At the eleventh hour, late on a Friday afternoon, the Government finally decided to stop ploughing ahead with reopening eviction cases in the courts on 24 August.

This news came as a relief to the many thousands of renters struggling to pay their rent due to the economic shock of Covid-19. However, a stay on evictions keep renters safe for now but it is just a sticking plaster. It is time the Government dealt with root cause and took action to end the rent debt crisis.

Even before the pandemic hit, two million households in the private rented sector were struggling to pay their rent – paying a staggering 40% of their income to private landlords on average.

Already stretched thin and with no savings to fall back on, private renters now find themselves without work or at risk of losing their job.

Having to rely on the welfare system, many for the first time, renters wait anxiously for money to arrive and are devasted when the housing allowance, even with the recent Government increase, nowhere near covers the rent they owe.

New research by Generation Rent found that just 12% of those who applied for benefits after lockdown have been able to cover their rent – meaning hundreds and thousands of renters have been forced to rely solely on their landlord’s goodwill.

With unemployment rising, the furlough scheme coming to an end, and an endless wait for an inadequate benefit payment, thousands of renters are at serious risk of losing their homes.

Renters like Elizabeth, Tim, Roy, Laura and Chrissie:

Elizabeth: ‘Our three-year contract is up. We informed our landlady we weren’t able to pay full due to cuts in our salaries due to Covid19. The landlady agreed – then the landlady gave us Section 21 eviction notice.’

Tim: ‘Covid 19 has meant that income has dried up. My landlord wouldn’t or hasn’t taken the three month mortgage payment holiday. I am 3+ months behind with my rent and frightened about receiving a Section 8 eviction notice from my landlord.’

Roy: ‘My landlord has been texting me once a month since this (pandemic) started telling me I’m going to be “out on my ear” if I don’t pay, trying to increase the rent while my income has halved and my savings are dwindling, I’m terrified for my children’s future.’

Laura: ‘I’ve been furloughed and the money hasn’t been coming in until the middle of the month so I’ve been unable to pay the rent on time. I haven’t slept I’ve been ill anxiety and depression levels have gone up.’

Chrissie: ‘We explained that we hadn’t been able to work for 3 months and we’ve rented for just under 30 years. The landlords agent said ‘well you know what to do, give the keys back if you can’t pay’. We’re not eligible for benefits as we own a retirement property abroad. We are both over 60.’

These stories break my heart. Sadly, Elizabeth, Tim, Roy, Laura and Chrissie are not alone. Their stories are just a snapshot of the renter experience Generation Rent hears every day.

Many have lived in their properties for years. They have children at local schools but now find themselves priced out of the area they call home. Some are behind with rent and others haven’t even been given a reason; their landlord has simply issued a ‘no fault’ eviction notice and asked them to leave.

Our research, carried out just a few weeks ago, has shown 1 in 5 private renters who has struggled to pay rent during the pandemic has already been told to move out, been given a rent increase or been threatened with eviction. Nearly half of struggling tenants were found to be already searching for a new home, with 59 per cent unable to find one they can afford or a landlord who will accept them – meaning homelessness will be the only option for renters as they find themselves with nowhere else to go.

Time is running out for renters.

In March, Robert Jenrick promised to keep renters hit by Covid-29 in their homes. He has to deliver on this promise. He has to put in place a permanent solution to alleviate the coronavirus rent debt crisis being faced by hundreds of thousands of renters.

With Parliament back from the summer recess, Generation Rent are more determined than ever to help renters saddled with rent debt.

That’s why we’re campaigning for an end to the rent debt crisis through lifting the benefit cap and increasing benefits to cover average rents, no rent increases until March 2021, and make grants available to cover the rent of the most financially vulnerable through our Coronavirus Home Retention Scheme.

We want to see an end to coronavirus evictions through emergency legislation to prevent ‘no fault’ evictions and evictions for rent arrears. This will ensure renters who have been hit by the pandemic do not lose their homes through no fault of their own.

And we want to see a permanent end toSection 21. Evictions for no reason were a leading cause of homelessness before the pandemic. Section 21 eviction notices are in frequent use and the pandemic has highlighted that the law is not fit for purpose. The Government has pledged to end ‘no fault’ evictions, and now is the time for it to honour this pledge.

Without a permanent solution to the rent debt crisis and evictions due to Covid-19 thousands of renters are at serious risk of losing their homes when the ban ends.

Generation Rent will be doing all it can to stop private renters tipping over the edge into homelessness. Homelessness destroys lives. Help us end the rent debt crisis – sign up at GenerationRent.org

Alicia Kennedy

A leader in strategic planning and campaign organisation, Alicia has had a 25-year career operating at the highest level of national politics.

She worked with Prime Ministers, Cabinet members, hundreds of MPs, and thousands of Councillors and volunteers to deliver successful local and national election campaigns for the Labour Party. She was made a life peer in 2012 and is non-aligned.

There are three things which are connected yet almost unique about the British economy. It has exceptionally stark geographic inequality; it has an extremely sharp housing crisis in its most expensive cities; and it has an unusually dysfunctional planning system.

Addressing those regional divides and the housing shortage requires replacing our discretionary planning system with a new flexible zoning system. The new reforms underway are one approach, but there are other examples from abroad which would also be major improvements over what we have now. But there must be fundamental change in how the planning system works if we want fundamental changes in inequality and housing outcomes.

Our discretionary planning system rations new homes

The current planning system is highly discretionary. This means that the planning system is empowered with a great deal of discretion to decide whether a development should take place on a specific site or not. In effect, new homes are rationed by the planning system, case-by-case.

Although there is often a local plan which “leads” development, this is not always true – York has not agreed one since the 1950s. Even when there is a local plan, the real power as to whether new homes can be built or not is in the case-by-case decisions by planners and planning committees. Applying for planning permission to build private homes, affordable homes, or social housing is never certain. One in ten planning applications fail, despite the fact that developers are presenting proposals they believe will succeed.

The discretionary planning system makes inequality worse

This mismatch between supply and demand creates terrible housing crises in the cities with the most successful labour markets and fuels inequality. In expensive cities, it widens divides between renters and homeowners. As housing costs for renters in Bristol increase, so does the wealth of their homeowning neighbours as house prices rise.

