Today there are 4.2 million people in need of social housing in England including people living in overcrowded, unsuitable and unaffordable homes or homeless. We are in a housing emergency, caused by years of cuts and short term piecemeal policy decisions. What the social housing sector urgently needs to be able to tackle the housing crisis is long term certainty – both in policy and funding.

Only a few months into power, the new government has already been promisingly vocal on housing. Secretary of State, Angela Rayner, has announced an overhaul of the planning system, reintroduced more ambitious mandatory housing targets and recognised the role of social and affordable housing in achieving the government’s ambition of building 1.5m homes over this parliament.

Housing associations are ready to play their part in making this happen, but they’re starting from a fragile financial position. For starters, successive rent freezes and caps mean that rental income is 15% lower in real terms than it was in 2015; this equated to £3bn in lost rental income for housing associations last year. Alongside this, the sector is also facing significant financial pressure from building safety costs. Since social housing doesn’t have access to government building safety funding, housing associations estimate they’ll need to spend in excess of £6bn making all their buildings safe over the next decade. Last year, housing associations increased investment in their existing homes by nearly 20%, spending a record £7.7bn on repairs and maintenance.

All of these competing pressures, on top of direct cuts to funding for new homes, has inevitably led to a reduction in plans for building new affordable and social housing at a time when they are needed more than ever.

Earlier this year, the Levelling Up, Housing and Committee’s report into the finances and sustainability recognised these financial barriers. For housing associations to have the confidence to plan for the future and help the government meet its ambition of building 1.5m homes, certainty of rental income and urgent funding is needed at this year’s Autumn Budget and Spending Review.

A new Affordable Homes Programme would be pivotal in supporting the social housing sector to build the number of homes the country needs. Ideally this would shift focus towards social rent, with greater flexibilities around grant rates and funding for regeneration. To deliver the step change needed in the delivery of social housing, a new Affordable Homes Programme would need to provide £4.6bn of funding per year on average for the first Parliament, on a minimum five-year rolling basis.

The Warm Homes: Social Housing Fund (formerly the Social Housing Decarbonisation Fund) is also playing a crucial role in helping the country to meet its net zero targets. However the sector will need to invest up to £50,000 per home by 2050 to ensure they are safe, high quality, decarbonised, and meet new regulatory requirements. The introduction of a new long-term Social Housing Investment Fund of £2bn per year would allow housing associations to continue their vital work in ensuring their homes are sustainable and fit for the future, while unlocking capacity for the supply of new homes.

There is also a crisis in supported housing which provides homes with support, supervision and care. NHF research shows that one in three supported housing providers have been forced to close services such as women’s refuges, homeless hostels, and older people’s housing over the past twelve months, due to the worsening impacts of funding cuts and rising costs. Without supported housing, an additional 71,000 people would be homeless or at risk of homelessness, we would need 14,000 more inpatient psychiatric places, 2,500 additional places in residential care and 2,000 more prison places. That’s why the government must reinstate ring-fenced funding for housing related support, with at least £1.6bn per year of funding, to ensure the continued viability of this vital provision.

Uncertainty around rents has also stopped housing associations from effectively planning for the future. A commitment from the government to a 10-year rent settlement would give social landlords the certainty they need to plan investment over the long-term while ensuring social rents remain affordable for residents. Alongside this, widening access to the Building Safety Fund to cover social housing, would help relieve the some of the financial pressures so many housing associations are facing.

The beginning of a new parliamentary term is the best time for bold action and long-term thinking, and that’s exactly what is needed for the government to be able to meet its housebuilding ambitions. Housing associations are ready to work with the new government to build the affordable homes the country needs and end the housing crisis for good.

Councillor Dave Ward returns from Kosovo with lessons in development finance. He argues that allowing the land and development supply chain to share in the upside of apartment sales can lower the barriers to entry for smaller housebuilders.

