‘The national project to make housing more affordable is focused entirely on increasing supply [and] … The plan for meeting the supply target is to change planning laws and allow more density in middle suburbs…’ So wrote revered Australian economic analyst, Alan Kohler in 2025.

Especially when it comes to the official narratives accompanying national housing policy in the 2020s, similar comments could be made for other countries including Canada and the UK, to name but two.

Even so, Kohler’s pithy summary underplays the diverse range of approaches that governments are nowadays deploying in their housing supply-focused efforts.

Moreover, while largely centred on planning reform and other ‘market enabling’ measures, initiatives in Canada and Australia now include direct commissioning and funding of housing construction on a scale without recent precedent.

To identify internationally adaptable approaches to boosting housing supply, our new study compared the post-pandemic housing market challenges and policy approaches of Canada and Australia, two of the world’s most comparable nations.

Structural factors

In both countries housing affordability challenges have come to the fore in policy and political debate since the 2010s, with rising house prices and rents generally outpacing incomes. Thus, Canada’s national house price-to-income ratio rose from under 4.0 in 2003 to 7.7 by 2022, with a similar increase observed in Australia.

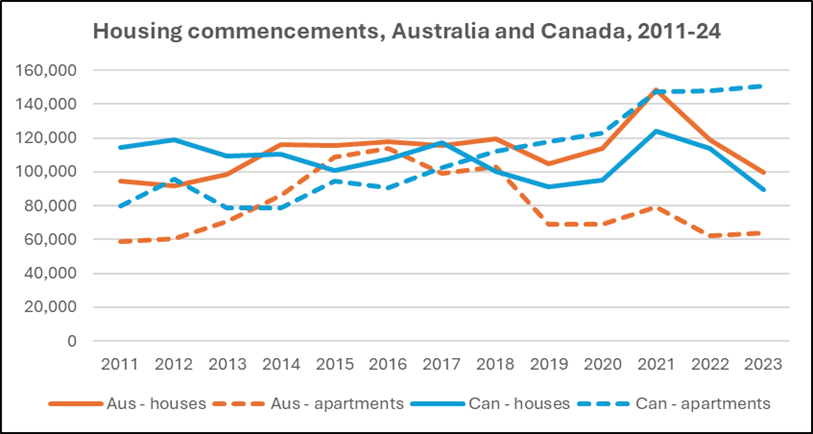

At the same time, the nature of the housing supply challenge in the early 2020s contrasts significantly across the two countries. Most notably, trends in apartment construction have markedly diverged. By 2024, such building starts had fallen by 48% from their 2016 peak in Australia, whereas Canadian unit commencements had surged by 71% over this period.

The main explanation for this contrast appears to be the revived vitality of Canada’s purpose-built rental (PBR) apartment industry in the post-Great Financial Crisis era. This is a sector far more strongly represented here than in Australia. Canada’s PBR construction surged more than threefold in the decade to 2024, representing a remarkable 42% of all housebuilding by that date.

As shown by the Canadian PBR industry’s relatively stable output in the immediate post-pandemic era, this speaks to the product’s resilience in the face of challenging market conditions. While abetted by favourable lending and mortgage insurance policies, the main explanation is probably the over-riding priority PBR investors place on long-term rental returns. This leaves them relatively sanguine about short-term market conditions and prospects.

Encouraging planning liberalisation

Efforts to both liberalise land-use zoning restrictions and streamline development approval processes are indeed central to contemporary pro-housing supply efforts in the two countries. However, federal administrations are constitutionally constrained here. Lacking powers to mandate planning policy (controlled by state/territory/local governments), federal influence must be transmitted indirectly.

In Australia this has been recently progressed under the Albanese government via the 2022 National Housing Accord. Central to this inter-governmental agreement was the commitment by signatory federal, state/territory and local authorities to ‘[i]mproving zoning, planning and land release’.

Accord participants also endorsed a national housebuilding goal to construct 1 million new dwellings 2024-29, later upped to 1.2 million homes within that timeframe. The federal government pledged a $AUD3B ‘New Home Bonus’ payable to state/territory governments conditional on achievement of jurisdiction-specific building targets.

Parallel Canadian efforts have centred on the federal Housing Accelerator Fund (HAF), a $CAN4B program to incentivise planning and other relevant reform by local governments. More subtly, HAF payments are intended to support municipalities growing housing supply ‘faster than [the local] historical average’.

As operationalised since 2023, Canada’s HAF program has involved federal-municipal agreements where, in exchange for pledged federal payments, lower tier governments have committed to specific planning reforms and other undertakings to expand housebuilding.