But it also creates divides across the country. As we do not build enough homes in cities like Brighton to stabilise prices, average housing equity per house in Brighton rose by £89,000 from 2013-2018. But an identical twin of such a homeowner in Sunderland would only have gained £3,000, as local land values have not risen due to the struggling local economy. This is the opposite of levelling up – the planning system redistributes wealth from the poor to the rich.

The discretionary design of the planning system creates a permanent shortage of homes

In fact, England’s discretionary planning system can be understood most clearly by comparing it to the planning systems of the former Eastern Bloc. In these planned economies, production was also rationed by the discretionary and uncertain granting of permits by planners, but for things such as mayonnaise or cars rather than new homes. Many of the behaviours which are sometimes described in England as unique to housing popped up across sectors in these Soviet-style economies – shortages, equivalents to land-banking, absorption rates, endless negotiations between planners and firms, poor quality new products, inequality in access to supply and speculation, among others.

These are more than just parallels. Both the former Eastern Bloc and the UK housing market are “shortage economies”. Their permanent state of undersupply is maintained by how the discretionary design of their planning institutions rations production, and is the defining characteristic of their systems. A few policy tweaks here or there or a little bit more funding won’t solve this core problem.

Instead England’s planning system needs fundamental reform which learns from other planning systems abroad that result in better housing outcomes, and for the discretionary element in our system to be minimised or removed.

England’s new zoning system is a move in the right direction

Moving away from a discretionary system implies a new flexible zoning system, where provided a proposal agrees with the local plan and building regulations so that the new structures are safe, it legally must be granted permission. This is a common form of planning around the world.

The new zoning reforms introduced earlier this month – establishing growth, renewal, and protected zones in England – are a big step in this direction. Within growth zones, there is no discretionary element, as the principle of development is already accepted by the zoning. Developments which comply with a design code and legally must be granted planning permission, after planning has resolved technical elements such as road layouts. This certainty will, within growth zones, end the unpredictable rationing of new homes that the current planning system creates, and by extension, address the housing shortage.

We can argue about the details, but we need a new zoning system to end the housing crisis

There are political choices to be made as to the inner workings of such a new zoning system, and Centre for Cities has previously set out how these could work. Japan is the clearest example of such an alternative framework abroad, where there are twelve different zones which shape the density and use of land while still providing much more flexibility than our current system.

But while the details of such a new flexible zoning system are contestable, the principle that we need one to solve the housing crisis is not. The discretionary granting of planning permissions is the single biggest systemic problem with our framework. If we want to improve the conditions and affordability of homes across England, we need to do things differently. We need to replace our planning system with a new flexible zoning system.

Anthony has also worked on research on commercial property in cities, services exports, productivity, and manufacturing. He also has a particular interest in lessons for planning, housing, and UK cities from Japan and the countries of the former Soviet Union. Previously he worked at the Fawcett Society as a Research Officer.

Supply is one of the key problems in the UK housing market. Sadly, the latest in-vogue argument is that the perceived housing supply shortage is a misconception. This track of thought has permeated right across the political spectrum. But do these claims hold weight?

Both centrists and the left have bought into the housing supply shortage myth. It is wrong to do so.

Last year the Labour Party produced its ‘Land For The Many’ report. In it all housings ills were laid at the feet of finance and speculation. Namely by the likes of Beth Stratford, Guy Shrubsole and Laurie Macfarlane. They argue there were “more powerful forces, besides supply shortages, putting upward pressure on house prices”. ‘Red tape’ in the planning system? Merely a “discredited theory”.

Regulatory supply constraints inherent within the current system have made house prices substantially more volatile. Research by Hilber and Vermeulen found the planning system has been an important causal factor behind England’s high housing prices. It was published in the flagship title of the Royal Economic Society. The Economic Journal.

Low interest rates would not explain 90% of house price growth if supply was more responsive

“Soaring UK property prices are due to low interest rates, not lack of housing supply, Bank of England finds” states yet another tabloid headline. Housing supply “will not solve the housing crisis” clamours Ian Mulheirn. If there were two more opposite statements of the truth these are it.

The low-interest rates “fuel” house price rises line of argument has caught up far too many economic commentators. Mulheirn claims institutions, lending policies, narratives, all interfere with the transmission that is the tide of global interest rates. Supply though? Not the answer.

Ian’s claim simply bears no logical validity. First and foremost, the same Bank of England report that acknowledges low interest rates have been the key explanatory factor of house prices rises, does not validate his own understanding. The doubling in house prices over the past 30 years would have been different if supply were more responsive to changes in price.

It suggested that had we had doubled the responsiveness of our housing supply to changes in price, and assumed lower income elasticity (i.e. the same change in income triggered a smaller percentage increase in demand), house price growth would have been cut by almost half. House price growth would have amounted to 88%. In contrast to the 173% modeled by the Bank of England on the current assumptions.

Income growth would have explained 55% of the increase. Decreases in interest rates explained just 40%. Therefore if supply was more responsive then both centrist and left-wing economist claims of mortgage lending being the key driver of house prices would simply not hold true.

In Japan housing affordability has improved despite a low interest rate environment

We can look to other countries and see low interest rates do not always explain housing unaffordability. For example, Japan has had low interest rates since the 1990s. Yet Japan’s price-to-income ratio has decreased by 31.3% since the year 2000. Over the same period the UK the price-to-income ratio has increased by 35.7%.

Cheap credit simply puts rocket boosters on demand in an already supply constrained market. Nothing more. Progressive housing policymakers need to recognise there is more to increases in house prices, and subsequently land values, than mortgage lending alone.

Antigrowth land regulations hand massive windfalls to landowners

Both are sadly defending the very man-made regulations that capture value into land. Enrico Moretti from UC Berkeley argues fixed or equitably anaemic housing supply results in productivity increases capitalised into land values. On the contrary if housing supply were infinitely on tap to meet demand then these productivity gains would go into workers’ wages. This is a given where there are fundamental economic drivers at play.

