The Levelling Up, Housing and Communities select committee is mid-way through an inquiry into shared ownership, which includes looking at the barriers to achieving full home ownership under the model and whether it is genuinely an affordable route to owning a home. Delve deeper into the terms of reference and it asks an interesting question: “are alternative schemes such as ‘Rent to Buy’ viable and do they offer more value for money?”

Rent to buy is not a new concept – the Coalition Government launched a £400m Rent to Buy scheme back in 2014 – but it has never really taken off in the way that other schemes to support first-time buyers have. From our experience on the ground, however, it feels like the tide is finally turning in favour of the tenure as more providers enter the market and an increasing number of local authorities adopt it as part of their housing mix.

This is perhaps a result of increasing recognition that the model has the benefit of tackling two key problems at once: in the vast majority of cases it provides new affordable homes to rent, whilst also providing a realistic route to ownership.

The Government describes Rent to Buy as helping tenants to save for a deposit to buy a home by offering properties at a discounted rent, normally 20% less than market rent.

Historically, it has been seen as a ‘niche’ product and there has been limited availability of it across the country, perpetuating the lack of awareness of the offer.

Now, with new entrants to the market, the sector is growing, but the challenge is that it is not homogenous. There are rent to buy products delivered by housing associations as part of their affordable rent provision; privately funded models that are included in local authorities’ affordable home ownership offer; and then rent to buy products that aren’t badged as affordable housing at all but are instead delivered as market homes. Muddying the waters further, the length of the rental period varies depending on the scheme – the 2014 scheme had a minimum of seven years renting, whilst the government website now states an initial rental agreement of just two. Some, like ours, offer a gifted deposit to add to renters’ savings, whereas others use the rental payments to count towards buying the property. This makes the sector hard to define in planning policy and confusing to navigate for local authorities, who are understandably wary of new providers in the market. Often, it is easier to stick to doing what they know.

However, as the cost-of-living crisis continues to bite, it is an attractive offer for renters who are struggling to save for a deposit and meets a major need in the market. Importantly, we have seen that it can successfully turn renters into homeowners.

As Keir Starmer looks for tangible ways to deliver Labour’s commitment to becoming the party of home ownership, he would be wise to look at how he can support growth of the rent to buy sector.

First and foremost, we know that saving for a deposit is one of the main challenges to getting on the housing ladder. In June, Zoopla found that the average deposit paid by a first-time buyer was £34,500, rising to £72,000 in the South East and over £144,000 in London.

For those who can’t rely on the ‘bank of mum and dad’, the difficulty is that often there is very little money left to put aside after paying rent and other monthly bills. The English Housing Survey notes that half of renters – some 2 million households – don’t have any savings at all. This rises to three quarters of those in the social rented sector.

This leads to a situation whereby the majority of first-time buyers come from the top two highest income groups, pricing out our nurses, teachers, retail and hospitality workers. This should not be the case. Workers across all income brackets should have a realistic prospect of being able to buy a home where they live. And we know that this is what they want; the aspiration to own has been constant at around 9 in 10 people for many years.

Labour will not be able to increase levels of home ownership and social mobility unless it addresses the deposit barrier. Rent to buy models do this in a way that Shared Ownership does not, by enabling tenants to move into the home that they will one day own without having to pay a deposit upfront, and instead being given the time and support to save for this.

The latest figures show that the average deposit for an initial equity stake under Shared Ownership was £20,800, putting it out of reach of the half of renters without savings. There is then the challenge of having to ‘staircase’ to full ownership, and the costs associated with this. Currently, comprehensive data on how many people reach full ownership and the time taken to do so does not exist, however, the House of Commons Library notes that the number of households staircasing to 100% in 2020-21 was equivalent to just 2.3% of all shared-equity homes owned by housing associations.

Homes England similarly does not collect post-sales information on grant-funded rent to buy homes; however under our model, 95% of renters have successfully become homeowners with a high street mortgage at the planned point.

On the question of whether rent to buy offers good value for money, we and other privately funded providers have proven that it is possible to deliver affordable home ownership products entirely without grant. We are fully funded by institutional investment such as major UK pension funds, meaning that there is no cost to the public purse whatsoever. As well as bringing more funding to the sector overall, using private investment to deliver affordable home ownership products enables local authorities to direct their grant funding to deliver more social housing; a win-win. This is an avenue that the Party seems interested to pursue, as the NPF document outlines that Labour will “encourage more private investment, properly regulated, in new supply”.

Rent to buy’s challenge is not that it is unviable, but that it has been small-scale and is not well known. With Help to Buy having ended, now is the time for it to be brought into the limelight and promoted as a major route to home ownership. Such a campaign from a future government would help boost local authority confidence and acceptance, encouraging more providers to the market and in turn increasing home ownership.

In addition, whilst privately funded providers do not require government grant through the Affordable Homes Programme, one of the main challenges is that local authorities are often reluctant to accept providers that are not government funded due to uncertainty over their standing. A Homes England equity programme for the rent to buy market would help to provide local authorities with confidence that the models had government support and had been assessed for quality and viability.

Following the G15 landlord Metropolitan Thames Valley Housing entering the rent to buy sector for the first time earlier this year, Inside Housing wrote: “Rent to Buy has been touted as a model that could replace shared ownership as the dominant affordable-ownership tenure.”

We believe that it can and that the Labour Party should be looking at how to make the most of its untapped potential.

Steve Collins

Steve is the Chief Executive at Rentplus, and has worked for more than 25 years in both public & private housing and development sectors

“We are on our knees in terms of the housing crisis. I have worked in this sector for 35 years and this is the worst I have ever seen it”

Fiona Fletcher-Smith, chair of the G15 group

To remedy what is already a catastrophe, we need to activate a national housebuilding programme to deliver the housing that the country needs now and into the future. It is only at this scale and by targeting the housing shortfall and needs of the country that we will stand a chance of providing the housing solutions this and future generations deserve.

Simply put, we need a lot of every type of housing, but mostly housing that is affordable, sustainable and secure. The housing we need is not being delivered due to a constrained planning environment, market conditions and funding complications. This is exacerbated by poor governmental leadership – 16 Housing Ministers in 13 years is not helpful. Institutes are unable to enact the measures needed due to being too risk averse and unable to support the affordable housing sector as they should.

