of ability and will of housing associations to intervene where required arising from the nature of some partnership arrangements;

failure of housing associations to solicit and sincerely take account of the concerns of long-term shared owners and campaigners;

the conflict of interests which inevitably arises from the cross-subsidy model; and

failure to fulfil fiduciary duties.

These matters should surely be of grave concern for housing association Boards of Trustees and likewise for regulators including the Regulator of Social Housing, the Charity Commission, the Advertising Standards Authority, and the Competition and Marketing Authority.

Thanks are due to Dr Audrey Verma (campaigner), Deepa Mistry (shared owner and campaigner), Dr Alison Bancroft (shared owner and campaigner), Ed Spencer (shared owner and co-founder of One Housing Residents Action Group) and Neil Goodrich (housing professional) for support in writing this article. Any errors are, of course, my responsibility and mine alone. I welcome feedback on the content.

Sue Phillips

Sue Phillips is an accountant (ACCA) who spent much of her career working in the not-for-profit sector. She is now semi-retired. She says she never expected to become a housing campaigner!

She purchased her own flat via a shared ownership scheme in 1999, staircased to 100% in 2013, and completed a lease extension in 2020.

Her own experience of shared ownership led her to start campaigning in 2019, with a particular focus on greater transparency on potential long-term costs and risks of shared ownership. She campaigns under the moniker Shared Ownership Resources.

LONDONERS ARE LANGUISHING IN TEMPORARY ACCOMMODATION HUNDREDS OF MILES AWAY – WE NEED A RETHINK.

Over the last several months London’s Labour Housing Group has been on a fact-finding mission to discover why out-of-area temporary accommodation is out of control. The findings of our latest research spells out the scale of the challenge we now face and you can read the write-ups from the Guardian or Inside Housing.

If there is one symptom of the housing crisis that brings to life its severity, it’s forcing the most vulnerable Londoners to live in homes as far as Manchester and Bradford. It’s a national scandal and only a matter of time before someone loses their life to what can only be described as social cleansing by stealth.

According to our analysis, 55,000 Londoners have been forced out of their local area because councils can no longer afford to rehouse them locally.

The number of people being rehoused outside of their local area is the highest since records began in 1998. Under Labour, one in ten people placed in temporary accommodation were placed out of their local area. Under the Conservatives that figure is closer to one in four.

Londoners in temporary accommodation are often the most marginalised. Parents with dependent children make up two-thirds of such households. A third are classified as vulnerable, with the vast majority with physical disabilities or mental ill health. The only solace we can take from the profile of families placed in temporary accommodation is that fewer victims of domestic violence, pensioners and pregnant women are placed outside their local area.

From a rudimentary mapping exercise of postcodes of two London authorities – Merton and Barking & Dagenham – it is clear that a ripple effect is taking place whereby wealthier boroughs, or where rents are higher, place their residents in neighbouring boroughs where rents are cheaper, which pushes homeless residents in those councils further out.

In what has traditionally been an issue for London and Londoners, out-of-area temporary accommodation is on track to become a nationwide problem: 92% of out-of-area placements were made by London authorities in 2015/16. That figure fell to 84% by 2020/21. If authorities outside of London continue to rehouse people outside of their local area at the same rate they are currently, within a decade they’ll be responsible for a third of all out-of-area placements.

What accounts for these developments?

Anecdotally, there is evidence that some London authorities aren’t doing enough. Councils have a statutory duty to place families as close to their local area as possible, but far too many are being sent hundreds of miles away.

Some councils have failed to forewarn the authorities that families are heading off to – making it difficult for them to access local services such as schools and doctors when they arrive. Last year Basildon Council reported that London authorities failed to forewarn the council of 58% of cases they received. The lack of communication about precisely how long an out-of-borough placements is – and it’s not uncommon for vulnerable families to be placed in temporary accommodation for over a decade – has seen young people remain in schools that they’re no longer able to travel to. One Londoner forced to live in Birmingham had to quit his job.

Other councils have been challenged in the courts – as the tragic story of Nzolameso vs Westminster City Council illustrates. Ms Nzolameso was in poor health. She had HIV, type II diabetes, depression and hypertension. She had five children between 8 and 14 years old, all of whom attended schools in Westminster. Her doctor was in Westminster and she also had a support network of friends locally who helped with her children.

When Westminster offered Ms Nzolameso accommodation over 50 miles away, she appealed. During the appeals process Westminster discharged its duty to house Ms Nzolameso and took her five children into care. The children were even separated between three different foster placements. It took a year and a verdict from the Supreme Court to change the outcome in what is clearly an extreme case but nonetheless illustrative of the human cost of the housing crisis. Too frequently it appears the wishes of tenants are not always given the consideration they deserve.

