The Affordable Housing Commission, organised by the Smith Institute, funded by the Nationwide Foundation and chaired by Lord Richard Best, has issued a call for evidence as it gets under way. It poses a number of questions:

What does affordability mean in different areas of the country? How does it link to the welfare system? Why has housing become unaffordable and what are its effects? What policies have been put in place and have they been working? How can supply be increased and what are the roles of the tax system, government funding, housing providers, and the planning system? What other areas of policy need to change – eg infrastructure, institutions, governance, public attitudes?

Most policies on affordability tackle the symptoms and not the causes of the housing crisis. Housing becomes unaffordable when the cost increases by more than earnings. If we fail to understand why this has happened over the last fifty years, we’ll repeat the mistakes of the past. Subsidising housing for those priced out of the market merely tackles the symptoms and will never provide a cure. It often helps one group of households at the expense of others.

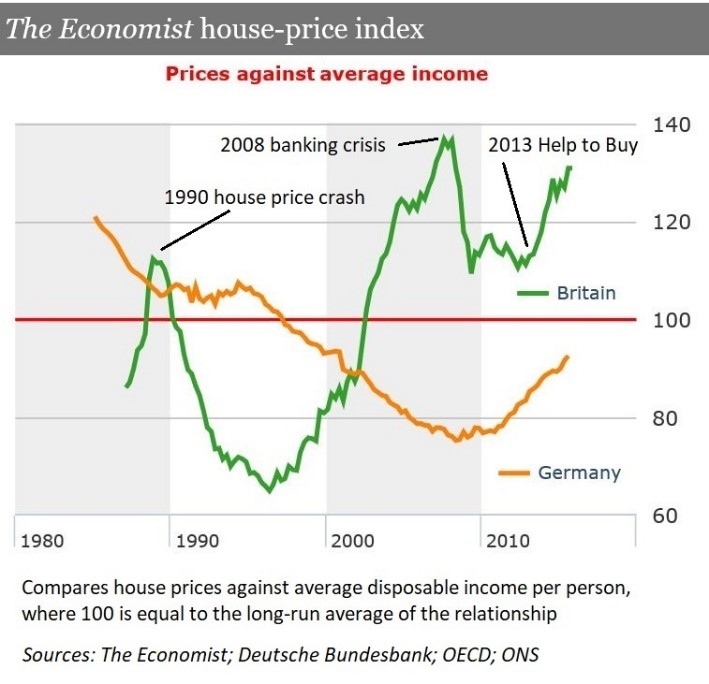

If the workings of the housing market are to blame, why is the problem so much worse in the UK than across most of Europe. Why does the same thing not happen in Germany?

I sought to answer these questions through an in-depth study of housing policies in ten European countries, and wrote it up in Housing Policies in Europe [1] The book contains the evidence behind the conclusions and proposals in this paper, all referenced back to its sources.

Impact of taxation of affordability

Taxation in the UK is more biased in favour of owner-occupiers and against tenants than anywhere else in Europe. This makes a home the most profitable investment anyone in the UK can make. The more they can invest the wealthier they will become. In Germany taxation is almost tenure neutral.

House prices in Germany are more stable than in the UK, and on average across the country have become more affordable over the last thirty years, with prices rising on average by less than earnings. Rented housing is taxed no more heavily than home-ownership. Germans get as good a return net of tax by investing in their industries as they would from buying their own home. This takes much of the heat out of their housing market. It may also help explain the success of German manufacturing.

House prices in Germany are more stable than in the UK, and on average across the country have become more affordable over the last thirty years, with prices rising on average by less than earnings. Rented housing is taxed no more heavily than home-ownership. Germans get as good a return net of tax by investing in their industries as they would from buying their own home. This takes much of the heat out of their housing market. It may also help explain the success of German manufacturing.

In cash terms a mortgage may be just as hard to pay as rent, but unlike rent it is an investment in an asset that rises in value and does so by more than the mortgage payments on it. In most years house prices in the UK rise at a higher rate than the interest their owners pay on their mortgages, and sometimes by more than the total income earned by the household. And yet these gains are completely free of taxation. Rents rise with inflation, and in response to rising house prices, typically doubling every ten years. Mortgage payments fluctuate with interest rates but do not generally rise over time. Once the mortgage is paid off the owner lives rent free. None of this additional spending power is taxed.