Homeownership rates among 19-29 years olds fell by two-thirds over the period 1989 to 2013, from 23% to 8%. The housing shortage is also leading to an increased number of concealed households, with the number of adults living with their parents rising to 4.7 million in 2021, an increase of 700,000 compared with a decade earlier.

For younger people this is yet another setback in a long line of measures that are holding them back – lower relative incomes, rising housing costs and student loans. Not only is this having a significant impact on their short- and long-term life options, it also directly impacts on national productivity as younger people are held back in their careers due to their immobility.

In many areas of England, younger working people are often not eligible for, or are unable to secure, social rented homes. Due to a lack of affordable supply, home ownership or rental is beyond their financial reach too.

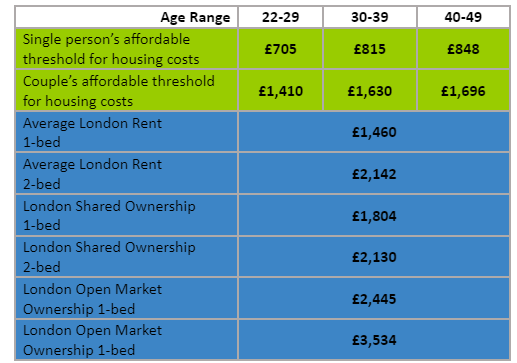

Set against median incomes, we can see that most forms of affordable (intermediate) homes are out of reach to people under the age of 35. This pushes more and more people into living in overcrowded or inadequate homes.

Chart 1 – The chart above shows what households should be spending on housing costs (green bars) based on the latest ONS data for median incomes against what is charged (blue bars). The affordable threshold for housing cost is calculated at 40% of net income (London Plan), which is the criterion set for affordability. It is 30% of gross income (Manchester housing strategy). The housing costs above are taken from actual housing offers around London and represent typical costs. It clearly shows that for people on median or lower incomes, they must exceed allowances to afford a home.

The Government states that you can buy a home through shared ownership if both of the following are true:

your household income is £80,000 a year or less (£90,000 a year or less in London)

you cannot afford all of the deposit and mortgage payments for a home that meets your needs

Yet, there is a huge gap between incomes and housing costs. The median incomes for all people aged between 30 to 39 (2020 ONS), in England was £32,259 – dropping to £27,087 for women, who make up the nearly two thirds of people buying shared ownership homes. Even with London weighting, this is a far cry from what is needed to buy a Shared Ownership or Discounted Market home in London which require incomes above £48-63,000 as shown below. A report from UCL illustrates that over the last 7 years, the value of the staircased share has increased by 60% implying that shared ownership is becoming less affordable.

Chart 2 – Example of typical incomes required for Shared Ownership Homes in London.

Chart 3 – Example of typical incomes required for Discounted Market Sales Homes in London.

The result is that well over 50% of younger working people, regardless of their jobs, do not have access to any independent housing options – this is a terrible situation and it is only getting worse. We are not building enough homes and not the right types of homes either.

To overcome the disparity between income and cost, we need to greatly increase housebuilding. We need to look beyond housing types and focus more on whether they are actually affordable to people. Too many people are getting further into debt and spending far too much of their income on housing and energy rather than wellbeing and their prospects.

There are a number of housing models (discounted rents or fixed shared equity) that can ensure affordability, but we are not providing anywhere near enough of these homes. Affordable housing providers and Local Authorities, if given the right levels of support, funding and expertise, can make significant inroads into delivering the homes we need. All suppliers of affordable homes should be supported with access to appropriately priced land and funding.

With the right housing policies and structures in place we can deliver the homes we need that are affordable, safe and protect us from the climate. We need stability and a determination to resolve the housing crisis. We can then aim to make housing a human right and begin to address the shortcomings set in front of younger people.

Pieter Zitman is an affordable housing provider and champion. He recently founded a Bursary to support disadvantaged architecture students in South Africa.

My report – Shared Ownership: The Consumer Perspective – explores gaps between aspirations and outcomes. It does so by assessing claims made for the scheme: that it is affordable, a pathway to full ownership, fair, user-friendly and a good product for the market to deliver. The report concludes that, despite the benefits of the scheme, there are also hazards arising from the characteristics of targeted homebuyers, the complexity of the model and of ownership structures, a lack of standardisation and consistency, inadequate information provision and weak regulation of marketing and delivery.

Here I touch briefly on three key underlying themes: long-term outcomes, consumer protection and value for money.

Long-term outcomes

Somewhat surprisingly for an affordable housing scheme launched over four decades ago, there are significant gaps in national data. How many shared owners staircase to 100%? (Excluding ‘back to back’ sales where a homebuyer purchases 100% by purchasing the shared owner’s share and the landlord’s share at the same time.) How many transition to full home ownership via a gain on sale? Is shared ownership financially sustainable over the long-term? What are the whole-life costs, and what are the opportunity costs if shared ownership turns out to be significantly more expensive than buying on the open market?

And without this information how can we possibly evaluate whether shared ownership is delivering for entrants to the scheme? Consequently the report recommends that Government and the Regulator of Social Housing undertake robust data collection, evaluation and reporting on the outcomes that matter to shared owners themselves: ongoing affordability and/or transition to full home ownership.

Consumer protection

Shared ownership can be tricky to get to grips with. The costs aren’t ‘shared’ and it’s not exactly ‘ownership’ either. Moreover, the ubiquitous marketing slogan – ‘part buy, part rent’ – was recently deemed to be misleading by the advertising watchdog, the ASA.

The ASA also found that adverts that do not “include material information relating to the costs of extending a lease” are likely to mislead. How many shared owners didn’t receive the facts they needed at the point of sale in order to make informed purchase decisions, taking into account likely future lease extension costs?

Of course, it’s impossible to turn the clock back. But many shared owners now face a double whammy. If they can’t afford to extend their lease, even selling may not provide the panacea they hoped for. The new model for shared ownership, quite rightly, requires a significantly longer 990-year lease term. But this could create a two-tier market further disadvantaging existing shared owners. Surely it’s only right to level the playing field by funding lease extension at a nominal flat fee for all those shared owners persuaded to buy a short lease and not informed, at the time, of the implications.