Yet the problem extends far deeper than individual authorities.

When he was Mayor of London, Boris Johnson criticised the approach taken by councils as “Kosovo-style social cleansing”. Well, the chickens have come home to roost.

There’s lots to unpack here and London’s Labour Housing Group will be doing so on Monday 7th of June at 18.00. Siobhan McDonagh MP will join panellists Jane Williams, the Chief Executive of London-based homelessness charity Magpie, newly elected London Assembly Member Sem Moema and I to discuss why we are where we are and what can be done to tackle out-of-area temporary accommodation. Ross Garrod will be hosting and it’d be remiss of me not to mention that he and fellow London Labour Housing Group member Rachel Blake have done a lot of behind the scenes work to bring our research and event to fruition.

Senior Policy Researcher in Parliament, Previously worked for the Shadow Minister for Local Government and the Local Government Association and is on the Executive of London’s Labour Housing Group.

Growing calls for 2020s to be the “decade of housing-with-care” as new task force awaits

At the end of March, more than 40 MPs, Peers, charity and private sector leaders joined forces to urge the Prime Minister to make the 2020s the “decade of housing-with-care”. The signatories to the open letter – who included Labour politicians, such as Siobhain McDonagh MP, Parliamentary colleagues from three other parties, plus household organisations like Age UK, Legal & General, the British Property Federation and Campaign to End Loneliness – said that “just as previous decades saw the expansion of the care home and home care sectors, there is now a new consensus that the 2020s need to be the decade of housing-with-care”.

Why, you might ask, should there be such widespread clamour for the growth of housing-with-care at this particular moment? At the top of the list is the urgent need to solve the UK’s social care crisis – made more pressing than ever by the Covid-19 pandemic. While finding a consensus on how social care is funded is pivotal, of equal importance is answering the question of where social care is delivered. Are we to stick with a system largely defined by two options, a care home or care at home, or are we to give older people a true choice by creating a greater variety of care settings?

There is a growing recognition that – for the social care sector – it cannot be business as usual. New ways of caring for older people are needed, which combine independent living with high-quality care and support; which not only enable older people to live longer but to live healthily for longer; which tackle the loneliness crisis by keeping older people connected with their community. As the letter’s signatories say, we need to create a “world-class system of housing-with-care that couples a focus on independence and prevention with a safety net of care services and consumer protection”, to “complement existing care options such as care homes and home care.”

It is an argument that has been gathering serious Parliamentary momentum in recent months. Alongside the open letter to the Prime Minister, MPs and Peers from four different parties, plus influential crossbencher Baroness Sally Greengross, contributed to a ‘Housing with Care Grey Paper’ in March with policy ideas to help grow the sector.

Labour politicians have been providing a strong voice on the issue, with Shadow Social Care Minister, Liz Kendall, arguing in a major speech a couple of weeks ago that we need more options inbetween a care home and care at home. The party’s former Shadow Secretary of State for Communities and Local Government, Andrew Gwynne, pressed the Government to respond to the open letter to the Prime Minister, and consider setting up a new task force to expand housing-with-care.

Why a task force? The challenge with growing housing-with-care is that it straddles multiple Government departments and so requires a new, collaborative vehicle for action. The “housing” part of housing-with-care lies with the Ministry of Housing, Communities and Local Government (MHCLG), while the “care” part stands with the Department of Health and Social Care (DHSC). A new Housing-with-Care Task Force, which Ministers are actively considering, would bring the two together to thrash out concrete policy changes so that the sector can play its full part in the social care system.

While the task force would need to decide its focus, there are a number of core policy areas that it would have to address to make the 2020s the “decade of housing-with-care”. Just as the expansion of care homes in the 1980s and 1990s and homecare in the 1990s and 2000s was largely driven by pieces of legislation and regulation specific to these sectors, we now need the same for housing-with-care.

That means properly defining housing-with-care in the planning system so it can be more easily built, providing strong consumer protection for residents moving into housing-with-care, and developing appropriate models of tenure. Ensuring the sector remains affordable for older people of all incomes is also crucial.

Some of these policy changes might sound minute, niche, even quite dry. The results will be anything but. A social care system where living a thriving, active lifestyle and receiving care don’t have to be in opposition but can be achieved together. Retirement communities which help regenerate high streets and bring people of all ages together through shared activities and services. Older people having great options to ‘right size’ and homes freed up for younger people. The list goes on.

We are on the verge of overcoming a perennial public policy challenge: getting different Government departments to talk to each other across competing priorities and bring about collaborative change. As we move closer to a cross-government Housing-with-Care Task Force, the prospect of a varied and imaginative social care system which meets the diverse needs of our ageing population is in sight.