I have just returned from Pristina, Kosovo where I got my new apartment ready for a summer rental to a couple of German students who are volunteering there for the summer and needed a place to stay.

As Chair of Planning at the London Borough of Merton, I am always interested in housing and planning policy, particularly around building new homes and it was very interesting to see and learn about the differences between the UK, specifically London, and Pristina.

Firstly, the scale is a lot smaller, Pristina is a city of nearly 150,000 people, just over eight per cent of the total 1.8 million population of Kosovo, and growing. This quite closely compares with London’s 7m people, roughly 10% of the total population of the UK.

So both cities are the centres of government, the financial sector, the media and the headquarters of many national and international businesses and other organisations. As in London this attracts a higher population as people come to the capital for work, which then leads to housing pressures.

Pristina is in the middle of a housebuilding boom. The block where I now live (for some of the year) is ten storeys, with roughly 60 apartments varying in size from small studios to three-bed apartments. It is one of at least eight similar blocks, either completed or under construction, just within a few hundred metres, in an attractive location just ten minutes walk from the city centre.

The most interesting thing I discovered about housebuilding in Pristina is they way it is financed which is very different from the UK. Typically a developer will find some land upon which a block could be built, purchase it from the original landowner, pay contractors to build the block, and suppliers for the materials, then when it is complete, sell or rent the homes and try to make a profit, just like here.

The difference is that the original landowner, contractors and suppliers are often paid, at the end of the project, in completed properties.

For example, the company which supplies the concrete struts which form the frame of the building might, instead of cash, upon completion of the project receive a floor, 6 or 8 properties which they can sell, keep or rent as they wish. The same for the building contractors, glaziers and anyone else involved in the project.

I was surprised at this and wanted to know more so, as I was due to meet the owner of the company which built the block I live in, I asked him about it.

His company usually funds around half of the construction costs of a new development in this way. It is kind of a loan, without interest, but it is more expensive. He estimates that building a new block of apartments would be 5 to 10 per cent cheaper if paid up-front in cash. This is a compensation for the contractors, for instance a building firm. They need to pay their workers, purchase the materials and do their work, paying up-front, on the promise of a number of properties upon completion, not knowing for certain what they will be worth at that stage. They are taking much of the risk, and therefore take a higher return.

This model is used widely in Kosovo and has been borrowed from nearby Turkey where this has been the norm for development for some time.

The practical implications of this are that housebuilding is slightly more expensive, but easier to do for those without huge amounts of up-front capital. So building is not dominated by large developers funded by the major banks or the very wealthy. A relatively small company, such as the family firm which built my block, can get into the housebuilding business and deliver new homes from very small beginnings.

Property prices and rental values in Pristina are, like London, higher than the rest of the country. They are much lower than London in actual terms, but also lower in relative terms compared to average income, wages and cost of living in Pristina. Housing is genuinely affordable for those on modest or low incomes.

To rent an apartment like mine – 2 bedrooms in the centre of town – a single person would need a salary around the middle range in Pristina. A couple sharing would find it more affordable. This is for a sought-after area near the centre of town. Move a few miles out, a bus ride from the centre and rents and prices become comfortably affordable for the lower paid.

Could this be replicated in full or in part in the UK? Could we open up housebuilding to smaller entrepreneurs, to housing associations, non-profit organisations, and to Local Authorities to build new housing, without the need for huge amounts of capital up front?

I think it is worth looking into.

Dave Ward

Dave is a Labour Councillor in the London Borough of Merton where he is Chair of the Planning Committee. He represents the ward of Colliers Wood.

Those on lowest incomes face rising costs without new provision, long-term grant funding for new homes is needed now more than ever.

The rising inequalities associated with the lack of affordable housing are becoming hard to ignore. Whether a tenant or a homeowner, housing expenses take up a large part of household’s earning each month and hence the pressure rises on political leaders to do something about it.