The complexity of shared ownership means that sometimes even the experts get it wrong. It’s an open secret that many shared owners have overpaid Stamp Duty Land Tax (SDLT) on simultaneous sale and staircasing. Unfortunately, HMRC currently imposes a 12-month deadline for refunds of SDLT overpayments meaning shared owners could unknowingly be left out of pocket as a result of incorrect professional advice. It’s a situation that clearly shouldn’t be allowed to drag on.

As one shared owner explains in Shared Ownership: The Consumer Perspective: “I had to pass an affordability test with the housing association initially to see if I could afford to pay for the share of the flat and its associated costs. But now, nobody cares whether I still can afford it. If I could sell, I would… but I cannot. Absolute and utter madness.”

Staircasing can also represent poor value for money. Unlike other instalment payment schemes where the initial cost is spread over a number of payments, shared ownership requires the prevailing market rate to be paid for each and every share. If property prices have increased since they bought their initial share, shared owners could pay considerably more in total than had they been able to afford to buy that home on the open market in the first place.

There appears to be even less justification for transfer of social housing stock to the open market via ‘back to back’ sales. What’s the likelihood of those homes ending up in the private rental sector, possibly subject to the unaffordable rents that drive many households to shared ownership in the first place?

The Shared Ownership: The Consumer Perspective report is aimed at decision makers in government, its agencies, regulators and housing providers, and makes a total of 18 recommendations. The Executive Summary and full report are available here. A suggested donation of £8.50 helps support the Shared Ownership Resources project.

Sue Phillips (FCCA) is a writer, retired charity finance manager and former shared owner. She launched Shared Ownership Resources in 2021.

Since 72 people lost their lives in the Grenfell tragedy on 14 June 2017, the cladding and building safety crisis has spiralled. Estimates vary as to how many households are affected. The End Our Cladding Scandal (EOCS) campaign believes that up to 11 million people are now caught up in the scandal. Luxury flats and social housing alike are affected. This article examines the impact of the cladding and building safety crisis on shared owners, and asks whether it lays bare fundamental flaws in the shared ownership model.

June 5th saw a National Day of Developer Protests outside new home sales offices, organised by local campaigners and supported by the national End Our Cladding Scandal (EOCS) campaign. The protests will be followed next month by a Leaseholders Together rally – planned in collaboration with the National Leasehold Campaign (NLC).

How long will it be before the spotlight shifts from developers to housing associations? How long before mass protests are taking place outside housing association offices and first-time buyer events?

What has gone so wrong that shared owners who placed trust in the promise of ‘affordable homes’ now face crippling bills? What are housing associations doing to support shared owners facing life-changing building safety remediation costs? Is it enough? What lessons may be learned, and what more can be done immediately to help shared owners and leaseholders in dire situations?

The Affordable Homes Promise: What’s Gone Wrong?

Schrödinger’s Flat

Shared ownership has been described as ‘Schrödinger’s flat’; it is simultaneously affordable and unaffordable. Housing associations define affordability by way of contrast to short-term costs of buying outright or renting, or accessibility of a mortgage deposit and loan. But these definitions oversimplify and distort understanding by failing to specify timescales of comparison, and by conveniently overlooking financial obligations imposed by leasehold contracts – such as indexed annual rent increases – and costs not referenced in lease terms, including lease extension. A rent that is often set initially as a percentage of the unsold share of the property, typically 3%.

Shared ownership is not ‘ownership’; it is an assured tenancy. And given that shared owners are liable for 100% of all maintenance and repair costs, on top of service and administration charges, and are now expected to pay for building safety remediation works too, it is clearly not ‘shared’ either.

The National Housing Federation chirpy marketing campaigns reassure first-time buyers shared ownership doesn’t mean sharing their home with a stranger but fail to explain clearly the risks arising from 100% liability for all costs. In fact, sponsored content encourages first-time buyers to believe ‘there’s no catch’. Not true! Something that the devastating cladding scandal has brought into stark relief. Problems for shared owners are complex and inter-related, full stop. Building safety issues massively compound inherent flaws and contradictions in the shared ownership model.

Staircasing rates were already dismally low: a mere 2.3% staircased to 100% in 2018-19. (It’s worth noting that this percentage is not analysed between staircasing to 100% to achieve full ‘ownership’, and a simultaneous sale and staircasing transaction undertaken purely in order to sell – a crucial distinction). The building safety crisis means any shared owners who planned to staircase to 100% are now likely to be unable to obtain mortgages to do so.

Shared owners who are unable to staircase to 100% have no statutory rights to lease extension. All things being equal, the cost of lease extension increases year on year. Particularly once the all-important 80-year threshold has been breached. And, in the absence of lease extension, shared owners’ homes will devalue dramatically over time (a separate issue from the nil valuations arising from building safety issues).

A significant number of shared owners will be trapped in negative equity situations as a direct consequence of building safety remediation charges. Those who purchased smaller shares, say 25%, are particularly disadvantaged. The people suffering the most severe financial distress may be those who had least to lose in the first place.

Going back to that £100,000 charge Irwell Valley Homes plan to levy on their shared owners… Although details remain sketchy, the Government has proposed a loan scheme capped at £50 monthly. At £50 per month, £100,000 would take 2,000 months, or 167 years to repay. Such charges are clearly a problem not just for this unfortunate generation of first-time home buyers, but for the next couple of generations too, perpetuating inequalities patently at odds with leveling up agendas.

How are Housing Associations Supporting Shared Owners?

Credit Loans

Some housing associations have obtained authorisation from the Financial Conduct Authority (FCA) to offer interest-free credit to shared owners where recharged building safety remediation costs are unaffordable. Although loans from housing associations have the advantage of being interest-free, unlike bank loans, this option raises a number of troubling questions.

The assured tenancy nature of shared ownership renders shared owners extremely vulnerable to repossession of their home in the event of mortgage or service charge arrears. Given the risks and unavoidable costs the current shared ownership model exposes shared owners to, what confidence can they have that housing associations and lenders have their best interests at heart? Why should they believe housing associations would be flexible as life circumstances change over the potentially life-long timespan of such loans? Additionally, housing associations that have already sold off freeholds may have tied their own hands regarding their ability to assist shared owners facing possession by lenders.

Such concerns are likely to be exacerbated by proposals to sell off shared ownership portfolios to institutional investors, whose primary motivation will be to maximise returns for their own shareholders and clients, not to act in the best interests of shared owners. This not only raises disturbing questions for the future of shared ownership, but also potentially stymies meaningful attempts to fix the broken housing market.

