By Dave Treanor*

The business model on which housing construction is funded is broken. It is slow to respond to rising house prices by increasing the supply of new housing, and stalls at the first sign of a downturn in the housing market. At the heart of the problem lies a failure in the market for potential building sites.

Construction companies have responded to the unpredictable nature of our planning regime by acquiring land banks so as to ensure a steady supply of sites to develop. Land banking enables them to increase their market share in housing construction and limits the supply of new housing from competitors that might undermine the prices they can obtain. As a result, the availability of building sites barely responds at all to rising house prices.

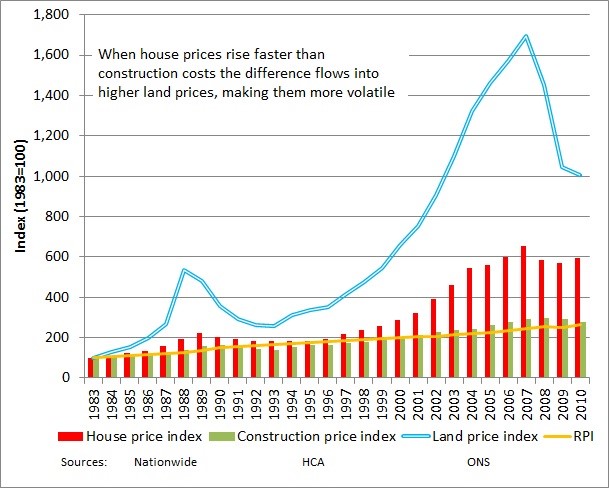

Developers profit far more from speculative gains in land values than the construction of housing. The reason is quite simple: if property prices rise by more than the cost of construction that increase flows through to the value of the land, which rises in price by far more than the housing. The corollary is also true: if property prices fall land prices will fall by a far greater amount. That is what happened following the financial crash, putting many out of business and allowing the stronger firms to buy out the weaker ones, largely to benefit from their land banks.

In a rising market why sell today when the land will be worth more tomorrow? In a falling market the bigger construction companies consolidate their control over potential building opportunities. It is never in their interests to release newly constructed homes at prices below those they expected when they secured the land several years previously, or in sufficient quantities to lower the prices being paid.

Much of Europe and some parts of the USA and Australia tackle this by levying an annual tax on the value of land, making land banking less profitable. There are lessons to be learned from previous attempts by Labour governments to tax these speculative gains.

Betterment Charge in 1947

Labour first introduced a ‘betterment charge’ in the 1947 Town and Country Planning Act. The right to development was made a state monopoly, and the increase in value resulting from planning permission was taxed at 100%. This was seen as politically more acceptable than the nationalisation of land. Landowners responded by holding on to sites in the expectation that the Act would eventually be repealed, which it was when the Conservatives were elected in 1951.

Land Commission Act in 1967

Labour had another go with the Land Commission Act of 1967. This empowered local authorities to acquire and hold onto land so that it could be subsequently developed, capturing the resulting gains. This worked well with quite a few councils actively engaging in land assembly to promote area regeneration. It also introduced a ‘betterment levy’ charged at 40% of ‘net development value’ calculated as the increase in land value resulting from the development. The result of the levy was much the same as with the previous betterment charge: it cost nothing to hang on to the land, which invariably increased in value by far more than any holding costs. The supply of sites dried up and the Act was repealed as promised by the next Conservative government in 1970.

Development Land Tax in 1976

A Development Land Tax was introduced by the Labour government in August 1976 through the Community Land Act. This taxed development gains on the disposal or ‘deemed disposal’ of land. It was levied at 80% of the gains realised. The Act included 94 pages of complex calculation with numerous exemptions and allowances. The Conservatives promised to repeal it; but they were willing to go along with the Development Land Tax if it was nearer 60% instead of 80% to 100%. When they came to power in 1979 they initially reduced it to 60% and then Nigel Lawson abolished it in his 1985 Budget[1].

S106 of 1990 Town and Country Planning Act

It was the Conservatives who introduced section 106 of the 1990 Town and Country Planning Act. The idea was to capture some of the increase in value when planning permission was granted, and use this to fund the inclusion of affordable housing in the development and improvements to local transport infrastructure and schools to deal with growth in the local population.

The Greater London Council under Ken Livingstone made very good use of this to leverage additional social housing in London. The last Labour government incorporated it into the grant funding regime for social housing. It achieved many of the same objectives as the earlier failed policies, and with a little tweaking to deal with some of the abuses that have crept in it could continue to work well.

Following the financial crash in 2009 housing construction ground almost to a halt. The big construction firms, which are amongst the largest donors to the Conservative Party, persuaded the government that the only way to get house building going again was to boost demand with lower interest rates, ‘Help-to-Buy’ schemes, and by reducing the obligations on which planning permission was granted. All that achieved was to increase house prices, while construction remained in the doldrums. In the four years before ‘Help to Buy’ new house building in London averaged 42,392 a year. In the four since ‘Help to Buy’ it fell to 35,274 per year. London house prices rose 48% since it was introduced in 2013.