Let’s keep up the momentum to make this a reality.

Sam Dalton

Sam is a policy and public affairs professional with expertise in housing, social care, social connection and loneliness. He works for the representative body for housing-with-care operators in the UK, ARCO, and previously led an inquiry on strengthening ties between young and old with the parliamentary group on social integration.

Sam has written for The Fabian Society and Left Foot Forward, as well as think tanks, social ventures and charities.

As the cabinet member for housing at the UK’s largest local authority, one thing I quickly learned was that it’s not simply enough to assume that a roof over someone’s head solves all their problems. Tackling homelessness is of course very high on the agenda, but the quality of accommodation and the support on offer is also key.

That’s why in Birmingham we are focussing on the exempt accommodation sector. Exempt accommodation is an unregulated type of supported housing. It is often used as a means of housing those with no other housing options, such as prison leavers and people from other vulnerable groups.

This sector has almost doubled in size in the city over the last two years, from 11,500 units to close to 20,000 and we’re seeing huge increases of exempt housing in some neighbourhoods, as private landlords build up portfolios of leased and owned accommodation, and then apply for registered provider status, exempting them from licensing regulations and local scrutiny. Over £200 million is spent on such housing in Birmingham alone.

Such accommodation can only be regulated through the Housing Benefit system and the regulatory standards for registered providers, overseen by RSH (Regulator of Social Housing) not local authorities on the ground. There is little or no regulation of care, support or supervision provided, merely an extremely vague requirement for it to be ‘more than minimal’. Lax Tory regulations means the sector is ripe for corner-cutting, exploitation and profiteering.

And, while there are many responsible and respected providers, there are also horror stories of vulnerable people being exploited and of neighbourhoods being blighted by an explosion of sub-standard accommodation.

So as a Labour Council what are we doing to fix things in Birmingham?

We’re focusing on halting the growth in exempt housing while vital oversight work can be carried out to:

Improve property standards through inspection and intervention

Improve support through increased scrutiny of claims

Gather intelligence of suspected organised criminal activity and dealing with anti-social behaviour with the police

Better scrutinising new claims for Exempt status

In Birmingham we are working with responsible providers who, once accredited, become the main point of referrals for statutory agencies.

We are also rolling out a Quality Standards Framework and a Charter of Rights for residents (both co-designed with people who live or have lived in exempt accommodation) to set a local standard until Government regulations catch up.

A growing number of key partners across Birmingham have now signed up to only referring to providers that adopt both the Quality Standards and Charter of Rights. This of course requires a robust inspection regime and we are piloting one in the city.

But there is only so much we can do as a Labour Council. Ultimately we need the government to change course too.

The exempt sector has been, and sadly continues to be a rich market and there’s a clear need for stronger regulatory powers so that those who provide poor standards to their tenants, face real consequences. This effort is being spearheaded in Parliament by Steve McCabe, Liam Bryne and Shabana Mahmood on behalf of Birmingham’s Labour MPs, and new West Midlands PCC – Simon Foster.

On 19th April Birmingham Labour Group in collaboration with the Birmingham Labour MPs launched a city wide petition calling on Government for urgent policy reform:

The local impact in some areas is causing a misery for tenants and local communities. We firmly believe there should be local impact assessments implemented and tests of whether someone is fit to be a landlord to protect communities. We just need government support to do so and have put a bill to parliament that would guarantee this.

In Birmingham we’re making a difference and our message to unscrupulous providers is that we’re coming for you and your time will soon be up.

Cllr Sharon Thompson

Sharon Thompson has been a Labour Councillor for the Birmingham North Edgbaston ward since 2014.

Once homeless herself, and a single mother at an early age, Cllr Sharon Thompson is currently the Cabinet Member for Homes and Neighbourhoods and on the WMCA Housing & Land Delivery Board.

New polling by the Fairer Share campaign hints at the huge potential gains in store for a party that is brave enough to reform our broken property taxes. With local elections around the corner, four out of ten people would consider switching their vote to a party pledging to replace council tax with a fairer property tax system with lower annual bills for most people and local services maintained at the same level. In the so called ‘red wall’ areas of the country, the figures are higher with almost half of all people questioned saying they would consider switching their vote.