The latest ONS data[1] reports that “households whose income is in the bottom 10% could expect to spend more than two years of disposable income on the upfront costs of an average house in London, the South East and the East of England” and “could expect to spend more than 70% of disposable household income on mortgage repayments for an average property in England”. On the rental market, households in the bottom 25% of the income distribution could expect to pay more than 30% of their income on the cost of renting an average property.

Double or quits report highlights the need for long-term grant funding

Building housing that is affordable is not straight forward. As with other types of social infrastructure, positive externalities may be hard to capture, and this justifies government subsidies into the supply of affordable housing. Government grant is essential to incentivise the provision of affordable housing tenures.

Since the introduction of the Housing Act 1988, the Government has largely provided grant on a short-term basis, mostly aligned with the political cycle. This short-term approach to grant funding leads to high levels of uncertainty and cyclicity on the housing market. I highlight this in a recent report called Double or Quits: The influence of longer-term grant funding on affordable housing supply. It was commissioned by the Consortium of Associations in the South East (CASE)[2], The National Housing Federation[3] and Shelter.

The report finds that extending the length of capital grant, all else equal, would add certainty in the development process and reduce development cycles. This in turn may lead to more housing provision.

Grant funded affordable housing has been on a downward trend

Double or quits starts off by conducting an extensive overview of the grant arrangements and outputs over the last three decades. Up until the late 1980s, local authorities were the main provider of affordable rental accommodation, when grant for affordable housing took a downward trend[S1] . In the last three decades, housing associations, or so-called registered providers (RPs), have been the main players in the affordable housing provision. RPs use capital grant to bridge the shortfall between the total cost of construction including private borrowing costs and revenues from the, so called, cross-subsidy[4].

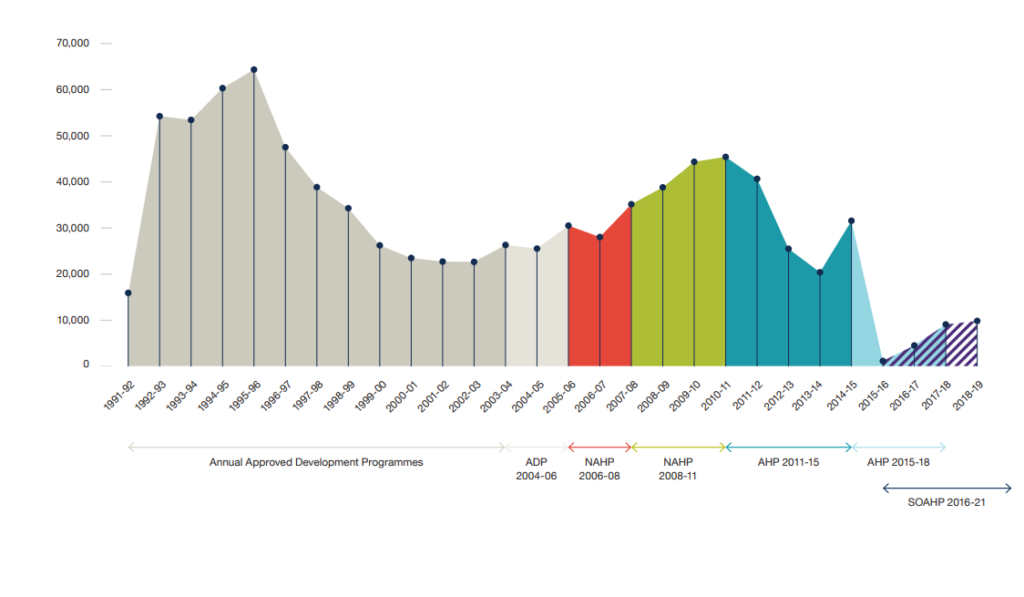

The Affordable Homes Programme (AHP), which has been the primary mechanism by which Government has funded new affordable homes since 2011, has provided funding on a three- to five-year basis. Table 1 shows the various capital grant schemes available since 1991. Each colour represents a grant cycle – from the beginning of the grant to its expiry. It is clear that towards the end of each grant programme, the output increases as the grant has to be spent by the cut-off date.