Buyback

Maureen Corcoran – a former board member of one of the largest housing associations in England, a member of the G15, and former Head of Housing in London for the Audit Commission – suggests that: ‘housing associations that sold these properties on a shared ownership basis could buy the shares back from anyone who is struggling and unable to move’. Housing associations counter that they do not have the financial means to do so at scale. Whilst some housing associations express commitment to do so in ‘exceptional circumstances’ it’s not at all clear what would constitute exceptional circumstances.

Where policies subtract the cost of any known or estimated remediation costs from the buyback valuation there may be little benefit of shared owners pursuing buyback as a way out of an impossible situation.

Back to back staircasing (a simultaneous staircasing and sale transaction) is sometimes required due to indexed annual rent increases (RPI plus 0.5%-2%). Where such increases have resulted in rent levels becoming more expensive than local private rents – or even specified rent on local new-build shared ownership properties – the property may become unattractive in the market place. Shared owners may have no other option but to eliminate the specified rent component, regardless of the erosion of any gain by the increased selling costs arising from the staircasing transaction.

Shared owners whose building doesn’t have a satisfactory EWS1 form face additional problems. Potential buyers are not currently able to obtain a mortgage due to nil valuations. To purchase a part share buyers have to meet affordability criteria; something that is highly unlikely to be the case if they are in a position to make a cash offer. Shared owners in this situation may have no alternative to back-to-back staircasing to 100% to facilitate a cash sale on the open market.

Confirmed or potential remediation costs will drastically reduce the purchase price. This is particularly problematic for shared owners whose housing association has a policy requiring shared owners to pay over to them any difference between the valuation and the purchase price.

Subletting

Subletting is generally prohibited on shared ownership properties. This is justified by housing associations on the basis that shared ownership properties are supposed to be the primary residence of the shared owner, and not a source of profit. Such an argument erroneously conflates ‘accidental landlords’ – who may need to relocate temporarily for a variety of reasons – with commercial for-profit operators. The no-gain requirement falls away once (if) a shared owner staircases to 100%, effectively penalising shared owners who can’t afford to staircase. Or, in the case of those whose buildings are found to have safety defects, are unable to staircase due to unavailability of mortgages.

The restriction on making a gain applies only to shared owners themselves and not to housing associations, who benefit from income streams generated from shared ownership homes; nor to institutional investors eyeing up shared ownership portfolios.

When exceptional permission to sublet is given it is on a ‘no gain’ basis; with no acknowledgement of the fact that in real life it is practically impossible for landlords to plan to break-even – not least due to the unpredictable nature of shared ownership service charges (including retrospective annual adjustments). Shared owners seeking to sublet rapidly discover they have taken on all the liabilities of home ownership, with none of the financial benefits and flexibility purchasing a home usually provides.

Are Housing Associations Doing Enough?

There are clear financial challenges for housing associations in addressing the building safety crisis. But growing vocal discontent across social media and elsewhere indicates that shared owners find it hard to accept how little housing associations are doing to support them now they are facing financial ruin. More than a few shared owners now regret the mistake of trusting persuasive marketing rhetoric.

Strong sector leadership is long overdue to protect shared owners from the worst consequences of a shared ownership model that has always exposed them to unlimited risk and costs regardless of affordability claims.

The following is intended to indicate some areas where the current offering could usefully be reviewed, by no means an exhaustive list.

Shared owners report that transparency and communication on building safety and related costs is poor. This is unacceptable and should be corrected as a matter of urgency.

“We know a bill is coming… Just not when, or how much…?”

A sector-wide review of whether current provision of expert financial advice and debt counselling adequately meets identified need.

A sector-wide published commitment to clearly identified policies to support shared owners facing building safety issues, including:

Not to initiate possession proceedings for shared owners in arrears due to building safety remediation charges (including waking watch and increased insurance premiums).

To waive marriage value on lease extensions (something MTVH have already committed to), and to calculate the premium on the percentage share held (where applicable) rather than total value.

Not to charge any difference arising between the valuation and the purchase price.

Work with mortgage lenders on whatever actions are required to facilitate access to consent to let or buy to let agreements.

Work with Government to remove, or apply considerable discretion on application of, restrictive and hard to justify restrictions on subletting, including no gain requirements and time limits.

Withdraw any shared ownership properties with potential building safety issues from the market unless it may be evidenced that there are no remediation cost consequences arising for first-time buyers.

Review marketing terminology to ensure buyers have full knowledge of exposure to long-term risks and costs. This information should include – but not be restricted to – building safety and defects, and associated costs and obligations. These should be simply, transparently and adequately explained to enable informed decision-making (in compliance with Consumer Protection from Unfair Trading Regulations 2008).

Review implications of cross-subsidy model for achievement of policy aims for shared ownership (affordability, fairness and transparency), and in relation to potential conflicts of interest.

What Lessons Can Be Learned?

The building safety crisis has bought into sharp focus a number of troubling aspects of the current shared ownership model:

a vast discrepancy between expectations created by marketing strategies and real-life outcomes;

adverse consequences of a policy and research focus on access to shared ownership rather than on performance of that tenure over the long-term and the success of exit strategies in achieving foot on the housing ladder policy aspirations;

adverse consequences of a policy and research focus on financial risks, costs and benefits arising for housing associations and mortgage lenders rather than those arising for first-time buyers;

lack of ability and will of housing associations to intervene where required arising from the nature of some partnership arrangements;

failure of housing associations to solicit and sincerely take account of the concerns of long-term shared owners and campaigners;

the conflict of interests which inevitably arises from the cross-subsidy model; and

failure to fulfil fiduciary duties.

These matters should surely be of grave concern for housing association Boards of Trustees and likewise for regulators including the Regulator of Social Housing, the Charity Commission, the Advertising Standards Authority, and the Competition and Marketing Authority.

Thanks are due to Dr Audrey Verma (campaigner), Deepa Mistry (shared owner and campaigner), Dr Alison Bancroft (shared owner and campaigner), Ed Spencer (shared owner and co-founder of One Housing Residents Action Group) and Neil Goodrich (housing professional) for support in writing this article. Any errors are, of course, my responsibility and mine alone. I welcome feedback on the content.