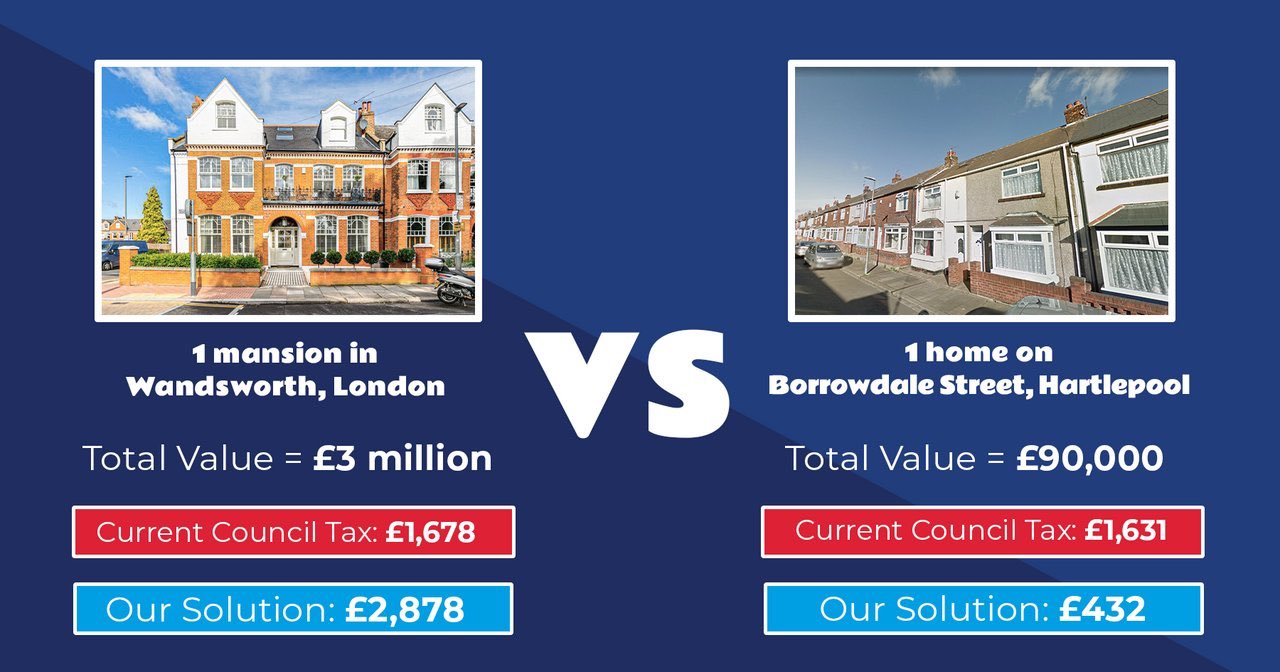

It should come as no surprise to see the extent to which many people are fed up with council tax. It is outdated and highly regressive, both within local areas and between them. Council tax hits the poorest residents of our society hardest while mansions or luxury apartments in Westminster or Kensington barely notice council tax, deeming it less than a service charge.

The worst hit areas are the regions of the United Kingdom once known as Labour’s heartlands, with the North East getting hammered the hardest. Hartlepool, for example, is the worst hit local authority. Residents there pay 1.31% of the value of their homes in council tax, whereas in Westminster, the average resident pays just 0.06% of their property value in council tax. That means the average resident in Hartlepool has a council tax burden 22 times that of Westminster.

Yet to talk about the regional disparities is to underplay the full extent of the problem. Council tax is derived by bands based on 1991 house valuations. The bottom bands pay a larger percentage of property value than the top bands, and houses at the bottom of each band pays significantly more than a property at the top of it.

At Fairer Share, we propose replacing council tax and stamp duty, which has a whole host of problems that hinder economic growth, with a flat property tax of 0.48% of the value of the property.

Flat taxes usually aren’t considered great progressive victories, but that is merely a reflection of the backwardness of the current system (something that shouldn’t be surprising given that portable MP3 players are five years newer than the current council tax regime).

Replacing council tax and stamp duty would be beneficial 76% of households across the UK. There are particular benefits for the poor, nearly 90% of the poorest in society and would add nearly £300 to their average net income per year. Although, on the face of it a neutral policy, it would also have social justice implications, with our analysis showing that large majorities of households in all the UK’s major ethnic minority communities benefiting from a move from council tax to a proportional property tax.

Remarkably, this policy can be achieved without taking a penny out of the treasury’s coffers. The flat rate of 0.48% would return exactly the same revenue as that lost by council tax and by stamp duty, and helping to preserve the vital local services on which we all depend. Raising money for police or social care with regressive precepts could be a thing of the past as local authorities could flex their local rate and raise revenues more fairly from their residents.

Support for the policy is growing in Westminster. Labour’s Grahame Morris is a key supporter, having pushed Boris Johnson on the policy at Prime Minister’s Questions recently. But the policy cuts across party lines, with a number of northern Conservative MPs also supportive.