Most home-owners would think it outrageous to even think about taxing these gains, and fail to recognise the extent to which they benefit compared with those that rent. This widens the gap between the rich and poor, transferring wealth from the young who generate most of it through their hard work to an older generation that owns most of the housing. The gap between rich and poor is growing ever wider. The biggest gap is found between those owning and those renting their homes. Yet housing benefit is seen as welfare and is being cut and capped, while the wealth tied up in a person’s home is increasingly exempt from inheritance tax.

The best solution would be to tax home-owners on the benefit of living rent free in their own home, as was done until this was abolished in the seventies.[2] Failing that a fair equivalent might be to allow tenants to offset rent against the tax they pay on their income.

Favourable taxation and other subsidies to promote owner-occupation result in higher house prices, benefitting existing owners at the expense of those less fortunate, adding to affordability problems.

Stamp duty which is paid by the buyer should be replaced with capital gains tax paid by the seller of a property. Tax the one making the gain, not the one struggling to climb the housing ladder. The lack of tax on these gains inflates prices higher up the ladder. Stamp duty discourages mobility and is a disincentive to down-sizing, whereas a tax on capital gains would only be incurred to the extent the property had increased in value, and the liability would be triggered but not increased by the transaction.

Inheritance tax rules also discourage the elderly from downsizing, by shielding part of the value of their residence from taxation.

Private rental sector

Private rental tenancy terms in the UK are amongst the worst in Europe, making home-ownership the only sensible option, adding to the demand putting pressure on house prices.[3]

Tenants in the UK are treated with very little respect. How can anyone make a home in a property where the landlord can repossess at two months’ notice?

There are a number of reasons why housing in Germany tends to be of better quality and more affordable than the UK. There are few circumstances where a tenant who pays their rent and abides by the terms of their tenancy can be evicted. They take pride in looking after their homes, with more control over repairs and maintenance. It is not uncommon for tenants to upgrade their kitchens and bathrooms by agreement with their landlord who may contribute to some of the cost. In the UK this is only possible where you own your own home. As a result, many middle-income Germans are content to live in rented housing.

Generally, elsewhere in Europe tenants can only be evicted if they break the terms of their tenancy agreement and are often less dependent on a landlord for day to day repairs and maintenance. Many families are happy to live in good quality rented housing, without paying extortionate rents. We must end no-fault evictions. But that is not the whole story.

The way to make housing more affordable is to tackle the underlying causes of house prices rising faster than earnings. That requires long-term changes in housing policy, much longer than our electoral cycles tend to promote. The poorest will always suffer the most from any shortage and require additional help, but focussing all subsidies at the bottom end of the market deepens the poverty trap. Subsidies to help the poorest tenants enable them to pay higher rents, raising costs for those that just fail to qualify. Solutions are required that impact across the whole of the housing market.

The German approach to social housing has also played an interesting role, and could hardly be more different from council housing in the UK. None of it is intended to remain as social housing forever. In return for subsidies from local, regional or central government to deal with a shortage of affordable housing, new homes are built and let to low-income households from a housing waiting list at no more than 80% of market rents. After an agreed period of between twenty and thirty years the obligation to let at below market rents tapers off. Most of this housing was originally provided by not-for-profit housing companies, some of which were set up by the municipalities.

Much of the privately rented housing in Germany was constructed with subsidies and initially let on social housing terms by a mix of private and non-profit landlords. These were professionally managed on generous tenancy terms, laying the foundations for a much fairer private rental sector. Even so, two-thirds of rented housing is now held by individuals who typically let one or two properties. The rest is provided by a combination of municipal companies, co-operatives and private companies.

The UK is quite exceptional in the proportion of welfare support provided through personal housing subsidies, an unfortunate biproduct of which is to raise market rents, particularly at the lower end of the rental market.