Not to mention what we have witnessed. In Central London for example, residual land values increased by over 600% in 20 years. Sounds to me like under the status quo landowners have been capturing massive windfalls for quite some time.

Research by Albert Saiz tells us the biggest determinant of poor housing supply responsiveness is geography. This is predominantly due to the physical constraints on land availability. Poor responsiveness of housing supply occurs indirectly due to increased land values resultant from this scarcity of land. Geography also indirectly creates higher incentives for antigrowth regulations such as the Green Belt. Of which ‘neighbourhood defenders’ like Guy Shrubsole and the CPRE vociferously protect.

Prices and past growth is empirically linked to planning regulations

Saiz tells us prices and past growth is derived from both physical and man-made (planning) regulations. Ian Mulheirn was presented this widely acclaimed study during his feature on The Jolly Swagman podcast.

But what did Ian Mulheirn make of the Saiz study dating back to 2010? He embarrassingly admitted he has never heard of it. Although still acknowledges there is relationship between prices and supply. Despite not recalling the paper Mulheirn claimed studies like this get the “order of magnitude wrong”. But we know this to be false. The assertion low-interest rates hold a higher magnitude does not hold true if supply responsiveness were more in line with international norms.

The link between responsiveness of supply and planning is not widely understood by housing supply shortage critics

Professor Ed Glaeser found in Greater Boston the decline in new construction, and associated increase in price, reflected increasing man-made regulatory barriers to building. Based on his empirical analysis he calls to ease housing regulation to increase supply.

Shrubsole, Stratford and Mulheirn all ignore or deny the empirical link between restrictive antigrowth land use regulations, lower levels of housing stock expansion, and exacerbated house price growth. While in places with relatively fewer barriers to construction the results are moderate increases in house price growth and a larger expansion of housing stock. Development professionals understand these international comparisons. And funnily enough, so do landowners.

The Federal Housing Finance Agency analysed a US data set of 14 million land values. It found supply restrictions and levels of land price positively correlated. Regulatory burdens and topographic difficulty in building result in an increase in the price of land. It is the largest dataset to suggest planning regulations impede the responsiveness of supply.

Unlike other countries Britain keeps making land more scarce in areas of high demand rather than expanding its supply

We must recognise the UK’s discretionary planning system is deepening wealth inequality by design. Political reluctance to review the Green Belt in terms of suitability for new homes has meant these restrictions have persisted for a prolonged period of time. All the while British urban conurbations have grown.

Other countries regularly review Urban Growth Boundaries (UGB) for expansion. For example, in the USA the state of Oregon expanded its UGB no less than three dozen times since it was first drawn. In the UK, the Green Belt has doubled since 1979. Instead of releasing land as our cities grow, we have done the complete opposite.

Thinly traded markets demonstrate the scarcity of land

The Investment Property Forum (IPF) notes the paucity of information on residential land values in the UK reflects the thinly traded nature of its land market. Being thinly traded means it cannot be sold easily without a significant change in price. This is due to there being a limited number of buyers or sellers.

Laurie Macfarlane believes this paucity of information makes it “difficult for policymakers and market participants to make informed decisions”. I argue to the contrary. Actors are making rational informed decisions. And those who are in the know are in the know. Landowners know in the long-run the economic incentives derived from the planning system will rule in their favour and that prices are sticky.

Developers on the other hand do face difficulties. Mostly with the planning system. In Britain developers can propose something not forbidden by the local plan, yet still lawfully be denied the right to build.

The planning system in Britain forces developers and planning authorities to haggle over height and affordable housing. Once a scheme is consented the permission can be sold on to crystallize the planning gain. The current system drives behaviour that plays on this uncertainty.

Land traders and middlemen punt around a thinly traded market consented schemes. Where often it can be slim pickings. This is in the hope another developer will take a view on height, massing, affordable housing once again. If house prices have moved on, they can capitalize these gains into land value. Simply stating 9 out of 10 applications are approved does not absolve the planning system for not seeing homes built out. It is at the heart of driving landowner economic incentives.

The current system has failed – how should Labour respond?

Anthony Breach draws parallels of the current system to the failed former Eastern Bloc. Our “Soviet-style planning system” has created crippling shortages of housing through institutional design. All ratified by political will. It is the case-by-case discretionary planning permission system that has created shortage economy in our housing market. This needs to change.

To grapple with the planning system Breach recommends a move to reconnect local demand through a rules-based zoning system. He claims should a developer propose a compliant scheme within zoning, design code, and building regulations then it must result in a building permit. Development proposed in line with neighbourhood plans that have been consulted on with the community will be determined by the need for new homes. Rather than by how much land has been rationed by the local authority and remains unsanctioned by local opposition. This gives the market certainty and takes the haggling out of land values.

In today’s context Breach’s recommendations should be revisited with a renewed focus on how such a planning system interacts with housing and the wider community. It is a myth to claim there is no housing shortage. And a myth to suggest planning plays no role in the responsiveness of supply to changes in price. We must turn to the academic literature and an empirical evidence base to inform our decision-making. Breach’s proposals may just have the answer.

Duncan Bowie argues the Labour Party has in the past failed to grapple with the planning system. He also said the Labour Housing Group should focus acutely on the relationship between housing supply and planning. I agree this needs to change. Labour needs to recognise and debate the positive and negative consequences of discretionary planning. Perhaps Breach’s proposals to the Labour Planning Commission can garner some further attention from the left. After all, they may be more relevant now than ever before.

Chris Worrall

Editor of Red Brick. Land Acquisition, Guild Living. Non-Executive Director of Housing for Women. Labour Housing Group, Executive Committee.

Previously Investment and Finance Manager at both Quintain and Thor Equities. Chris has expertise in developing new residential investment strategies and real estate development finance. He writes in a personal capacity.

It is the misfortune of the Affordable Housing Commission to release their report in March 2020, just as Covid -19 took hold. Not only did the report get buried by more pressing news, but the Commission also had to rush out a Covid-19 supplemental report in July 2020.