Across the UK, more than 120,000 households have signed our petition calling for a proportional property tax. A progressive Labour party should also be wholeheartedly backing the introduction of a fairer system of property tax that will deliver in real terms for the majority of voters up and down the country.

Andrew Dixon

Andrew is the Founder of Fairer Share, the campaign to replace Council Tax and Stamp Duty with a fairer system through the introduction of a Proportional Property Tax.

Housing Revenue Accounts (HRAs) manage council housing. They receive no subsidy. Their income is overwhelmingly from tenants’ rent and service charges; 94% of the collective income of all HRAs. The quality of the homes, and hence the living conditions of tenants, depends upon key housing components (bathrooms, kitchens, central heating, roofs etc) being renewed in good time. If they are left beyond their useful life then the homes deteriorate.

Today, HRAs have insufficient funding to renew existing homes over the long term. My own council, Swindon, has a shortage of capital funding of £80 million over the next five years alone. This is unexceptional amongst councils. Whatever the differences between them all HRAs are short of sufficient resources.

Why are they short of funding? In 2012 a new council housing finance system was introduced – self-financing. It involved a ‘debt settlement’ in which what was deemed by government to be the national council housing debt was disaggregated and shared out amongst stock owning councils. £13 billion extra bogus debt was imposed on 136 councils.

In this fraudulent paper exercise the Public Works Loans Board (an agency of the Treasury) ‘loaned’ them £13 billion. Together with ‘historic debt’ councils owning housing are burdened with around £26 billion debt.

This isn’t in any real sense debt. It is the result of what you might call creative accounting by the Treasury. It’s a means of fleecing tenants whose rent pays off the loans and the interest charges. Currently, it costs councils £1.25 billion a year – 15% of the £8 billion total income of HRAs – to service this debt. Only 12%, £970 million, was budgeted for capital spending last year. That covers renewal of existing stock, cost of new build and purchases.

We can say this debt is bogus because we know that council tenants have paid more rent than the costs of borrowing for past building programmes. The House of Commons Council Housing Group discovered that in the 25 years to 2008, tenants paid £91 billion in rent but councils only received £60 billion ‘allowances’1. The £31 billion difference was more than outstanding debt for past building programmes. That’s why the demand to cancel this so-called debt was made by Defend Council Housing, the House of Commons group, even the LGA. Unfortunately John Healey refused to agree, as did the Tories when elected.

Grant Shapps, Housing Minister in 2012, said that it would provide sufficient funding for councils to be able to maintain their stock to the Decent Homes Standard, over the 30 years of their business plans. This wasn’t true. The previous government’s own research showed that if funding was based on actual need, it would require a 67% increase. Yet the increase was just 24%. So under-funding was built into the system from the very start. Then from 2012 the coalition and Tory governments introduced policies which resulted in the amount of income councils collected being much less than projected in the ‘debt settlement’.

The amount of so-called debt which each council was given was based on an estimate of their rental income over 30 years and the number of RTB sales (each home sold is rent income lost to HRAs). However, the government

increased discounts on RTB as a result of which there was a five-fold increase in sales. This meant that councils lost far more rent than estimated in 2012.

introduced a 4 year rent cut of 1% a year.

Since HRA business plans were based on projections which are now completely out of synch with actual income, councils are collecting hundreds of millions of pounds less rent than incorporated in their business plans. For example, Swindon is projected to collect approximately £360 million less rent over the course of the business plan than the 2012 estimate, Newcastle in the region of £500 million less. Overall, councils will take in many billions less rent income than estimated in 2012.

The result of this is that HRAs have insufficient funds to renew their existing stock in the long-run. Key components which are left in place beyond their useful life not only lead to worse living conditions for tenants and the irritation of repeated job requests as components fail regularly, but they also drive up responsive repair costs.

Labour’s 2019 general election Manifesto included a commitment to review council housing debt. Obviously it cannot do that directly without being in government. However, it is time for Labour to end its silence on this issue. It can challenge the Tories under-funding of HRAs. Under the 2011 Localities Act the government has the power to reopen the ‘debt settlement’ and readjust the debt if there are significant changes in income or costs. Labour should be demanding that the government do just that and write off debt at least in line with the projected losses that have resulted from their policies since 2012. Through its group in the LGA, Labour could collect statistics which highlight the scale of the shortfall faced by councils over the course of their business plans and organise a national campaign.

Labour should also make a commitment itself, to cancel the debt if elected. The Labour Campaign for Council Housing has just published a pamphlet, The case for cancelling council housing debt, which examines the historical reason for this financial crisis in more detail than I have space for here.

