“We are on our knees in terms of the housing crisis. I have worked in this sector for 35 years and this is the worst I have ever seen it”

Fiona Fletcher-Smith, chair of the G15 group

To remedy what is already a catastrophe, we need to activate a national housebuilding programme to deliver the housing that the country needs now and into the future. It is only at this scale and by targeting the housing shortfall and needs of the country that we will stand a chance of providing the housing solutions this and future generations deserve.

Simply put, we need a lot of every type of housing, but mostly housing that is affordable, sustainable and secure. The housing we need is not being delivered due to a constrained planning environment, market conditions and funding complications. This is exacerbated by poor governmental leadership – 16 Housing Ministers in 13 years is not helpful. Institutes are unable to enact the measures needed due to being too risk averse and unable to support the affordable housing sector as they should.

Homeownership rates among 19-29 years olds fell by two-thirds over the period 1989 to 2013, from 23% to 8%. The housing shortage is also leading to an increased number of concealed households, with the number of adults living with their parents rising to 4.7 million in 2021, an increase of 700,000 compared with a decade earlier.

For younger people this is yet another setback in a long line of measures that are holding them back – lower relative incomes, rising housing costs and student loans. Not only is this having a significant impact on their short- and long-term life options, it also directly impacts on national productivity as younger people are held back in their careers due to their immobility.

In many areas of England, younger working people are often not eligible for, or are unable to secure, social rented homes. Due to a lack of affordable supply, home ownership or rental is beyond their financial reach too.

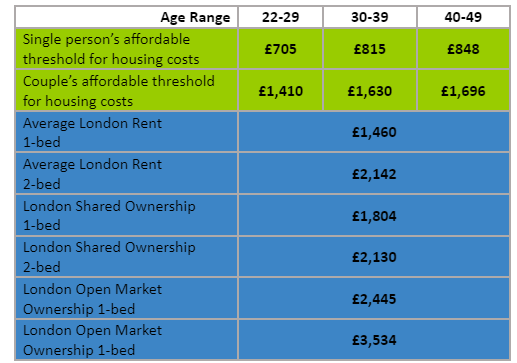

Set against median incomes, we can see that most forms of affordable (intermediate) homes are out of reach to people under the age of 35. This pushes more and more people into living in overcrowded or inadequate homes.

The Government states that you can buy a home through shared ownership if both of the following are true:

- your household income is £80,000 a year or less (£90,000 a year or less in London)

- you cannot afford all of the deposit and mortgage payments for a home that meets your needs

Yet, there is a huge gap between incomes and housing costs. The median incomes for all people aged between 30 to 39 (2020 ONS), in England was £32,259 – dropping to £27,087 for women, who make up the nearly two thirds of people buying shared ownership homes. Even with London weighting, this is a far cry from what is needed to buy a Shared Ownership or Discounted Market home in London which require incomes above £48-63,000 as shown below. A report from UCL illustrates that over the last 7 years, the value of the staircased share has increased by 60% implying that shared ownership is becoming less affordable.

The result is that well over 50% of younger working people, regardless of their jobs, do not have access to any independent housing options – this is a terrible situation and it is only getting worse. We are not building enough homes and not the right types of homes either.

To overcome the disparity between income and cost, we need to greatly increase housebuilding. We need to look beyond housing types and focus more on whether they are actually affordable to people. Too many people are getting further into debt and spending far too much of their income on housing and energy rather than wellbeing and their prospects.

There are a number of housing models (discounted rents or fixed shared equity) that can ensure affordability, but we are not providing anywhere near enough of these homes. Affordable housing providers and Local Authorities, if given the right levels of support, funding and expertise, can make significant inroads into delivering the homes we need. All suppliers of affordable homes should be supported with access to appropriately priced land and funding.

With the right housing policies and structures in place we can deliver the homes we need that are affordable, safe and protect us from the climate. We need stability and a determination to resolve the housing crisis. We can then aim to make housing a human right and begin to address the shortcomings set in front of younger people.

Pieter Zitman is an affordable housing provider and champion. He recently founded a Bursary to support disadvantaged architecture students in South Africa.