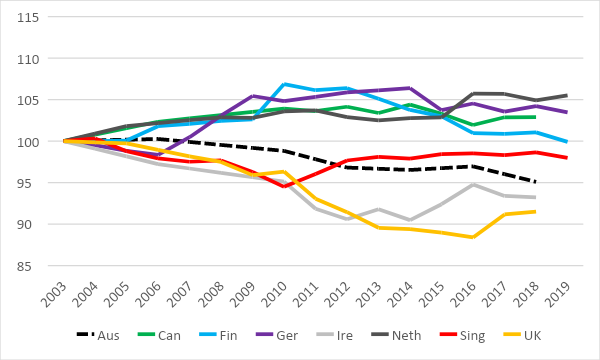

Boosting home ownership: an overriding housing policy objective for many decades, not only in Britain but the world over. And yet, as also seen in many countries, the past 10-20 years have witnessed owner occupancy rates static or falling – see graph.

Home ownership levels among young adults have widely plunged in much more dramatic fashion. In the UK, for example, the 25-34 age group owner occupancy rate declined from 51% in 1989 to only 28% in 2019. And, in another concerning dimension, both in the UK and Australia, within each age cohort, ownership rates have declined disproportionately among lower income households. Given the range of inherent benefits believed associated with home ownership, these trends present a major housing policy challenge.

It is not as though official endorsement for home ownership can be dismissed as purely rhetorical. Quite the contrary. As demonstrated by our recent research comparing approaches across eight countries including the UK, a highly diverse array of first-time buyer assistance interventions have been, and are being, pursued around the world.

Demand-side and supply-side interventions

In Britain this has lately involved schemes such as the Help to Buy shared equity model, where government effectively takes an equity stake in the value of an acquired home via a (time limited) interest-free loan, thus reducing the size of a purchaser’s necessary mortgage. Significant stamp duty concessions and government-backed low deposit mortgages have also been recently offered for first time property acquisition.

Since these types of help effectively enhance consumers’ ability to pay for housing, they can be classed as ‘demand-side’ instruments. Supply-side measures, by contrast, involve government support for home ownership targeted through housing suppliers (developers) or through the below-market-value disposal of publicly owned assets.

UK examples include grant funding for housing association shared ownership dwellings and the effective subsidy offered to council tenants exercising the Right to Buy, as well as developer contributions to affordable home ownership mandated through land use planning.

In Australia, while supply-side interventions are nowadays virtually absent, government-commissioned build-for-sale schemes formed an important instrument for boosting home ownership in the early post-war period. Direct state involvement in land and housing development to generate ‘entry level’ homes for sale meanwhile remains significant in both Germany and the Netherlands, and extensive in Singapore.

All demand-side and supply-side models identified in our research feature among seven distinct forms of first-time buyer assistance identified in our generic policy typology – see Table 1 in our published report.

Political potency

Generally speaking, anglophone countries (e.g. Australia, Canada, Ireland, New Zealand, UK) have in the past 10-20 years tended to see growing deployment of demand-side first-time buyer assistance measures.

Approaches of this kind chime with the neo-liberal preference for governments to act as ‘market enablers’ rather than to play a more direct role in provision. They also tend to be politically attractive because of their media appeal and electoral resonance.

However, especially where they take the form of cash grants or tax concessions, demand-side measures are widely criticised by economists and public policy experts as inequitable (because the beneficiaries tend to be moderate income rather than low income households) and ultimately counter-productive since, by boosting purchasing power for a commodity with inelastic supply, they contribute to house price inflation.

Those losing out under this type of approach – because of the higher prices consequently faced – include all aspirant first-time buyers failing to qualify for such assistance. The main beneficiaries, on the other hand, are existing home owners, whose properties consequently appreciate in value without any effort by property holders themselves.

Nonetheless, the political potency of home ownership affordability was notably highlighted in recent national elections in both Australia and Canada where rival demand-side first time buyer assistance measures were pushed high among contested issues by the leading rival parties.

Broadening access to home ownership?

How far do first-time buyer assistance schemes in fact broaden home ownership across the income spectrum, as sometimes claimed? From our own work we would largely endorse the conclusion of UK researchers who concluded in 2017 that:

‘[Low cost home ownership] schemes are not expanding … social mobility by opening up home ownership to new groups of lower income households. Rather they are being used by households who would most likely buy anyway’.

Instead, the main effect of models such as shared equity (e.g. Help to Buy) or low deposit mortgages is to bring forward home purchase for moderate income earners otherwise destined to buy some time later. Alternatively, beneficiaries are enabled to buy a home somewhat bigger, or better located, than in the absence of assistance.

Arguably, regarding the scope for broadening access to home ownership, the discounted sale of council housing to sitting tenants could be something of an exception to the rule, since many scheme participants have indeed been relatively low-income households. Nevertheless, considering the eye-watering value of the effective subsidy receivable via discount entitlement (currently up to £100,000 per buyer), the true program cost to government is, and has been, colossal.

Because such costs have been historically incurred without direct government expenditure (but, rather, by accepting a below-market price for a state-owned asset), they have had low political visibility. However, if the Conservative government was serious about its recently declared intention to promote housing association Right to Buy sales, this would change because the associations concerned would expect Treasury compensation for the value of discounts approved.

Some more recommendable first-time buyer assistance measures include:

- Mandating developers to include below-market price housing for sale (as well as affordable rental) in residential developments is recommendable on the grounds that the discount is effectively financed by taxing land value

- A strength of the shared equity model (e.g. Help to Buy) is its potential for lowering both the income and wealth threshold for home ownership access, to the benefit of lower income households.

- Enabling development of for-sale housing by state agencies or housing associations offers a means of providing dwellings that can be sold to qualifying applicants at cost price (i.e. no need to factor-in profit), while also expanding overall housing supply to the benefit of the wider market.

Housing unaffordability – the elephant in the room

Well-chosen measures to assist first-time buyers are a desirable element of a wider housing strategy. But their potential for expanding access down the income spectrum remains very limited if other key policy settings remain sacrosanct. Overall home ownership growth demands systemic change to tackle the much tougher challenge of easing broader housing affordability.

Yet this objective calls for the dampening of property values, an objective in tension with the dominant theme of home ownership policy: to facilitate wealth accumulation through asset ownership.

Some will argue that this demands land-use planning de-regulation to ‘free up supply’. In our view, however, the volume of new housing output is primarily influenced by developer response to market conditions, not by the planning system. Rather, the key problem lies in the taboo status of key tax and/or social security policy settings that in many countries encourage people with spare money – or credit capacity – to plough it into housing. In the UK context this could refer to the unlimited exemption from capital gains tax for the principal home, the weakness of the inheritance tax regime and the absence of a broad-based land tax.

A serious commitment to expanded home ownership demands consideration of phased reforms in areas like these.