Debt cancellation would address the under-funding of HRAs in relation to the existing stock. The extra £1.25 billion would enable more than double the level of investment in renewal of key components to be spent. Labour should be demanding from the government funding sufficient to maintain and improve the standard of existing homes. Moreover, with a Decent Homes Standard review currently taking place Labour has a duty to highlight the consequences of this under-funding. Proposals to improve the standard of the DHS would be worthless without councils having the wherewith-all to carry out the necessary work.

The last year has heralded massive changes to the way we live and work. Millions of those in work have seen huge changes in the way they do their jobs, learning how to reduce Covid risks in the workplace, or carry out their job from home via video calls and remote working. Millions of others, however, have been out of work throughout this time – creating a growing gap with the new skills required in the workplace. Some jobs are starting to come back, but how many? In what areas? And will people whose jobs don’t return be able to find work in new areas?

Peabody Index background and findings

As a London-based housing association with over 150,000 social housing residents, Peabody has long been interested in helping our residents into stable employment with a living wage. Our Peabody Index reports track employment among our residents, comparing them with broader measures in London and throughout the UK, publishing updates throughout the pandemic.

Job vacancies in London are recovering, but they are sill 14% below pre-pandemic levels, compared with vacancies back to normal levels (or higher) in the rest of the country. Unemployment is still growing faster in London, with a 4.9% increase between December 2020 and March 2021 compared with 3.8% in the rest of the country.

Falling incomes have caused a rising rate of people are in high levels of debt. Worryingly, many are taking out bad loans just so they can buy essentials like groceries and toiletries. Young people and ethnic minorities appear worse affected.

The future is uncertain for those in work as homeworking seems to be with us for a long time. Londoners favour working from home more than their counterparts elsewhere in the country. Research suggests that about one third of them expect to work from home more in the future, mirroring the one-third of our working residents who are currently working from home. If workers in the City of London stay at home, there is serious concern for the future of the support economy that services those jobs.

What should policy do?

So what can be done? Employers need supporting to create jobs, and to support young people into the workplace – something that can be more challenging when staff are working remotely or when the economic future is uncertain. Peabody are pleased to be getting involved with the Government’s Kickstart Scheme for jobs and apprenticeships for young adults, which shares many ideas with the Opportunity Guarantee that Peabody has supported.

Given the broader shifts towards homeworking, many of us have taken on new digital skills, some of which we might take for granted. In February 2020, how easily could you share your screen on Zoom or co-edit documents on Sharepoint? For people who have lost their job during the pandemic or been unable to transition to homeworking, coordinated digital skills programmes will be needed to prepare for a future of working remotely. Other people have worked outside the home and developed a range of new skills – from taxi drivers learning new road layouts due to increased pedestrianisation to care staff learning to use PPE, our residents have told us of a huge range of new skills developed. Those not in work may need training to catch up and renter the workplace.

And despite encouraging signs of recovery, we need to make sure the welfare safety net functions well at the time it is needed most. That is why we continue to call for Universal Credit wait times to be reduced and the £20 per week uplift to be made permanent.

Helping social housing residents into work

At Peabody, we try to use the best evidence to help our social housing residents. During the pandemic, this means the evidence must analysed quickly and spread through to our teams. The Peabody Employment and Training Teams have helped 451 people into employment, supported 92 residents to achieve accredited qualifications and a further 103 residents into non-accredited training.

Delivering this support remotely has been challenging. We have developed a mix of online resources, independent training support, and general information sessions with guest speaker presentations. We try to make these sessions well-rounded, with guest speakers from local MPs, GLA Assembly Members and the South-East Chamber of Commerce. We are seeing a rise in those who are self-employed or planning to open a business. Our monthly business forums aim to help people get these ideas off the ground.

Not all work is done online, even during the pandemic. We have supported procurement opportunities and facilitated pop-up markets to provide the businesses with an opportunity to trade during and in-between lockdowns. This year we saw Thamesmead businesses, supported via our enterprise programme, on both the Greenwich and Bexley side win at their local business awards.

More needs to be done as we pull out of this pandemic. So much of the past year has been responsive – trying to make sense of the pandemic and its impacts. Only with rigorous research and evidence-based policies and programmes can we start to shape the future of work in London and the UK.

Greg Windle

Greg is a Research and Insight Analyst at Peabody.

Students often experience some of the worst housing conditions in the country, yet their voices are often marginalised and ignored. The issue has worsened, to the extent that student housing has essentially become a joke, with various popular culture depictions portraying the often disgusting conditions in which students are forced to live.