We need to rescue the report because it offers a great analysis of the housing crisis and realistic policy proposals. This is exactly what you would expect from a Commission headed by Lord Best, one of the sharpest minds in UK housing and supported by the left leaning Smith Institute.

The main argument is the last 20 years has seen the continuing decline of social rent housing, and the doubling in size of the Private Rented Sector (PRS) up to 22% of current housing. There are now 1.5m private landlords. Whilst, the social rent sector has continued to decline. The problem is that people who need the security of social rent sector face the insecurity of the PRS. Those on a low and insecure income, elderly, the ill and those with children should not be living in a sector where you can be required to leave with just a couple of months’ notice. For instance, a quarter all households with children now live in the PRS compared to 8% in 2004. People are staying longer in the PRS, often into old age. The Commission describes this as a ticking time bomb, as an increasing number of older private renters will find that they can no longer pay the rent when they retire.

The commission found that 23% of private renters are paying more than 40% of their income on rent, which is creating poverty. A Nationwide Foundation survey in 2019 found that a third of private renters had less than £39 per week to live on after they had paid essential bills.

In London the difference between social rent and private rents is the greatest, driving many below medium income into poverty. In the area of Bermondsey, south London where I work 50% of ex –council homes are now rented out, with private renters paying nearly four times more than their council neighbours and having to find a deposit of around £2,000.

The other effect of high rents is that it stops renters from building up the funds to escape into owner occupation. Bob Colenutt estimates a third of people born in the 1980’s and 1990’s will never be able to afford to buy their own home (Colenutt 2020). The average deposit needed by a first time buyer is London was a staggering £146,757 in 2019. Also the Commission highlights that the explosion of Buy to Rent mortgages has helped to force up house prices. Even George Osborne, the most political of Chancellors, recognised the need to slightly dampen down the increase in Buy to Let.

Within social housing, there has been a trend towards higher rent ‘affordable’ homes, rather than genuinely affordable social rents. Higher rents are seen as the way of spreading government money more thinly and building more ‘sub-market’ homes. Government subsidy has dropped by a third since 2010 and housing associations have moved 100,000 properties from social rents to higher affordable rents. The problem, as noted by the Commission, is that for low earners higher rents mean more poverty.

The Commission argues for a re-balancing of the housing market by increasing social rent housing, to provide an alternative for those for whom PRS is unsuitable. The Commission accepts that it will take 25 years to rebalance, and proposes that we start now so that a child born today should be able to live in an affordable home when they are 25 and want to live independently.

To achieve this, 90,000 new social rent and 55,000 shared ownership/ intermediate rent homes are needed each year to address the overall shortage of 3.1m social rent homes identified by Shelter

This will require an increase in government expenditure from 1.9% to 3%, which is £12.8 billion per year. To put this into context the housing benefit bill was £25 billion in 2016 and £1 billion was spent on poor quality temporary accommodation for homeless people in 2019, but neither expenditure resulted in any new homes. The cost of Help to Buy, aimed at helping first time buyers, was £10 billion in 2013 and there is a debate about whether the scheme added to supply or merely forced house prices up.

The Commission does argue for PRS rent caps, the end of Section 21 evictions and a landlord registration scheme to give some protection to those remaining in the private rented sector.

The Commission also calls for local authorities to be given discretion over the selling of their council homes, in the context of the intensity of housing need in their area.

In a Zoom meeting with LHG members, Thangam Debbonaire, Shadow Secretary of State for Housing, was clear that this is too early in this Parliament to make spending commitments, especially as the full effects of the Covid-19 recession are not known. However, this report seems to set out a good general direction of travel.

Andy Bates

Andy is on the Executive Committee of the Labour Housing Group and is a member of Old Southwark and Bermondsey CLP.

His is an advocate of residents collectively managing their own homes. Andy is a JMB Manager at the Leathermarket JMB. Southwark’s largest resident-managed housing organisation covering over 1,500 homes.

How arbitrary definitions and a focus on ‘headline figures’ are exacerbating the housing crisis

Nowadays it takes just a quick scan of the main newspapers to see the latest on what the government is planning to do to ‘help the people’. Slogans like ‘Build Build Build’ and ‘Jobs Jobs Jobs’ are recurring motifs – perfectly simple, sound bite morsels, that promise so much.

And, in theory the pledges look impressive. Boris Johnson’s £12 billion New Deal announcement for housing sounds huge, as does 180,000 ‘affordable homes’ over the next 8 years. That is the beauty of the marketing strategy. Without comparison these large numbers fill the imaginations of voters looking for hope in a dark situation.

But if we look a bit deeper, it’s exactly that, a marketing strategy. And not just that, but a marketing strategy working at the detriment of everything else. The Johnson government’s focus on headline stats has sacrificed true progress in solving the problems they are supposedly dedicated to.

To take Johnson’s New Deal specifically, how far will 180,000 ‘affordable homes’, over 8 years, go? It sounds significant, until you consider that approximately 14 million people in the UK live in poverty.

A cross-party report published at the end of July sheds light on the huge gap between the government’s aims, and what is actually needed on the ground. The report found that 90,000 additional social rented homes will be needed every year to meet the country’s housing need.

Currently, there are 83,700 households in temporary accommodation, and the number of people sleeping rough has increased 165% since 2010. If you needed proof to belie the attempts to promote the ‘Build, Build, Build’ scheme on the basis of radical progress, this report is it.

Particularly interesting is the committee’s stubborn refusal to use the word ‘affordable’, when describing housing attainable for the poorer sections of society. This is because the government’s definition of housing ‘affordability’ is perhaps one of the most pernicious examples of policy branding.

This clever tactic is based on exploiting the public’s associations with the word ‘affordable’. Obviously ‘affordable housing’ is going to be attainable for low income families, right? But curiously, the government definition of ‘affordable’ is not based on income, or wealth at all. It’s based on housing market rates. The government normally regards homes to rent or buy which are 20% or more below local market rates to be ‘affordable’. The key assumption here being that local market rates are accessible to the majority.

But, local market rates aren’t affordable to ‘average’ income earners. The latest ONS report on housing affordability found that in 2019, full-time employees ‘could typically expect to spend around 7.8 times their workplace-based annual earnings on purchasing a home’. As most banks will not mortgage a home worth more than 4.5 times an individual’s annual income, it’s clear that the average income earner can’t afford the average house.