Beyond their status as ‘reward payments’ for relaxing or simplifying land use planning’, Canadian HAF subsidies fund other municipality actions on housing supply. This includes local commitments to channel such funds into affordable housing construction.

Other pro-supply measures

As unpacked in our research, though, pro-housing supply measures in both countries extend well beyond planning liberalisation. As represented to some degree in both Canada and Australia, these include:

- Infrastructure funding support

- Low-cost debt facilities and development de-risking

- Federal property tax reform

- Workforce capacity building

- Technological development

- Government-funded housing production

- Identifying and allocating public land for affordable non-market development.

Generally, these interventions have been disproportionately larger and more ambitious in the Canadian case – especially when it comes to de-risking private housing development, and in financial support pledged for pre-fabricated (or ‘modular’) housing construction.

But, while ‘market enabling’ measures remain dominant, recent initiatives have seen both countries also pledging muscular interventions in the commissioning and funding of housing for both sub-market rent and sale. The new Build Canada Homes agency launched by the Carney government is tasked with ‘[constructing] affordable housing at scale’ – including $CAN4B loans and $CAN6B contributions to [non-market] ‘deeply affordable housing, supportive housing, Indigenous housing, and shelters’.

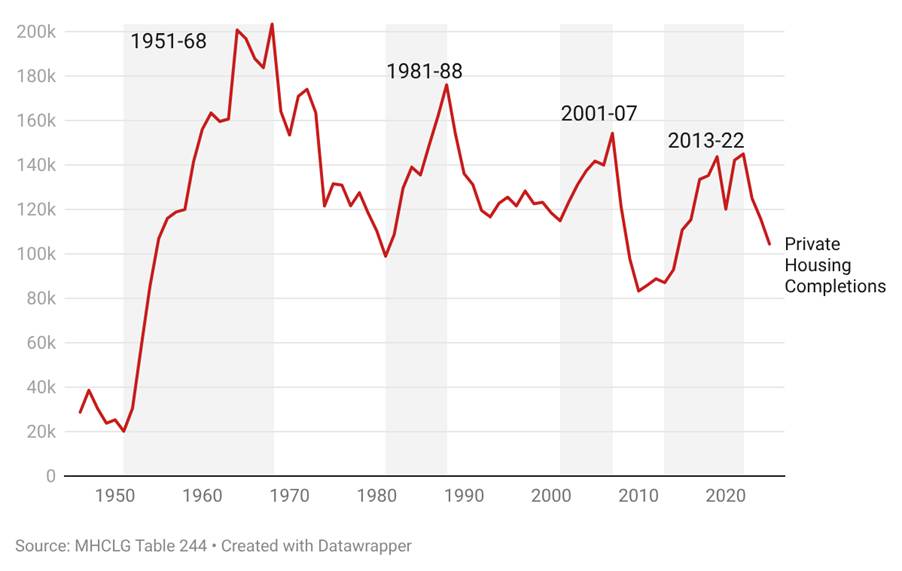

Meanwhile the Australian Government pledged in 2025 to commission 100,000 homes for (ring-fenced) sale to first home buyers over eight years. This revives a practice which contributed significantly to expanding Australian home ownership under the Keynesian consensus of the early post-war period, although subsequently absent for half a century until now.

The modern pre-occupation with expanding housing production while doing little to dampen housing demand remains highly questionable. But the range of pro-supply initiatives proceeding in countries such as Canada and Australia is far broader than the dominant ‘planning deregulation’ narrative implies. These extend to measures that, in their interventionist nature, arguably challenge decades of neo-liberal orthodoxy.

Much like its Australian and Canadian counterparts, the Starmer government’s housing reform narrative has overstated the scope for easing housing affordability through planning reform.

Lessons for the UK

As in those comparator nations, UK governments need to shift away from over-reliance on blanket efforts to boost market supply through development approval deregulation. Instead, taking a leaf out of Canadian and Australian books, the promised national housing strategy for England should embrace a wider range of pro-supply initiatives.

Emulating recent boundary-pushing measures under Premiers Carney and Albanese these measures should include more direct interventions that recall an earlier post-war era when such actions were standard practice.

Hal Pawson is an Emeritus Professor at the University of New South Wales Sydney. Steve Pomeroy is an Industry Professor at McMaster University, Hamilton, Ontario.

A version of this article first appeared on Australia’s Fifth Estate site.

Would you like to write for Red Brick? Email rose.grayston@gmail.com to pitch your piece (c.600-900 words)