Fresh Meat provides a prime example of this; while it might seem hyperbolic at first glance, for those who didn’t go to university or who were privileged enough to be able to spend extortionate amounts on purpose-built student accommodation. Even students who can afford this, still face problems with the standard of accommodation and value for money available.

However, slug trails, mould, broken windows, burglaries and malfunctioning boilers are all issues that students are faced with regularly. This is not hyperbole, it is reality.

I have spoken to many of my friends and family members about student housing and nobody was surprised by my experiences of substandard housing and neglectful landlords. Everybody knows that this is happening. In my own experience, I have dealt with broken windows not being fixed for four months, mice, slugs, mould, no heating or hot water for weeks, windows with no curtains that woke me up at sunrise everyday and landlords turning up unannounced during a pandemic without masks.

Throughout this pandemic hundreds of students have posted on platforms such as TikTok, showing leaking ceilings, broken kitchen equipment and rat infestations. So it begs the question of why this is allowed to continue. It is a woeful neglect of young people and it leaves students incredibly vulnerable and living in awful conditions.

This isn’t only a problem with students privately-renting, it is also a problem with student accommodation, whether provided directly through the university or a third party provider. As the Guardian reported, student accommodation ‘doesn’t officially classify as housing…as it falls outside a specific use class, it doesn’t have to adhere to the usual standards associated with dwellings’. It means that student housing is often treated as either a hotel (C1) or residential institution i.e. care home or hospital (C2), because these types of accommodation are not intended for prolonged residence, there are far fewer regulations when it comes to space and daylight.

The responsibility for the poor conditions and facilities that students endure in purpose-built student housing lies directly with universities and third parties. Universities have, or should have, a duty of care to their students and exploiting gaps in housing regulations completely contradicts this moral obligation.

There is a huge divide in student cities, between aging university-owned student accommodation that is in dire need of refurbishment, and brand-new purpose-built accommodation often in city centres. For the majority of students, choosing their university accommodation for the first time they are faced with a dilemma: spend all or the vast majority of their student loan on quality accommodation and struggle with living costs for the year or have more money to enjoy their first year of university life, but live in poor housing.

Most students choose the latter and while it might seem like a good compromise for them, students should not have to choose between having enough student loan to survive, and living in adequate housing.

Part of this comes down to a lack of understanding about tenants’ rights among students. I’d argue that the blame for this lies with the universities themselves. They clearly understand the position that young people are in when they arrive at university. Yet, they don’t provide any real information to students about their rights with regards to renting. The vast majority of young people rent for the first time at university and so this kind of information would be crucial to these students. Why is none provided?

ACORN renter’s union has been working hard in many major student cities to provide students with more information about their rights. Additionally, they have taken action on behalf of students who are struggling with neglectful landlords, such as their recent action in Manchester when ‘over 25 ACORN members marched on the business address of Zear Property who left university student Kelsey in squalid living conditions so bad, that she was forced to move cross-country back to her hometown in the middle of the pandemic.’

While, of course, it is great that students have groups on their side in these situations and this support is clearly needed, it should be the landlords themselves and universities that are taking action. Additionally, it is clear that gaps in regulations surrounding student accommodation needs to be resolved.

It is interesting then, that when young people attempt to make their voices heard about their housing experiences they are often dismissed and deemed irrelevant or naive. The state of the housing market at present means that it will likely be decades before current university students are able to put down a deposit on a first house, and so their experiences of renting are incredibly valid.

Moreover, if young people do not know their rights with regards to tenancies and are taken advantage of during their university study, they will likely continue to be taken advantage of once they graduate. This creates more opportunities for landlords to cut corners, provide substandard accommodation and charge extortionate prices for the privilege.

The government has argued that it has introduced measures to protect students in student housing and this is woefully inaccurate. Although protections have been put in place regarding deposits, and this has been a welcome development, there is much more that needs to be done. This government announcement suggests that more has been done to make sure that landlords resolve problems quickly, yet this is just not being seen implemented in reality.

From my personal experience, I had to wait for three months for our heating to be fixed, despite being in constant contact with my landlord asking them to resolve the issue. Landlords certainly seem to exploit the lack of understanding of the rights of tenants at present and government action has done little to resolve this.

We need real, robust action from universities to provide useful information to students from the moment they apply, months before they will need to choose accommodation. Young people need to be aware of their options, realistic expectations and rights before they enter into any contracts. Some universities provide lists of approved landlords, who do not attempt to take advantage of students, while other universities actively attempt to discourage any such lists being made.

Universities need to be standing up for their student populations and working with local councils to ensure that private student housing is up to scratch. MPs also need to be raising this issue, to draw attention to the increasing disparity between aging student accommodation and modern expensive accommodation, but also to amend legislation to make sure that student housing is adequately regulated.