Figure 1: Private Registered Providers’ Homes England / GLA funded affordable completions

Source: Ministry of Housing, Communities and Local Government (MHCLG), 2020.

Development for social rent has been on a rapid decline since 2011

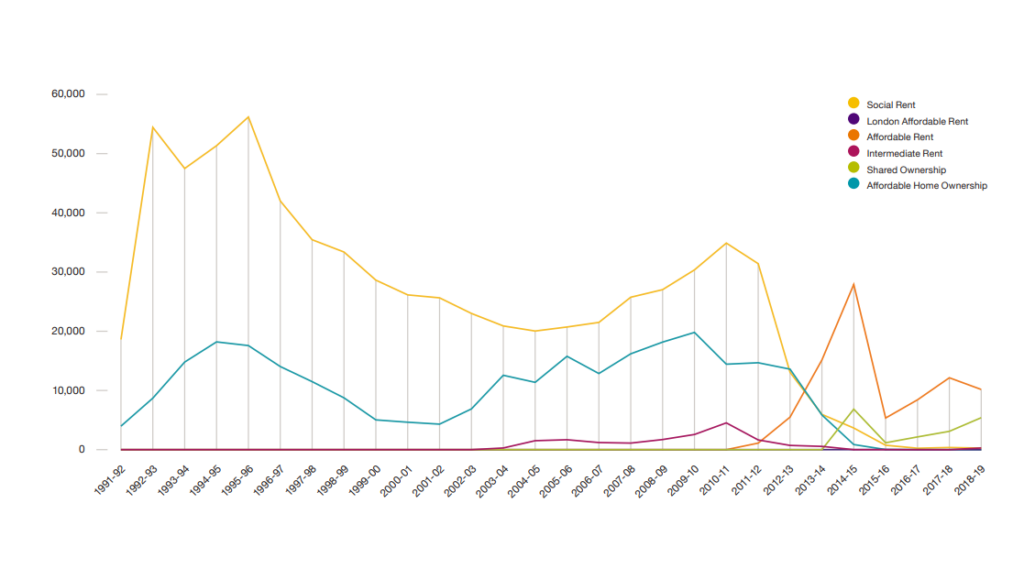

Affordable housing completions can be subdivided into four main tenures, as defined by the government, social rent, affordable rent, shared ownership and intermediate rent. Figure 2 shows the affordable housing completions by tenure for England between 1991 and 2019. 2010-2011 marks an important shift in the provision of affordable housing with the introduction of a new tenure – affordable rent. Completions of social rent have rapidly declined since 2011, from around 40,000 units per year to less than 10,000.

They have been replaced by a new tenure[S2] . While the average grant per dwelling has been around £50,000 between 2006 and 2011, covering about 40% of total construction costs, it has dropped by more than half between 2011 and 2018. That led to housing associations delivering from around 50,000 social rent and shared ownership units in 2011 to less than 6,000 in 2019. The latest figures by the Ministry of Housing Communities and Local Government report total affordable housing completions of 57,185 as of the end of 2019, half of which are affordable rent.

Figure 2: Affordable Housing Completions by Tenure for England

Source: MHCLG, 2020.

Significant rise through developer contributions obtained through Section 106 Agreements

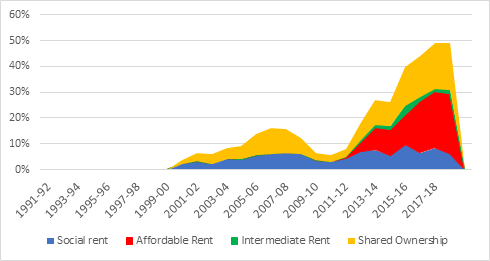

Since around the same time as the decline in social rent completions, most of which are delivered by housing associations, in 2011, there has been a huge rise in the share of completions associated with Section 106 (S-106) planning agreements. This is evident in Figure 3 below.