If UK housing associations had invested in secure market rent over the last thirty years, there would now be a substantial stock of well managed housing on which nobody was extracting capital gains. The growth in buy-to-let demonstrates how profitable that would have been. It would have reduced the pressure on rents and improved the choice of housing for those who cannot afford to buy and would never reach the head of the queue for social housing. It is never too late to change.

We should learn from the German experience. It requires little if any subsidy for a social housing organisation to develop secure market rent alongside more affordable options. Some are already doing it on a small scale. I can think of few policies that could have more of an impact at such a low cost. All it needs is the political will to do it and encouragement from those regulating the sector.

Instead, private landlords are blamed for competing with first-time buyers and bidding up prices. They are burdened with heavier taxation, all of which is paid out of tenants’ rents. Imposing fairer tenancy terms would have been a far more effective way of rebalancing competition between first-time buyers and buy-to-let landlords, and less likely to push up market rents. A drop in the availability of rented housing is never going to reduce rents or improve the choices faced by tenants. The few studies of the effect on house prices of purchases by landlords show less of an impact than is commonly assumed.[4]

Excessive borrowing fuels the growth in house prices

If more money flows into the housing market than is spent on construction and renovation it can only have one result: higher house prices. This is true whether it comes through banks’ lending additional money raised on wholesale markets, from parents passing wealth down to their children, or from help to first-time buyers, or from overseas investors finding housing in the UK a safe haven for their money.

Mortgage lending in the UK is relatively unconstrained. Where demand outstrips supply and getting onto the housing ladder is clearly profitable, the amount they will pay is only constrained by how much they can borrow.

Most mortgage loans in Germany are restricted to 80% of the property value, limiting the amount a household can afford to pay, unlike the UK where excessive borrowing fuels the growth in house prices.

With mortgage interest rates at below 3% it soon becomes cheaper to buy than to rent, adding to incentives to climb onto a housing ladder. Saving for the deposit is the most significant constraint.

Quantitative Easing, cheaper credit for banks and reductions in the bank base rate following the financial crash reduced the cost of investment in housing without making it any more affordable: the reduced cost and increased availability of borrowing was all captured by existing owners and developers in higher house prices. Above all it boosted land prices, increasing the pressures on affordability.

Failings in the business of housing construction

The market in potential building sites is controlled by a diminishing number of major developers who control the supply of new housing, and will only build in a rising market.

The supply of land for housing is restricted by planning regulations and constrained by the green belt, so it does not increase in response to rising demand.

In order to ensure a regular supply of sites the construction companies build up land banks, or buy options securing sites on pre-agreed terms. Developers and land dealers assemble potential sites, using their expertise to take them through planning, adding considerably to their value in the process.

The price a developer is prepared to pay is based on the expected value of the properties that might be built on each site over the next ten years. The land market ‘prices in’ the expected increase in property prices.

It should also take account of local planning requirements. But in competing for potential building sites developers become adept at minimising the affordable housing liability, arguing it would make the development unprofitable. They run rings around councils in negotiating planning permission and s106 planning gain commitments.

The latest National Planning Policy Framework (NPPF) includes measures intended to make the viability process more transparent. It clarifies that the land value used in assessing how much affordable housing would be viable should be based on the Existing Use Value of the site under current planning consents (plus a premium to incentivise development), and not the potential value it might fetch in the market taking into account any likely change in permitted use. If the developer overpaid for a site that is their problem. In theory that should ensure that any requirement in the Local Plan to include a proportion of affordable housing is reflected in land prices, ensuring it is deliverable.

But in practice local authorities are also expected to meet targets for the delivery of new housing, weakening their position in negotiating with developers.

Land banking contributes to the problem. If house prices rise by more than the cost of constructing them, the increase in value flows through to the land. When house prices rise by more than expected, land prices go up at an even faster rate. But the corollary is also true: when house prices fall, land prices fall even further. That is what happened following the financial crash in 2009. As a result, many smaller construction companies found themselves in breach of their loan covenants, with insufficient assets to cover their debts. They could not afford to build their way out of trouble, particularly in a housing market where demand had collapsed. This became a great opportunity for the bigger and richer construction firms to buy up the smaller and weaker ones largely for their land banks, giving them ever tighter control over the housing market.