So, when Boris Johnson pledges to build more ‘affordable homes’, he’s actually pledging to build more houses that are unobtainable to many people, and in particular those most in need. At the same time, homelessness, and the number of those struggling to find suitable housing grows.

A good illustration of the scale of the issue is the fact that 30% of 20-34 years olds still live with a parent – unable to afford rent or housing in the cities they work in. The general public however is presented an image of a government working to support the poorest in society, and ‘Build Build Build’ more homes for everyone.

Startling, is how effective this strategy is. After Boris Johnson’s ‘Build Build Build’ announcement, The Express ran a poll asking readers whether they thought the UK actually needed more housing. 62% of partaking readers thought not. The article talked about the number of empty properties in the UK, and how Brexit would reduce immigration – implying there was actually a lack of demand for affordable homes.

We should be particularly worried about the implications of this public feeling when it comes to the new planning regulations that Robert Jenrick is currently shepherding in: a mixture of increased Permitted Development Rights, and efforts to ‘cut the red tape’ of planning processes. The key message is that making it easier to build more homes will make housing more affordable.

However, research into use-change permitted development properties has consistently demonstrated that they fail to meet basic housing standards. The latest report published in July, found that only 22.1% of dwelling units met the nationally described space standards (compared to 73.4% through full planning). Ten units visited were even found to have no windows at all. On top of this, by avoiding the full planning process they’re also able to evade scrutiny on ‘affordable housing’ quotas (which as we’ve seen aren’t even that affordable).

These new regulations allow for the easier creation of low-quality housing by established developers and landowners, to be sold at unaffordable market rates – as well as a boost to the government who can claim the praise for boosting house building. What they don’t do is provide fit-for-purpose housing for those that desperately need it.

This strategy of ‘image first’ and big headline figures, is endemic to the operation of the Johnson government. We have seen this not just in housing policy, but across the board. Our first step should be to constantly question definitions and scrutinize the housing policy based upon them.

Rosie Hamilton

Rosie is a writer, and content marketer, working for a proptech start up. Her work focuses on researching the latest news, policy, and advice for homeowners. But, as a Northerner renting in London, she takes a particular personal interest in the difficulties the ‘average’ person has in the world of renting and finding affordable housing.

Before moving into her current role, Rosie worked for a property development company, and learnt a lot about the ways planning policy was being manipulated to maximise profit, often at the expense of the resident’s that would ultimately have to live there. This experience galvanised her views and provided the tools and insight to start to scrutinize it.

Landowners aren’t paying for the crisis. But they should be paying for the recovery.

Amid the carnage of lost jobs, bankrupt businesses and an overrun health service, one thing hasn’t changed: rent is still due.

That is not to say it shouldn’t be – as others have argued, there are wide ranging consequences from cancelling rent, that could have adverse effects for working people, and the labour movement as a whole.

But as with so many parts of our economy, landlords profit from others work. When someone takes a risk and starts a business, property values go up. When you renovate your house, property values go up. When the government invests in schools, transport, or a public park, property values go up.

And every time property values go up, so does rent.

When we pay rent, we’re not only paying landlords for the property we live in, we’re paying for our own taxes being invested in parks, services, and roads. We’re paying a windfall to landowners, regardless of the work they put into the property, or the quality of the service they provide.

Land isn’t like other parts of the economy. If people need more TVs, cars or computers, we can always make more TVs, cars or computers. But we can’t make more land. We have to do as much as we can with what we have. So as people need more housing, and more importantly, housing close to their work, friends and family, they become willing to pay more in rent – driving up prices to extortionate levels.

It’s why, even as jobs have been lost, businesses have closed and services strained, rent has stayed the same. As we begin to rewire our economy after the crisis, we need to recognise that landlords have earned

Rather than use a land tax, as some have proposed, to revamp local government funding, it should instead raise money for central government. It should be set at the same rate – say 1% of land value per year – across the country.

When property values go up – be it from government investment or new jobs and businesses in the area, landlords pay more tax, because their asset became more valuable. Doing so would be vital to reorienting our economy in the wake of our current crisis.

First, it would make tax fairer – shifting from those who earn, to those who own. Our government is funded on the backs of those who earn a wage, rather than those who pay their wages, or the owners of assets. A land tax would begin to change that.

Since 1997, the average house price has risen 259%, while the average earnings have only risen 68%.[1] If a land tax is used to fund a tax cut for working people, it will assuage fears of an increased tax burden, and leave the landowning middle class no worse off than they were before.

Second, it would redistribute wealth to the regions. Land in poorer areas and outside the main cities is worth less, and so would be taxed less. The effect would be more investment in rural areas, as businesses and workers alike respond to the incentives, and purchase land away from the main centres of economic growth.

Third, it would help counter the housing crisis. A land value tax, which should apply only to unimproved land, rather than the property as a whole, is designed specifically to encourage landowners to build more houses. When you renovate your kitchen, the value of the land underneath your home stays the same, and so your tax bill doesn’t change.

The more people living on a plot of land, the lower the tax bill per person will be, which makes higher density apartments more affordable than singe family houses. Denser cities are better for the climate, easier to get around in, and most importantly, have more housing for those most in need.

Finally, it would lower rents for everyone. Rents, which are driven not by the quality of housing, but by the value of land, would already be helped by encouraged density and discouraged property speculation. But unlike other taxes, landlords can’t pass a land value tax onto tenants.

The market is already so skewed towards landlords, that rent is based on what tenants can pay, not the expenses of landlords. And a tax applied to all land is a tax that cannot be avoided – you can’t store land in the Cayman Islands, nor can you make less of it.

Directly, rent makes up as much as half of the cost of living for working families. Indirectly, it shows up in everything from groceries to electronics. In London, a third of the price of a cup of coffee is just paying the rent.

Skyrocketing rents have crushed the high street and the family chequebook, priced aspiring workers out of jobs, and a generation out of its first homes. As we rebuild our economy in the wake of a pandemic, it’s time landowners paid their fair share.

