On the 6th August 2020 the Conservative Government announced a change to the standard method for calculating the housing need requirement. The debate had up until this point shifted from the ‘numbers’ question. Towards the ‘how’ and ‘where’. Now the proposed new method seeks to achieve a ‘fair share’ under Boris Johnson’s ‘levelling-up’ agenda. But is this the right approach?

The Government’s housing targets have come under fire for contradicting its ‘levelling-up’ agenda.

Recent claims by the Local Government Association (LGA) argue the proposed new standard method would seriously jeopardise the Government’s ‘levelling -up’ agenda.

While the Campaign to Protect Rural England (CPRE) said “the last thing we need is another ‘mutant algorithm’ – this time deciding where development takes place”. We have seen from the exams fiasco the damage that can be caused by erroneous calculations.

Backlash has also come from within the Conservatives. Neil O’Brien, MP for Harborough (Leicestershire), claims “it would be quite difficult to explain to Conservative voters why they should take more housing in their areas to allow large Labour-run cities nearby to continue to stagnate rather than regenerate”. Neil had written for Conservative Home. He argued the new formula would “level down our cities, not level up”. Yet we know large parts of existing suburbs in England and Wales are providing almost no new homes. Tory shires staying untouched? Evidently delusional.

Analysis by the LGA found under the new formula lower growth in housing stock would be expected in Northern regions. London on the other hand would see a 161% rise in homes built. An increase of 57% is expected in the South East. 39% in the South West. For those in the North East proposed targets are 28% lower. While 8% lower in the North West.

On average the house price-to-earnings ratio across the UK stands at 10.7. However, price-to-earnings ratios are still below their previous 2007 peaks in the North East, North West, Yorkshire and Humber, and Wales. In London, the price-to-earnings ratio has worsened by over 50% since 2008. Similarly, the South East, South West, East, and the East and West Midlands have all surpassed their Pre-Covid19 crisis peak. Surely adopting this approach makes sense for these targets to be reduced. Or does it?

On new projections the housing targets are well below what we really need, and fall short in basic economic terms.

On the new proposed standard method it is estimated to be 337,000 – so an annual increase of 1.4%. Currently the Tory housebuilding target of 300,000 accounts for an annual increase of 1.2%. Compared with the two decades between 1931 and 1951 housing stock grew on average at 2.85% per year.

Labour should be attacking the Tories over their lack of ambition. To achieve the levelling-up agenda we need greater supply responsiveness to house prices and housing stock to grow faster than incomes. Only then will we achieve a less volatile housing market. But how could we achieve this?

The Bank of England targets inflation at 2%. As at April 2019 the total number of dwellings was 24.4 million. In effect to ensure growth in housing stock exceeds growth in full-time earnings. Thus, we should be setting the national target closer to 490,000. Somewhat 45% higher than the Tories current level. If we achieved the growth in housing stock at rates seen between 1931 and 1951 this figure would be closer to 696,000.

The average house price-to-income ratio now stands at a whopping 18 times the average salary in London. In London housing supply targets have either been based on land capacity. As seen in the recent Draft London Plan. Or in times gone (and still to date) by projections based on ‘nonsense demographics’.

It makes sense for the Government to require those areas that are seeing the most demand. And demonstrably so in areas that have increasingly high price-to-earnings ratios. Even the North West, North East, and Wales have seen increases in price-to-earnings ratios from their Pre-Covid19 crisis trough. Housing supply should remain an important policy concern for all when considering the ‘levelling-up’ agenda.

It is no surprise why house prices have rocketed in London, the growth in housing stock has not exceeded incomes.

For the period 2009 to 2019 housing in London stock grew by merely 8.6% in aggregate (0.8% p.a.). While full-time earnings grew at 16.9% (1.6%). Almost double the rate. A ten-year target set at the anticipated growth rate in wages, using the inflation rate as a proxy, would see London housing stock need to grow by 2% p.a. or 21.9% in aggregate.

By the end of 2019 London the total number of dwellings across all the tenures reached 3.6 million. London would need 786,700 net additional stock delivered over the following decade. Sadiq Khan would need to increase his original annual target from 65,000 homes per year up to 78,700. This would see London take its fair share of the levelling-up agenda.

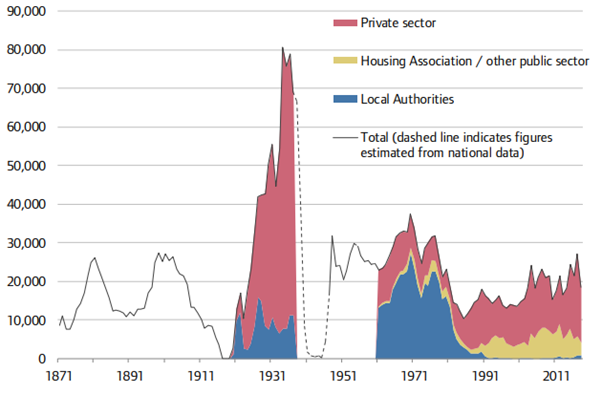

London has not seen such levels built, largely by the private sector may I add, since 1935. This is a time that pre-dates the permanent protection of London’s antigrowth local land regulation, namely the ‘Green Belt’. And the tortuous Town and Country Planning Act, which has poisoned London’s well of supply ever since.

Figure 1: New build homes in Greater London, 1871 to 2018

Sadiq had his own target reduced by the naysayers. An independent review said his small-site target was unachievable. This reduced the original target of 65,000 to 52,000. Still more than Boris Johnson’s 41,882. Yet considerably lower than the proposed new standard method of 93,532. A figure London has never built in its history.

Targets set under the Housing Delivery Test (HDT) over the three years between 2016 to 2019 required one home for every 80 residents on average. Or 38,400 annually. Output would need to increase by 200% to increase housing stock at the same pace as income to hit a target of 78,700. Or 243% to hit the levels set out using the proposed new standard method.

The race to the bottom of build cost and quality is a symptom of a broken land market.

The endemic cladding scandal has left over 3 million in worthless flats. Economic incentives of landowners under the current planning system have led to economic growth and value from cost cutting measures absorbed by land values. The result? A race to the bottom on build quality to pay the highest price.

Our land market has been so constrained that the economic interests driven by the current planning system has seen build quality deteriorate. Literally to the point where basic fire safety has too often become hard to achieve.

Housing targets under the Tories remain a tabula rasa, only Labour has the ambition to level up our nation.

Levelling-up the land market requires planning reform and appropriate housing targets. And densifying cities. Only then will we re-balance the see-saw between land values and build quality. Liberal socialist John Rawls has advocated a move from a broken system of welfare state capitalism, to a property-owning democracy. Where everyone can participate in the productivity gains of a nation.

If every British citizen had a stake in a sizeable amount of property, access to capital and the productive decisions of society, then we can put power in the hands of the many and not the few. In China, the homeownership rate is as high as 90%. We should try to emulate this ambition. And while no silver bullet, revolutionary rent-to-buy schemes such as Rentplus could provide one such solution.

The levelling-up agenda will require a significant amount of homes at social rent levels for those on low-incomes. Particularly in big cities. Labour needs to ensure housing targets are driven on the premise we need to make homes more affordable. This can only be achieved by committing to more supply. And a huge, huge amount of it.