It is never in a developer’s interests to release newly constructed homes at prices below those they expected when they bought the land several years previously, or in sufficient quantities to lower the prices being paid.

The property development companies are some of the biggest donors to the Conservative Party, and persuaded the government that the only way to get the housing market moving again after the financial crisis was to boost demand with lower interest rates, Help-to-Buy schemes, and by reducing the obligations on which planning permission was granted.

All that achieved was to increase house prices, while construction remained in the doldrums. Before ‘Help-to-Buy’ new house building in London averaged 42,392 units a year. Since ‘Help-to-Buy’ it fell to 35,274 per year. London house prices rose 48% since it was introduced in 2013.

What the government could have done as prices rose was to introduce an annual tax on land value to discourage the hoarding of potential building sites. In an optimised market construction companies would buy sites a few months before they were ready to build on them, and the supply of land would become much more responsive to any increase in demand. Construction would be opened up to new building companies, breaking the monopoly of the big players. The profits of developers should derive from their ability to add value through good design and efficient delivery, rather than speculation in property prices.

Capturing hope

More of the unearned profits arising from public investment and planning decisions should be captured for the benefit of the community, rather than going into the pockets of landowners.

Public housing built in the thirty years after the war was largely self-financed from rents and the sales income it generated. Councils built on bombsites, or land bought at slum-clearance prices, with loans financed by the Public Works Loan Board and repaid from rents, requiring little or no subsidy.

New Town Corporations paid little more than agricultural prices for land and repaid their entire borrowing from the added value of the developments. This paid for the delivery of whole towns including their infrastructure, creating 32 communities and housing 2.8 million people. They paid £4.75 billion back to Treasury in 1999 and have since then yielded an additional £1 billion in profit. [5]

All of this was ended by a court case in 1974 that reinterpreted the 1961 Land Compensation Act, requiring public bodies acquiring land through compulsory purchase to pay the ‘hope value’ arising from potential future development on top of the value under its current planning status. In practice this affected all land valuations, and put an end to self-funded new towns and council house building. It also added to the cost of roads, railways, airports and other infrastructure development. It represented a massive transfer of unearned wealth to landowners and led to a massive reduction in public sector housing construction.

The arguments for and against retaining ‘hope value’ in compulsory purchase valuations were explored in a Parliamentary Inquiry that reported in September 2018.[6] Labour proposes to change these rules and establish an English Sovereign Land Trust working with local authorities to buy land at prices close to existing use value. With the ‘hope value’ removed, the cost of building a two-bed council flat in Wandsworth, south-west London, would be cut from £380,000 to £250,000. In Chelmsford it would fall from £210,000 to £130,000.[7]

Previous initiatives by Labour governments to capture some of these gains were thwarted by the owners of potential development sites hanging on to them in the hope that things would return to the way there were following the next election.[8] What we really need is a cross-party consensus. But, council tax is in serious need of reform, and if a Labour government replaced that with a Land Value Tax, an incoming government might find that harder to reverse.

Dave Treanor

[email protected]

[1] See Housing Policies in Europe available as a free download from www.m3h.co.uk/publications

[2] Schedule “A” tax against which they could offset interest on their mortgage

[3] See www.treanor.co.uk/blog/Fixing_our_rental_sector.pdf

[4] ‘Buy-to-let mortgage lending and the impact on UK house prices: a technical report’ by Ricky Taylor, published by the National Housing and Planning Advice Unit (abolished by the Coalition government in 2010).

[5] https://publications.parliament.uk/pa/cm201719/cmselect/cmcomloc/766/76602.htm

[6] https://publications.parliament.uk/pa/cm201719/cmselect/cmcomloc/766/76602.htm

[7] https://www.theguardian.com/politics/2018/feb/01/labour-plans-landowners-sell-state-fraction-value

[8] https://redbrickblog.wordpress.com/2018/01/24/taxing-speculation-in-land/