Joe Pagani

Joe Pagani is a political strategist with a background as a New Zealand Labour Party activist and political commentator. He is a member of Bethnal Green and Bow CLP.

Describing his controversial plans to scrap the contributions that developers make to affordable housing and other local infrastructure, Secretary of State Robert Jenrick told the BBC: “This isn’t giving more power to developers – we’re actually asking them to pay more.” As the interviewer Nick Robinson reminded him, he was asking an awful lot if he expects people to trust him on this issue, when not long ago he’d helped a Tory party donor avoid developer contributions on a major development in London. “You need to win people’s trust, Mr Jenrick,” he pointed out.

Ironically, developer contributions (“section 106” in the jargon) weren’t “a product of the 1940s Attlee government” as Jenrick told Today listeners, but of the Thatcher government, shortly before it came to its end in 1990. This is not the first time that the system has come under attack – the combined forces of George Osborne and Eric Pickles during the coalition government worked to erode its effects, pressured (as ever) by developers complaining about “red tape” and giving as their excuse for cutting it the need to revive housebuilding and the housing market after the global financial crisis.

But it did not work. Developer contributions went from strength to strength. Back in 2000/01 they provided only four percent of affordable housing in England, and under the last Labour government this barely changed, reaching less than six per cent by 2010/11. It was under the coalition and then Conservative governments that developer contributions really took off. By 2012/13 they provided a quarter of affordable housing output and by 2018/19 this had reached almost half of the total – all of them homes built without government grant. The harsh reality was that, because the government had cut the grants budget, developer contributions were vital if some reasonable level of affordable housing output was to be sustained.

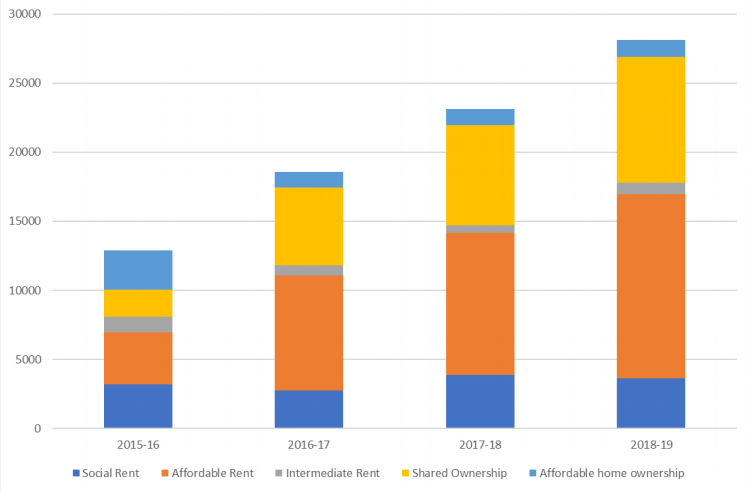

Figure 1: Additional affordable housing supply started, agreed through S106 agreement 2015-2019, England

Source: The Incidence, Value and Delivery of Planning Obligations and Community Infrastructure Levy in England in 2018-19 MCHLG, 2020

A report released quietly last week shows their importance even more sharply. The chart above is taken from the report and shows the recent growth in affordable housing supply resulting from section 106 agreements, broken down by tenure. The report says that contributions towards affordable housing alone were worth a total of £4.7bn in 2018/19; this was two-thirds of the total value of contributions, the remaining third going towards local infrastructure such as roads and schools.

To put this in perspective, the new Affordable Homes Programme announced by the Chancellor in March, and confirmed in his Summer Statement, is worth just £2.44bn annually, and this was flagged as a significant increase on the current programme, worth £1.95bn each year. In other words, what developers contributed to the delivery of affordable housing in 2018/19 is more than twice as much as the government paid out in grants.

The report has another statistic: 44,000 affordable homes were agreed in new planning obligations in 2018/19. This is a fall since 2016/17, but the value of this housing has increased over the same period due to an increase in house prices in many areas, with higher developer contributions. In 2018/19, the total of affordable homes built was 57,185, the highest in the last four years. Obviously the 44,000 new units arising from developer contributions will be spread over more than one year, but this comparison confirms their huge importance.

The new proposals would sweep away the existing section 106 agreements, which are negotiated locally, and replace them with a fixed national levy that would be based on the value of new developments. The amount would be set nationally but collected and used by local planning authorities.

What Mr Jenrick wants us to believe is that developers will pay more under this new system and that more affordable homes will be built as a result. He says the current system heavily favours the big volume housebuilders, which is true, and there is plentiful evidence of their finding ways to circumvent the system, not only by arranging to sit next to Mr Jenrick at Tory party fundraising dinners.

Indeed, his proposals do favour small builders, by proposing to exempt small developments of under 50 homes from the new levy that would replace section 106, at least for a limited period. But this worsens Mr Jenrick’s task, since small schemes currently do contribute to affordable housing. If he’s to be believed, and overall payments by developers towards affordable housing are to be even higher than the current £4.7bn, then big developers will have two extra burdens.

They’ll not only have to shoulder the contributions currently carried by small builders but will need to pay more on top of that. Developers have paid over £12 million to the Tory party since Boris Johnson took office: is this the return they expected for their investment?

Monimbó

Monimbó is a senior housing policy professional who has been a pseudonymous Red Brick contributor for many years.

England’s housing system is broken, and the out of area placement process could not make it more obvious. Out of area placements are used by local authorities across the country in order to address the ever growing demands for housing. Council’s often failing to find a local solution, will offer individuals the opportunity of accommodation outside of their hometowns.

Generally, authorities will use this option to source temporary accommodation opportunities, which are meant to provide short –term housing, but in some cases can last for over three years. Residents can also be offered permanent relocations out of an authority’s jurisdiction, if suitable housing is not available locally, through the private rented sector.

On the face of it that sounds like it should make sense, but in practice where real lives are involved, it is often a tragedy bordering on farce. Struggling London boroughs, not able to meet housing demands in already heated markets, eye up housing in the comparatively cheaper Home Counties to relocate their residents. Likewise, the now saturated out-of-London housing markets in turn force those local authorities to seek housing solutions elsewhere, some sending residents as far as 250 miles away to northern cities, in order to secure affordable accommodation, having made deals with private sector landlords.