Greater consultation with students over their housing experiences would help to identify major problems and explore mitigation. Our experiences are valid and they represent a significant problem of landlords having too much power that is present throughout our housing sector.

Amy Dwyer

Amy is the Chair of the Young Fabians Education Network, Founder of the University of Manchester Young Fabians and Co-Secretary for Labour Doorstep.

Alongside this, Amy is also studying for her MA Politics and is standing as the Labour candidate for Longton and Hutton West in the South Ribble Borough Council By-Election.

The UK is in the midst of a housing crisis that isn’t going away anytime soon, with the pandemic only exacerbating this problem and leaving people struggling financially. Whilst we are seeing strong levels of first time buyers get onto the property ladder, simultaneously nearly 1 in 5 (18.7%) of households are occupied by private renters, with a further 16.7% of households occupied by social renters.[1] This is a huge proportion of the population, and whilst we are working to increase access to homeownership, it’s important that those who are currently renting are not left behind.

At MTVH, it is part of our DNA to support people at all levels and provide a quality home. Whilst we offer a dedicated shared ownership through our SO Resi brand, we also support those who are renting. For example, in London we offer London Living Rent which is a form of ‘try before you buy’ and allows Londoners to rent whilst building up savings to buy a home.

But let’s start with shared ownership.

Shared ownership is needed in society, as it provides an affordable opportunity for people to have access to a stable, well-located home. My personal belief in shared ownership is firmly rooted in my own experience – it’s not only how my wife and I were able to buy our first home, but also how my parents were able to get onto the property ladder after moving to the UK in the 1960s. My story is not unique and so many of my colleagues at MTVH have similar anecdotes about how shared ownership has given them the security of homeownership, which we know helps to open other doors to improve overall quality of life.

Our dedicated shared ownership brand SO Resi recently published a research report in conjunction with Cambridge University that looked at the shared ownership market in 2020. Perhaps most significantly, our research showed that since 2015/16, the number of shared ownership completions per year has increased from just 4,084 to 17,021. But it’s important to understand why shared ownership is taking centre stage for young buyers.

A combination of staggering house price growth, increasingly high deposits and a lack of lower loan to value mortgage options has led to aspiring homeowners moving away from the open market and utilising government products such as shared ownership. Whilst the government’s new 95% mortgages may work to address some of these problems, for many people a five per cent deposit on the open market is still out of reach.

Our research also revealed data sets surrounding the proportion of those who staircase each year. There is a misconception that those in shared ownership homes will never staircase, but our research shows that on average between 2-3% of shared owners staircase to 100% ownership each year. Staircasing isn’t possible for all shared owners, but the flexibility of shared ownership means individuals can make the scheme work to suit them – whether that’s living with a 25% ownership or working to increase your shares over a period of time.

Shared ownership has been around for decades, and the government’s plans to amend the product simultaneously presents both opportunities and concerns. Many of those who took part in our research specifically raised concerns around changes that will allow buyers to purchase a minimum 10% share rather than the current minimum of 25%. Housing providers will also be responsible for repairs for 10 years, leading to an increased financial commitment from providers.

There is no denying that these changes are advantageous for the buyer, and will open the doors even wider to homeownership. However, those surveyed believe the shift in responsibility of repairs will reduce the supply of homes that they are able to build. If the level of affordable homes available drops, this will worsen our current housing crisis and plunge more people into difficult situations when it comes to finding a home.

We know that a good home and environment are key in ensuring that everyone has the chance to live well. But homeownership isn’t possible for everyone – and whilst shared ownership increases access, there are still those who rely long-term on renting, whether privately or through a social housing provider.

To solve the housing crisis, we need to offer solutions that deal with different challenges, which vary as people need homes to rent and to buy. Instead of pitting one tenure against another, we need to collaborate and support those who do depend on the rented sector. Rent prices are rising and this is leaving a generation of people locked in paying high rent prices with no possibility of saving, either for a house deposit or to improve their quality of life.

Long-term, we need some clarity on solving the housing crisis as simply launching temporary schemes isn’t enough anymore – we need real policies that tackle the problems faced by young people today to ensure they can continue to get onto the property ladder at an affordable price in their preferred area.

In the current economic climate, shared ownership demonstrates its importance by supporting people to grow and start their families, put down roots and enjoy the benefits of homeownership without having to find the astronomical deposits required to buy on the open market. Like any product, shared ownership isn’t perfect, nor is it the single solution to the housing crisis, but it is an incredibly important offering that bridges the gap between renting and full ownership.

Kush Rawal

Kush is the Director of Residential Investment at Metropolitan Thames Valley Housing