Sue Phillips

Sue Phillips is an accountant (ACCA) who spent much of her career working in the not-for-profit sector. She is now semi-retired. She says she never expected to become a housing campaigner!

She purchased her own flat via a shared ownership scheme in 1999, staircased to 100% in 2013, and completed a lease extension in 2020.

Her own experience of shared ownership led her to start campaigning in 2019, with a particular focus on greater transparency on potential long-term costs and risks of shared ownership. She campaigns under the moniker Shared Ownership Resources.

The UK is in the midst of a housing crisis that isn’t going away anytime soon, with the pandemic only exacerbating this problem and leaving people struggling financially. Whilst we are seeing strong levels of first time buyers get onto the property ladder, simultaneously nearly 1 in 5 (18.7%) of households are occupied by private renters, with a further 16.7% of households occupied by social renters.[1] This is a huge proportion of the population, and whilst we are working to increase access to homeownership, it’s important that those who are currently renting are not left behind.

At MTVH, it is part of our DNA to support people at all levels and provide a quality home. Whilst we offer a dedicated shared ownership through our SO Resi brand, we also support those who are renting. For example, in London we offer London Living Rent which is a form of ‘try before you buy’ and allows Londoners to rent whilst building up savings to buy a home.

But let’s start with shared ownership.

Shared ownership is needed in society, as it provides an affordable opportunity for people to have access to a stable, well-located home. My personal belief in shared ownership is firmly rooted in my own experience – it’s not only how my wife and I were able to buy our first home, but also how my parents were able to get onto the property ladder after moving to the UK in the 1960s. My story is not unique and so many of my colleagues at MTVH have similar anecdotes about how shared ownership has given them the security of homeownership, which we know helps to open other doors to improve overall quality of life.

Our dedicated shared ownership brand SO Resi recently published a research report in conjunction with Cambridge University that looked at the shared ownership market in 2020. Perhaps most significantly, our research showed that since 2015/16, the number of shared ownership completions per year has increased from just 4,084 to 17,021. But it’s important to understand why shared ownership is taking centre stage for young buyers.

A combination of staggering house price growth, increasingly high deposits and a lack of lower loan to value mortgage options has led to aspiring homeowners moving away from the open market and utilising government products such as shared ownership. Whilst the government’s new 95% mortgages may work to address some of these problems, for many people a five per cent deposit on the open market is still out of reach.

Our research also revealed data sets surrounding the proportion of those who staircase each year. There is a misconception that those in shared ownership homes will never staircase, but our research shows that on average between 2-3% of shared owners staircase to 100% ownership each year. Staircasing isn’t possible for all shared owners, but the flexibility of shared ownership means individuals can make the scheme work to suit them – whether that’s living with a 25% ownership or working to increase your shares over a period of time.

Shared ownership has been around for decades, and the government’s plans to amend the product simultaneously presents both opportunities and concerns. Many of those who took part in our research specifically raised concerns around changes that will allow buyers to purchase a minimum 10% share rather than the current minimum of 25%. Housing providers will also be responsible for repairs for 10 years, leading to an increased financial commitment from providers.

There is no denying that these changes are advantageous for the buyer, and will open the doors even wider to homeownership. However, those surveyed believe the shift in responsibility of repairs will reduce the supply of homes that they are able to build. If the level of affordable homes available drops, this will worsen our current housing crisis and plunge more people into difficult situations when it comes to finding a home.

We know that a good home and environment are key in ensuring that everyone has the chance to live well. But homeownership isn’t possible for everyone – and whilst shared ownership increases access, there are still those who rely long-term on renting, whether privately or through a social housing provider.

To solve the housing crisis, we need to offer solutions that deal with different challenges, which vary as people need homes to rent and to buy. Instead of pitting one tenure against another, we need to collaborate and support those who do depend on the rented sector. Rent prices are rising and this is leaving a generation of people locked in paying high rent prices with no possibility of saving, either for a house deposit or to improve their quality of life.

Long-term, we need some clarity on solving the housing crisis as simply launching temporary schemes isn’t enough anymore – we need real policies that tackle the problems faced by young people today to ensure they can continue to get onto the property ladder at an affordable price in their preferred area.

In the current economic climate, shared ownership demonstrates its importance by supporting people to grow and start their families, put down roots and enjoy the benefits of homeownership without having to find the astronomical deposits required to buy on the open market. Like any product, shared ownership isn’t perfect, nor is it the single solution to the housing crisis, but it is an incredibly important offering that bridges the gap between renting and full ownership.

Kush Rawal

Kush is the Director of Residential Investment at Metropolitan Thames Valley Housing

The Government has made the startling admission that it does not know how many people have transitioned to full ownership under its Shared Ownership model. Despite not knowing how effective it is, the Government has set out its expectation that Shared Ownership will account for the “vast majority” of the home ownership homes it funds.

Whilst the proposed new Shared Ownership model will make it easier both for people to buy an initial stake and then to increase their equity in the property, for some, the uncertainty over exactly how long it will take them to fully own their home will still not suit their needs. If you buy an initial 10% stake, after 15 years of gradual staircasing at 1% you would still only own 25% of the home. Legal fees apply at each increase and if shared owners want to buy larger shares using the existing process then all fees (valuation and legal) remain their responsibility. However large their share is, tenants also have to pay 100% of service charges.

For some aspiring homeowners, this part-rent, part-own process remains complicated and unattractive. Yet with first-time buyer deposits jumping £10,000 last year to nearly £60,000, key workers and those on lower incomes will struggle to buy on the open market. Despite the return of some 10% deposit mortgage deals, rising house prices combined with a partial public-sector pay freeze make saving this amount of money completely unrealistic for many.

As we have argued before in this blog, the key to widening access to home ownership is addressing the difficulty in saving for a deposit. It is this that is blocking many renters who could afford mortgage repayments from being able to buy a home. This has been compounded by coronavirus. The Joseph Rowntree Foundation’s annual report on poverty highlights that 41% of private renters who have seen a drop in income since March have had to use their savings to make up for the shortfall; savings that they might have been hoping to use for a house deposit. Many others didn’t have any savings to fall back on; over two thirds of social renters and almost half of private renters in the bottom half of the income distribution had less than £500.