These are capacity and cost based decisions that reflect the state of our housing market. In fact, some councils are paying hefty incentives to private sector landlords outside of their borough, in order to secure accommodation. Such incentives can be for thousands of pounds and can undermine an authority’s ability to procure housing in the local market, creating a vicious cycle of need.

In theory people can only be placed out of area for housing with their consent. In reality there are increasing questions about the legitimacy of this claim. A recent documentary, Forced out Families*, featured families from Medway who were moved as far as Bradford. One resident interviewed, claimed that he had been threatened with having his children placed in care, if he did not take the accommodation offer, while another was told he would not be able to keep his dog if he decided to stay local. The pressures placed on the housing system makes it incapable of addressing the needs of residents, forcing them to make decisions with little ‘real’ choice.

It is often the most vulnerable in our communities who find themselves in such challenging circumstances with the potential to have significant long-term impacts. Residents in need could potentially be moved hundreds of miles away from their families and local networks to completely different towns and cities without the support they need. Most at risk are children who in their formative years could be faced with unstable circumstances, with the potential to have a detrimental impact on educational achievement and mental health.

The impact on local resources is also significant. The law governing out of area placements requires that the receiving authority is made aware when residents are placed in temporary accommodation within their borough, but this does not always apply when the transfer is on a permanent basis. This means that local authorities will often have no real grasp of the numbers moving into their jurisdiction. In places like Medway, the increasing number of families relocating under this system is placing additional pressures, on already creaking local services, including schools and health care.

Most local authorities will express their frustrations at the current system, and stress that out of area placements are often a last resort. So what can really be done to fix this growing trend? Understanding the origins of the problem is the first step in finding solutions. A housing crisis, which sees house building failing to keep up with demand and chronic lack of social housing is central to the challenge.

It has been exacerbated in recent years by an increasingly unaffordable private rented sector and changes to the welfare system, driven by a Conservative government, which has placed an increasing number of households at risk of homelessness and left local councils struggling to meet housing demands. Regional economic inequalities are also highlighted, confirming that house prices in London and the South East are no longer sustainable.

The causes are complex, which means that the solutions are also not simple. Local authorities do not necessarily have the answer and in the long term it requires a complete overhaul of our housing system, addressing the inherent problems which have led to the current crisis. In the short term, local councils need to come together to look at how we can work better together to manage housing demands, share information and alleviate the burden on local resources.

Naushabah Khan has been a Medway Councillor since 2015, and is currently Medway Labour’s Spokesperson for Housing. Naushabah is passionate about securing sustainable development in Medway which includes sufficient affordable housing and proper infrastructure.

Naushabah was a Parliamentary Candidate for the Rochester and Strood in both the by election in 2014, and the general election in 2015. She is the Local Government Representative for the South East and works as a Director in Public Affairs.

The anticipated planning reforms will be the biggest changes to the planning system seen for some time – a complete overhaul. Planning isn’t perfect, but nor is it beyond repair. If government are serious about housing delivery, they’d be talking about sensible improvements not whole-scale reforms. Instead they seem intent on riding roughshod over local people and all too willing to put private profit ahead of what our neighbourhoods actually need. So if it were up to me, what would I be doing? There’s plenty to do, but these are three things I’d start with.

Firstly, the housing delivery test. A small but technical change could really push developers sitting on land with permission to actually focus on delivery. The Local Government Association estimate that nearly 9 out 10 applications are approved and in the last decade alone nearly a million homes have not been built despite permissions being granted. The Housing Delivery Test measures the number homes delivered against the number of homes required. Where delivery of housing has fallen below the housing requirement, councils can be penalised.

The main issue is the fact that Councils, unless they are their own schemes, do not deliver planning permissions – they are totally reliant on the market/ developers/ registered providers. Developers may seek to restrict delivery in order to maintain profit levels; landowners may gain permission and land bank rather than actually deliver; and registered providers are also heavily dependent on state funding streams. Crucially, events such as cyclical changes to the economy, and currently Covid-19, can significantly affect delivery which councils have no control over.

So a solution? Give local authorities the power to rescind permissions or more radical still take the build over themselves, if possible using better compulsory purchase orders if development does not begin within a year. Not a huge change but certainly could stop land-banking and start delivering housing and infrastructure.

Secondly, permitted development (PD). It has morphed into a policy that will cause more harm to a locality than actually result in good quality homes and a Government report has concluded the same. Aside from the fact there have been numerous cases of horrendous office to residential conversions and no obligations to affordable housing, PD has resulted in the displacement of valuable business and employment in many areas because the residential return far exceeds the commercial. The new permitted development rights could actually see high streets decline even further. Something that goes against what the Government are seeking to do.

I am not suggesting residential conversions can’t take place in high streets but it needs to be in a planned process that takes in to account the local economy and secures quality and space standards. In Brent we have introduced an Article 4 direction in growth areas to stop office to residential conversions and are now seeking to expand that for the whole borough. My solution would be to give councils the ability to opt in to PD with guaranteed quality of housing, rather than a blanket nationwide policy. It needs to be locally led and part of a solution to address local housing, infrastructure and economic needs.

Thirdly, public sector land should be developed in partnership with local councils not developers. Currently, many public sector bodies have housing targets and often go to developers to deliver those numbers. This results in public sector land being sold, as well as not delivering 100% affordable housing due to ‘unviable’ financial viability assessments.

A simple solution is to legislate that public sector organisations give councils first right of refusal on land to deliver housing or enter in some sort of partnership. Councils can borrow again to build housing and combined with grants, schemes can be delivered with higher numbers of affordable and social homes on all public sector land.

Essentially, these solutions are small but significant and are certainly not only thing we need to do. Fix what is currently not working in the system, give councils the freedoms and powers to maximise affordability, infrastructure and support for local economies. Covid has changed so much and it now time to take decisive action to support councils properly in housing and infrastructure delivery. It is now time to enable councils to lead the housing market, not be hampered by it.