S106 negotiations are based on a financial viability appraisal to assess how much affordable housing a site could sustain whilst remaining profitable to develop. These assessments were politicised by the Coalition Government (under Eric Pickles) which introduced a six-year window whereby developers were encouraged to use the viability assessment mechanism to challenge s106 agreements made prior to the financial crash. It established 20% as the profit a developer could reasonably expect to make.

In a competitive market a developer that is adept at minimising the affordable housing obligation can bid at a higher value and is more likely to secure sites. Developers run rings around councils in negotiating planning permission (1).

Part of the problem is that a council’s negotiating position is open to public scrutiny while the financial viability assessments used by developers to argue for a reduction in the requirement are treated as commercially sensitive. This really is nonsense: only the owner of the land could benefit by applying for planning permission and they do so without competition from any other developer who might be able to offer more affordable housing. The truth is it strengthens their negotiating position if the council’s calculations are public and theirs are kept private.

A number of planning authorities now require developers to openly publish any viability assessment they use to argue for a reduction in s106 obligations. Under the London Mayor’s Supplementary Planning Guidance (SPG), instead of local authorities having to prove a scheme is viable with 35% affordable housing, the developer has to justify where it is not. Any development has to be profitable, but if a developer overpays for a site by discounting the requirement to include affordable housing, that is their problem. The aim is for the requirement to provide 35% affordable housing to be fully reflected in land prices. The obligation can only be challenged where the value added though granting planning permission is insufficient to fund the affordable housing requirement. The planning gain against which this is assessed is the difference in Existing Use Value with or without the change in planning status, and not the price the developer paid for a site.

Once viability assessments are opened up to public scrutiny planning authorities will be in a position to benchmark the assumptions being used against comparable schemes elsewhere, introducing a genuine element of competitive pressure into the negotiations.

Land Value Tax

Land value tax is widely seen by economists and housing experts as the most effective solution in the longer term, and was recommended by the Mirrlees Review on reforming the UK tax system. It would replace council tax and business rates with an annual tax on the value of land, based on its potential use in accordance with a Local Plan. It would be levied on the residual value of the land net of the construction cost of any buildings. It is more progressive than Council Tax, and could lay the foundations for a shift towards taxing wealth.

It tackles not only the issue of speculative gains in land values – but also the practice of land banking itself. It has been successfully implemented in France, Denmark, Belgium (Flanders), Spain, Finland, Estonia, Bulgaria and Hungary in various forms (2).

The council tax regime is dated and ripe for change. But any change to the system of raising local taxes is fraught with difficulties, and many previous reforms have floundered. There would be a number of practical challenges to overcome as well as the political risk from ‘winners and losers’ created by the change.

A report to the London Assembly recommended enabling legislation that would allow a planning authority to trial the introduction of Land Value Tax so as to flush out and deal with the difficulties. This was reflected in the Labour Manifesto for the last election which said “A Labour government will give local government extra funding next year. We will initiate a review into reforming council tax and business rates and consider new options such as a land value tax, to ensure local government has sustainable funding for the long term“.

Dave Treanor

*Dave researched ‘Housing Policies in Europe’ having retired from M3 Housing and the National Housing Maintenance Forum, where he produced development appraisal systems and the NHF Schedule of Rates. This is his first piece for Red Brick.

Notes

1. The economist V H Blundell put the failure of these measures down to:

- Being too complex and riddled with anomalies and unintended side-effects

- A failure to incentivise landowners, provoking resistance and inertia, discouraging development and leading to the hoarding of land

- The big mistake was to levy it on development rather than as a general tax on land value.

2. Dave Treanor: ‘Housing Policies in Europe’ 2015 available as a book or a free download here.

7 replies on “Taxing speculation in land”

Reblogged this on nearlydead.

Excellent article, many thanks!

The Housing and Communities Select Committee have started an inquiry into land value capture http://www.parliament.uk/business/committees/committees-a-z/commons-select/communities-and-local-government-committee/inquiries/parliament-2017/land-value-capture-inquiry-17-19/commons-written-submission-form/

Submissions by 2 March and all of this post should be of interest to it.

Excellent and helpful analysis. Thanks.

[…] [8] https://redbrickblog.wordpress.com/2018/01/24/taxing-speculation-in-land/ […]

[…] on the land question done by others in the recent past and covered on Red Brick, see Dave Treanor here, London Assembly Housing Committee here and Josh Ryan-Collins, Toby Lloyd and Laurie Macfarlane for […]

[…] on the land question done by others in the recent past and covered on Red Brick, see Dave Treanor here, London Assembly Housing Committee here and Josh Ryan-Collins, Toby Lloyd and Laurie Macfarlane for […]