Rent to buy schemes address this hurdle by not requiring any initial deposit when people move into a brand new house. They also provide a clear and defined route to full ownership with tenants buying their home outright at a set 5 yearly interval. Paying only an affordable rent enables them to save more for a deposit than if they were renting privately. At Rentplus we add to that by giving them a gifted lump sum of 10% of the value of the property when they are ready to buy.

In the meantime all repair and maintenance costs are covered by the landlord and service charges are included up until the point they become full homeowners.

The model is open to aspiring buyers provided they are working or in training. They undergo a financial assessment of their likely ability to buy before being accepted onto the scheme. Generally, applicants need to be on the local housing waiting list or Help to Buy or Shared Ownership register to be considered and they usually have a local connection to the area. In some areas up to half of tenants have moved out of existing social housing; freeing this up to be re-allocated to those most in need. Over half of all our tenants are key workers.

Unlike the unknown effectiveness of shared ownership in helping people to fully own their home, this spring the first of Rentplus’ tenants will become 100% homeowners after just 5 years.

Whilst all tenants are currently on track to buy, inevitably down the line some people’s circumstances will change and not everyone will be successful in purchasing at the planned date. In these cases tenants can opt to renew their tenancy in five year increments up to 20 years. If at this point they still can’t buy, we will work with the council and housing association to support them to look for new accommodation. They will have still benefitted from a 20 year affordable rent.

Rentplus’ model is fully funded by institutional investment bringing in additional housing finance and enabling councils to direct their grant funding to delivering social rented homes.

The main constraint to the model is that demand outstrips supply as only a small proportion of local authorities have adopted it to date.

Homes England reported a 34% decrease in affordable home ownership scheme starts over the six months to September 2020. Whilst coronavirus was a factor, this highlights the much greater role that privately funded providers can play in boosting the overall number of homes for first-time buyers with no reliance on Government funding.

The Government and local authorities should do more to encourage the development of innovative home ownership models on a much wider scale instead of putting all their eggs in the unproven, shared ownership basket.

Steve Collins

Chief Executive of Rentplus, the leading affordable rent to buy housing provider. Steve has over 25 years’ experience in housing and development, both in private and public-sector organisations.

This includes working for the then Homes and Communities Agency where he had responsibility for the successful delivery of over 42 Government programmes with a combined value of c.£900m pa, aimed at accelerating the delivery of housing and public sector land across the country.

Glossy ads present a rosy picture of shared ownership. But some first-time buyers are discovering the reality doesn’t live up to the rhetoric. Why are shared owners demanding greater transparency from housing associations and the National Housing Federation? This article breaks down some home truths about shared ownership, and what one housing campaigner is doing about it.

Shared ownership isn’t shared and it isn’t ownership. It’s arguable to what degree it constitutes affordable housing. Yet housing associations market this complex tenure with the same degree of levity with which a company might sell, say, comic books or whoopee cushions. The National Housing Federation (Nat Fed) marketing campaign promotes shared ownership schemes with slogans including: ‘Painting every wall luminous green’ and ‘Cooking in your pants on Sundays’.

My younger self would have enjoyed the jocular tone of Nat Fed advertising. My older self thinks the campaign does home buyers a great dis-service by failing to live up to laudable claims of ‘myth busting’ and ‘explaining what shared ownership means’. Taking out a mortgage could be one of the most expensive decisions first-time buyers will ever make. And, if they get it wrong, the consequences can be catastrophic.

An advertorial published during Shared Ownership Week 2020 included a quote from first-time buyer, Laura: “I think a lot of people don’t understand it, they think there’s a catch. There isn’t.” And there’s the problem in a nutshell… It’s perhaps a moot point exactly what constitutes a ‘catch’ but there’s no shortage of possibilities.

For a start, shared owners are often surprised to discover they don’t ‘own’ their home in any meaningful sense. The ‘part buy, part rent’ slogan is widely used in promoting shared ownership. But legal experts suggest that such terminology is potentially misleading as it misrepresents the legal form of the tenure. One law firm, Walker Morris (in a 2017 article ‘Shared Ownership: Risks and Rewards for Lenders’) say: ‘It is incorrect, and therefore misleading and potentially an offence in contravention of the Consumer Protection from Unfair Trading Regulations (2008) for housing associations, landlords, developers or lenders to advertise or refer to shared ownership schemes as ‘part buy, part rent’, or indeed by using any other terminology or slogan which suggests that the customer purchases anything other than an assured tenancy leasehold interest at any time prior to the 100% staircasing stage’.

The Nat Fed campaign appears to confuse a marketing strategy (defining ‘it’s yours’ as ‘not sharing’) with the legal reality (it’s not ‘yours’ and there are therefore risks of forfeiture, possession, and loss of or reduction in equity).

Shared ownership isn’t even that good an investment. The Homes England model contract specified a minimum lease length of 99 years for flats up until 2016, and 125 years thereafter. Shared owners have been shocked to discover a need for expensive lease extensions with no benefit other than to maintain the market value of their home. And, of course, some simply can’t afford to do so, and find themselves in possession of a devaluing asset. The London Mayor recently addressed this issue by unveiling a plan to ensure all shared ownership homes built in the capital as part of the new Affordable Homes Programme are sold with a 999-year lease as standard. But this doesn’t address problems faced outside London and also by legacy owners, many stranded with an increasingly unsuitable and undesirable housing product.

It gets worse. Shared owners have no statutory right to lease extension unless they’ve staircased to 100%. I contacted Mike Shone, Homes England’s Monitoring and Reporting Manager, in 2019 to ask what percentage of shared owners achieve full staircasing. The response: ‘Unfortunately this is not something that is recorded by Homes England or the Regulator of Social Housing’. But Parliamentary Research briefing CBP-8828 reports: ‘The increasing costs of shared ownership have made it more challenging for households to progress to full ownership. Around 4,000 households staircased to 100% ownership in 2018/19, equivalent to 2.3% of all shared-equity homes owned by housing associations’.

What about much vaunted affordability claims? These appear reliant on comparison with private rental or open market purchases over a relatively short timescale. They don’t factor in whole life cycle costs such as lease extension; rents that increase annually regardless of whether average market rents are increasing, static, or even declining; and full 100% liability for service and management charges regardless of the % share purchased. (Fire safety remediation costs are too complex to go into here but are self-evidently a source of huge emotional and financial distress for affected shared owners).