Shama Tatler

Councillor Shama Tatler is the Cabinet Member for Regeneration, Property and Planning at the London Borough of Brent. She was elected to represent the Labour Party in Fryent Ward in May 2014 and has been a Cabinet Member since Dec 2016.

She is running for the Labour Party NEC and her reasons for running can be found here. Shama also sits on the LGA City Regions Board and the West London Economic Prosperity Board.

We cannot borrow our way out of the housing crisis: mortgage credit is part of the problem

One of the key issues highlighted in my new book about ‘Generation Rent’ is how mortgage lending drives the UK housing crisis. I am far from the first person to point this out: my understanding of the problem is drawn from the research of the think tank Positive Money, IIPP economist Josh Ryan-Collins, property cycles expert Philip J Anderson, and many others.

But no-one in government seems to be taking it seriously. As a result, a dangerous policy proposal in the 2019 Conservative manifesto has gone largely unchallenged: the promise to support the mortgage industry in delivering long-term low fixed-rate mortgages for first-time buyers, which will ‘slash the cost of deposits’. This may sound like an enticing idea, but in practice it will only pour more petrol on the fire.

The truth about where mortgages come from

When you take out a mortgage, the lender conjures new money into existence. The money doesn’t come from other customers’ savings accounts, nor does it come from bank ‘reserves’: it is created from nothing.

The main constraint on mortgage eligibility is the borrower’s ability to repay the debt. Effectively, a mortgage is a large withdrawal from The Bank of Future You. And while you can typically only borrow 90%-95% of the property value, this does little to keep mortgage borrowing in check, as property prices can rise in response to expanding mortgage credit and vice versa.

When property and mortgages collide

When cheap and readily-available mortgage credit meets residential property, house prices shoot up. This is because the supply of land, which accounts for about 70% of the value of a home, is fixed. No market can produce new land in response to the demand for housing created by expanding mortgage credit. And you cannot take out a mortgage against a home that hasn’t been built yet.

So, what you get is an ever-expanding supply of money chasing after a finite amount of property. Maybe we should think of it this way: rather than house prices going up, the value of money itself has been systematically trashed relative to the value of property.

What if we pour new money into new homes instead?

This was the rationale behind the government’s Help to Buy Equity Loan scheme, which was reserved for new-builds only. The idea was that, because the new loans would be used to increase the housing supply, the scheme wouldn’t lead to house price inflation.

A culture of land speculation entrenches the issue

Maybe the land-credit feedback cycle would be dampened if it were possible to take out a mortgage to fund a self-build property. But to acquire land, you normally have to satisfy a landowner’s price expectations (claiming vacant or unregistered land in this country is almost impossible). These expectations are likely to have been warped by the speculative nature of the land market.

Most landowners know that, under current rules, a piece of agricultural land can become around 92 times more valuable with a grant of planning permission for residential buildings. If the seller doesn’t like the price on offer, they can withhold their land indefinitely with no consequences.

A whole ‘land promotion’ side-industry has sprung up to enable speculators to share in the planning uplift, using legal mechanisms like ‘option agreements’ and ‘promotion agreements’ to reduce risk and increase profits. As a result, land is scarce and acquiring it is both costly and difficult, despite the fact that only around 6% of UK land mass is actually built on.

Why planning reform won’t solve the problem

Perhaps because land speculation is so rampant in Britain, the planning system is currently painted as the big bad wolf of the housing crisis amongst conservative thinkers. There is a belief that the land market will magically start behaving like any other free market if we scrap the 1947 Town and Country Planning Act. But for all its flaws, the planning system is not the fundamental issue here, even if there is a genuine case for planning reform.

In Victorian Britain, slum housing, rising rents and overcrowding plagued the Capital and other areas of rapid economic growth. This had nothing to do with rules and regulations (which were next to non-existent), and everything to do with the power that comes with land monopoly. The poor got poorer and the landed got richer: ‘twas ever thus.

We need to keep talking about land and credit

The only way to permanently stop the price of property ballooning out of all proportion is to tax the land beneath it. A land value tax could replace council tax (a ‘highly regressive’ policy that falls hardest on the least well-off), business rates and Stamp Duty Land Tax, and would disincentivise land speculation. It could raise much-needed revenue for public services hit by austerity cutbacks. Or it could even be redistributed in the form of a ‘citizen’s dividend’ or Universal Basic Income.

This idea has garnered support from across the political spectrum, but has traditionally been opposed by governments beholden to wealthy landowners and a predominantly homeowning public. So, since it may take some time to get the electorate to come round to the idea of a land value tax, a more urgent and politically possible course of action would be to reform the land acquisition process, so that local authorities can afford to build genuinely affordable social housing at scale.

In addition, the Right to Buy policy must be scrapped immediately to stem the loss of social housing – especially given that nearly half of the homes sold are ending up in the private rented sector and contributing to the soaring cost of housing benefit. The shortage of genuinely low-cost homes is acute; the number of people stuck on social housing waiting lists stands at well over 1 million.

For too long, spiralling house prices have been dismissed as an inevitable force of nature, or the product of too little housebuilding, or too much immigration – even though research from the Bank of England has concluded that the quadrupling of house prices over the last 40 years is ‘more than accounted for’ by falling interest rates. It may be dry, knotty and difficult to fit into a soundbite. But until we increase public understanding of the land and credit feedback cycle, the housing debate will only keep going around in circles.

Chloe Timperley

Author of “Generation Rent: Why You Can’t Buy a Home (Or Even Rent a Good One)”. ORDER: http://bit.ly/2AX2LhE

Chloe’s professional background is in financial planning, which involves analysing pensions and investments. This led her to delve into how the financial sector sits at the heart of Britain’s housing crisis. During her research, Chloe went undercover at landlord events, spoke to MPs and activists, and joined a tenants’ union.

She also listened to the stories of scores of tenants who — like her — remain stuck against their wishes in the private rented sector.

Now, she wants to shift the housing debate away from simple narratives of supply vs. demand, and towards the underlying mechanisms that drive our dysfunctional land and housing markets.