Planning obligations under Section 106 were introduced in the Town and Country Planning Act of 1990. They are ‘developer contributions’, similar to highway contributions and the Community Infrastructure Levy, partially provided for affordable housing. This means that there has been a shift in the sourcing of funds for affordable housing provision. Now, only about 50% of the funds come from the grant provided by Homes England (HE) and Greater London Authority (GLA).

The reliance on private development to deliver affordable housing through S-106 contribution has been greater than ever. This has been enabled through the substitution of social rent by affordable rent and shared ownership. The striking picture depicted in Figure 3 makes clear the direct positive relationship between affordable housing supply and market housing supply. If, following a slow-down in economic growth, development activity drops by, i.e. 30%, the provision of shared ownership and affordable rent may drop by a similar proportion, since 30% less S-106 provisions may be made.

Figure 3: Share of Completions by Tenure as Part of Section 106 (S106) Agreements

Source: MHCLG, 2020. Data for England.

Lack of predictability of grant big issue say developing housing associations

Given the trends described above and the reliance on the market to supply affordable housing, the report goes on to investigate how increasing the length of the housing grant to 10 years could affect the provision of affordable housing by conducting structured interviews with 13 Chief Executives or development directors of housing associations.

The lack of predictability in grant provision may lead to a more cautious approach by housing associations when it comes to building their development pipelines and limit the number of affordable homes they deliver. The pronounced peaks and troughs in delivery associated with the short grant cycles, with completions skewed towards the end of Programmes, have knock-on consequences for development costs, build-quality and the productivity of the housebuilding industry.

The report finds that a ten-year Affordable Homes Programmes would enable housing associations to purchase more sites without planning permission and take on larger and more complex sites. This may lead to reducing overall construction costs and passing the savings on to the homeowners or tenants.

Land-led development by housing associations would become more prevalent

Housing associations will be more likely to invest in their in-house development teams and intensify relationships with private developers, house builders, land managers and local authorities, including through joint ventures. This can lead to consolidation on the market and economies of scale in the production of new affordable housing.

Furthermore, a move to long-term funding would also increase housing associations’ ability to fulfil deliver affordable housing counter-cyclically. It would do so by accelerating the trend for greater levels of land-led development, whereby housing associations act as the lead developer on sites rather than acquiring homes from private developers via S106.

This would enable housing associations to build up longer and more consistent pipelines of development sites, which would help avoid some of the pronounced peaks and troughs in delivery that have been associated with previous Affordable Homes Programmes.

Resilient funding provisions for affordable housing should be a high priority for Government

Due to the strong dependence of housing development on economic cycles, as outlined above, the risk of taking a market approach to affordable housing is that affordable housing supply may become more volatile and pro-cyclical.

As we are experiencing in the current Covid-19 economic downturn, having a safe and affordable place to live is a key necessity for every human being. It is in periods of downturn, that households are more likely to lose their job, become evicted and struggle to afford housing. Having a resilient provision of affordable housing, for those most in need during downturns, should be high on the priority list of the Government.

Dr Stanimira Milcheva

Dr Stanimira Milcheva is an associate professor in Real Estate and Infrastructure Finance at University College London. Stani’s research is broadly in the field of real estate and infrastructure finance. She also works on topics related to affordable housing.

[2] CASE is a group of 10 major housing associations providing affordable homes in the South East of England. Collectively, members own more than 400,000 homes across the country, with over 140,000 in the South East. The members of CASE are: L&Q, Metropolitan Thames Valley, Moat, Optivo, Paradigm, Radian, Sovereign Housing Association, The Guinness Partnership, The Hyde Group and West Kent Housing Association.

[4] Cross-subsidy is model in which the profits from the sale of market housing are used for the construction of affordable housing, including tenures like social rent.