Housing sector professionals appear to believe that lawyers should provide information on such issues. Wanda Goldvag, chair of the Leasehold Advisory Service (LEASE), interviewed on Radio 4’s consumer affairs programme You and Yours in January 2019 said: “lawyers have an absolute duty to explain complex clauses to people”.

But it’s hard to understand such reliance on lawyers. Research funded by the Leverhulme Trust (Exploring experiences of shared ownership, 2015) found that: ‘Modern conveyancing practice is not equipped to provide information to buyers about the specifics of shared ownership leases. […] That increases the onus on providers to provide relevant, simple and clear information to buyers’.

Shared ownership is pitched as the ‘affordable’ route into housing. Marketing rhetoric implies that ALL buyers benefit from shared ownership as a ‘step onto the housing ladder’. But this is over-simplistic and fails to recognise that the wider housing market creates both winners and losers.

Moreover, a rapidly rising property market will benefit buyers who interpret ‘a step onto the housing ladder’ as obtaining a first property as an investment generating a gain to help buy their next property, but will disadvantage buyers who interpret it as an opportunity to purchase their forever home in staircasing instalments (the original intention of the scheme per the 1979 Conservative election manifesto). And the converse is equally true.

Whilst risks and opportunities arising from property markets are clearly not restricted to first-time buyers purchasing shared ownership homes, this demographic is particularly vulnerable to financial difficulties and poor outcomes arising from inadequate information and advice.

Housing associations have a dilemma; too much transparency could compromise achievement of sales targets. It’s pragmatic to assume housing associations will continue to place emphasis on short-term benefits to shift units. And, unless there are fundamental changes to the shared ownership model, many shared owners will continue to discover that shared ownership isn’t anywhere near as affordable as those glossy ads suggest.

Could the shared ownership model be improved? Could it be made more affordable? To some degree perhaps… A sector-wide commitment to cease taking advantage of the 2019 Zucconi precedent (a discretionary change in the method for calculating leasehold extension premiums which creates a windfall for housing associations, but pushes lease extension even further out of reach for many shared owners) would help some. Widespread adoption of the London Mayor’s proposal for 999-year leases as standard would render lease extension costs obsolete (except for increasingly disadvantaged legacy owners, of course!).

But here’s the rub… housing associations’ overall funding model has historically depended in part on profits arising from shared ownership schemes (for example, the receipts from staircasing shares sold at current market value rather than original market value) to generate cross-subsidy for social rented homes. So the financial interests of individual shared owners are directly in conflict with the wider objectives of housing associations. Shared owners are discovering they are, in many respects, the benefactors of affordable housing rather than the recipients they thought they were. It’s complicated!

If I had to choose one key policy reform…? “To stop using the term affordable for housing that isn’t” (a phrase I’ve stolen from Tom Murtha). To stop using the term ‘shared’ for housing that isn’t. And to stop using the term ‘ownership’ for housing that isn’t. Though that may not happen anytime soon. First-time buyers, shared owners and leaseholders deserve better. Which is why I’ve created a Crowdfunder project to raise funds for an independent shared ownership website with comprehensive information, analysis, and signposting to sources of professional expertise and advice. The Crowdfunder ends at 2.52pm on 9th February 2021.

Sue Phillips is an accountant (ACCA) who spent much of her career working in the not-for-profit sector. She is now semi-retired. She says she never expected to become a housing campaigner!

She purchased her own flat via a shared ownership scheme in 1999, staircased to 100% in 2013, and completed a lease extension in 2020.

Her own experience of shared ownership led her to start campaigning in 2019, with a particular focus on greater transparency on potential long-term costs and risks of shared ownership. She campaigns under the moniker Shared Ownership Resources.

Shared ownership has its benefits, but it is not the panacea for the country’s housing crisis.

Home ownership is becoming an ever-distant dream. Nowhere is this seen more acutely than in London where exorbitant house prices mean exorbitant private rents are often considered the only viable option. So those with the opportunity to get on the property ladder through the somewhat elusive shared ownership route are the lucky ones, right?

Well let us explore that further.

You can get a shared ownership home through a housing association. You buy a share of your home (between 25% – soon to be lowered to 10% – and 75%) and pay rent to the housing association on the rest.

Northern Ireland and Scotland set their own criteria, but elsewhere in the UK you can buy a home under this scheme if your household earns £80,000 a year or less (capped at £90,000 in London) and are either a first-time buyer, someone who used to own a home but can’t afford to buy one now, or are an existing shared owner.

It is true, there certainly are benefits to this arrangement. Shared owners have more stability than those renting. They are not so much at the mercy of a landlord who could evict them almost immediately under section 60. Greater permanency is met with greater control. Shared owners can paint a wall or put up a shelf without first seeking permission from a reluctant landlord.

Then there is the cost. Shared ownership can form a happy medium for those wishing to leave the private rented sector but who cannot yet meet the stratospheric costs of full ownership. This is again particularly true in London where the average house price is more than double that of the national average.

But just because this can be the more affordable option, it does not automatically mean it’s affordable by anyone’s definition. Which is where we begin to uncover the flaws of this scheme.

In London, shared ownership is increasingly expensive. An investigation by the London Assembly Housing Committee found that the incomes of new shared owners, and the deposits they must put down to buy their share, are generally higher than those of the average earner.

Affordability is called further into question when you compare what a share in a London property will get you with what you could afford in a part of the country with lower house prices. For example, a 30% share on a two-bed flat in Wandsworth could get you full ownership of a four-bed semi-detached in Wigan.

The purse strings must be loosened again when service chargers are factored in. Service charge estimates given to prospective shared owners often increase following completion. Residents can be presented with service charge statements a chartered accountant would have trouble understanding.

Any credit can soon turn out to be a false credit because the managing company has forgotten to charge for building insurance and service charge bills can increase each year because the faulty lift requires additional maintenance.

This is all compounded by the expense shared owners must take on to extend their lease, problems with poor maintenance of properties, and the difficulties in staircasing to full ownership. Moreover, residents continually report that Housing Associations are unresponsive to their queries and concerns.

With so many pitfalls, we might ask why shared ownership is considered the preferred option for many people. There will always be the lure of home ownership, but there is more to it than that.

Most shared owners are first-time buyers. Many have no experience of buying property, nor the financial and administrative burdens of shared ownership. The Assembly’s Housing Committee found that many reported not knowing what exactly they were getting into.

For those who have already undergone that process, some say the model still is not working for them, that they had not been given enough information when buying and that they’re now lumbered with spiralling costs.

So, what is to be done? Well, the positive news is that the scheme is not beyond repair. With the right political will, there are actions we can take today to make it work for those already in shared ownership, as well as prospective shared owners.

A requirement on housing associations to report on service charges and maintenance costs for every block of shared ownership homes is an essential first step, because the biggest hindrances to making these fairer are the lack of transparency and scrutiny.

This should be met with a requirement on housing associations to set out for prospective buyers, in one clear document, an accurate description of what shared ownership entails – and costs – in reality. Clear guidance should also be provided on routes for redress for those who feel they do not receive a decent enough service for the amount they fork out in service charges.

To understand the value of shared ownership in helping first-time buyers successfully get a foot on – and then move up – the property ladder, housing associations should be required to publish annually the types of tenure those that sell their shared ownership property are moving into, alongside staircasing sales.

Given the call upon affordable housing resource that shared ownership necessitates, this is the very least we should expect from those organisations who benefit. And on a similar note, the Government should reverse their decision to make it easier for shared ownership properties to be sold on the open market and work instead to ensure they remain affordable housing stock.

Labour’s role is, and always will be, to level the playing field. Shared ownership is a good place to start to explore how that might look under a future Labour government. Overhauling the scheme to make it more accessible to the many is one option.

But of course, there is always the alternative of moving away from this type of model in favour of more affordable housing options accessible to those on lower and middle incomes.

Sadiq Khan’s action in delivering record levels of affordable housing, driving up council house building in the capital and implementing the London Living Rent are shining examples of what can be achieved when Labour is at the helm. Now, just imagine what could be achieved under a Labour Government.

Len Duvall

Len Duvall is the London Assembly Member for Greenwich and Lewisham and has been Leader of the London Assembly Labour Group since 2004.

Before joining the London Assembly, Len was Leader of Greenwich Council for 8 years. On the Assembly, Len is Chair of the GLA Oversight Committee, Deputy Chair of the Budget and Performance Committee, and a Member of the Police and Crime Committee and the EU Exit Working Group.

Len leads on the London Assembly’s Campaign for a Domestic Abusers’ Register. He has been in elected office since 1990.

With property prices for first time buyers increasing 69% over the past 10 years[1] and an average deposit of £47,059 needed it is no surprise that shared ownership is thought to be a good option for first time buyers.

The part-rent part-buy properties are mainly developed by housing associations as “low cost home ownership” and so can qualify as the affordable housing needed to secure planning for new developments.

But does it really represent good value for money for the purchaser and the wider public?

There is a lot to love in shared ownership if you are fed up with paying rent to a buy to let landlord. You don’t have to have keep paying out management fees, deposits and all the other costs associated with renting. You also benefit from rising house prices.

With shared ownership only have to save for a 5% the deposit on the proportion of the property value that you are buying – if you are buying 25% of a £400,000 property the minimum deposit is £5,000. If you buy in the open market you need a £40,000 deposit for a property of the same value because mortgage lenders require a 10% deposit.

The downside is that you are responsible any repairs and maintenance – your shower breaks down; you must pay the plumber. Even if you only own 25% of the property, you’re responsible for 100% of the cost of new doors to meet changing fire regulations.

It can be expensive buying additional shares in the property, especially if you repeatedly buy small shares. If you want to buy any part of the remaining portion there will be legal, valuation, stamp duty land tax and mortgage fees to pay. If house prices are rising you will be paying more for property as the cost is based on current market value, not the price you originally bought it for.

Another drawback is that most shared ownership is on leasehold flats so that on top of the rent, owners must pay service charges and ground rent. Nor can shared ownership residents exercise the “right to manage”, so you will be stuck with your managing agent even if they are useless.

But the main problem is down to the so-called new build premium – a term used to describe the fact that most new build properties cost more than otherwise similar homes. In 2019 Zoopla found that on average a new build was £65,000 more than a similar older home in the same location. It is tempting to buy a property that has a dishwasher in the fitted kitchen, and a 10-year guarantee against major property defects. But is it worth £65,000?

All the aspirational property TV programmes focus on the “potential” in buildings – essentially buying something run down, making improvements with new kitchens and bathrooms, and creating additional value. So why is shared ownership restricted to properties which have no room for improvement, and where the main beneficiaries appear to be large scale builders who get their planning permission for large blocks through low cost home ownership and not true social, affordable housing?

The first two homes I owned were wrecks, cheaper than new builds and I was able to put in central heating, double glazing, and new kitchens over time. Just the sort of properties that are snapped up by buy to let portfolio landlords today. Why can’t subsidies be directed to people who are happy to take on a project and use local builders to make improvements rather than hand profit directly to the large-scale building developers?

In England there have been some co-operative shared ownership schemes, but these have mainly been based on a new development rather than benefit from the lower prices in the second-hand market. A number of housing associations work with disability charities to provide adapted housing through the government-backed HOLD (housing for people with long term disabilities) scheme in England.

Qualifying people can buy any home for sale on a shared ownership basis (part-rent/part-buy) and this model works well for people who have received compensation for an accident and qualify for long term disability benefits.

To assist people to buy their first home I think there needs to be a second-hand market option, backed by a housing association to manage the rental element and ensure the finances are in order. We don’t have to look far for a model – based in Belfast the Co-Ownership Housing Association[2] is enabling first time buyers to part-rent and part-buy in the second-hand housing market across Northern Ireland.

Since 1978 more than 29,000 people have been assisted to buy their first home and currently 9,000 people are currently co-owners. A 50% own/50% rent is cheaper than private renting and normally no deposit is needed. The home owner is able to choose the property they want to part-rent part-buy in the open market and, subject to valuation the housing association will buy 50% of the property and charge rent based on 2.5% of the value of the rented portion.

This will require a new way of thinking for housing associations and there will need to be some seed funding but rental incomes and purchases of additional portions of the property should make the scheme sustainable in the long term. If we want sustainable communities, we need to have a variety of tenures and affordable homes, and shared ownership can help achieve that.

Sue Rossiter

Sue Rossiter is the Chair of Bethnal Green and Bow CLP and is an expert in mortgage policy with more than 20 years experience of regulatory policy development.