Mr Bean’s rent policy

If people rent from a council or a housing association, how much rent will they pay? The answer is anything between 40% of local ‘market rents’ (and sometimes less) and 80%. But is there any logic to the system of rent-setting or is it just inept bungling? All the below rent types are available to homeless households and waiting list applicants who get offered a council or housing association rented home, depending on where they live and the luck of the draw.

- Social rent – council (lowest)

- Social rent – housing association (higher)

- London Affordable Rent (higher)

- Council rent at above LAR benchmark (higher again but unclear how high)

- Affordable rent, discounted to c.65% market rate (probably even higher)

- Affordable rent at full 80% of market rate (highest)

One of the criticisms of Labour’s 2002 policy for social rents was that it was based on a strict formula which meant that ‘Whitehall’ would set each and every rent in the country, leaving no room for local factors or landlord (or tenant) choice. Some liked to call it Stalinist, a curious word to describe a policy of the Blair government. ‘Rent restructuring and convergence’ as the policy was known, sought to harmonise council and housing association rents (HA rents were often significantly higher) over time, moving both at different speeds to a ‘target rent’ which was calculated on a mix of house values and regional pay rates. The government held a review of general rent levels which concluded that they were broadly correct at the equivalent of c.40% of market rents. The policy meant that tenants would pay more over time but within a highly structured and predictable policy environment backed by a comprehensive and generous housing benefit system. Most social rents are still based on this formula.

The policy could have been more flexible, but it stood the test of time. Although slow acting, its flaw was the underlying increase in real rents (normally 0.5% or 1% above inflation): over time rents would become less affordable, passing the strain onto the housing benefit system.

Since 2010 a successful but centralised rent-setting system has been replaced by increasing fragmentation descending into chaos for new homes and new lettings. The huge (by anyone’s standards) cut in housing investment in Slasher Osborne’s first Budget – more than 60% – led to the abandonment of the new homes for social rent programme. It was replaced by the abomination of Grant Shapps’ ‘affordable rent’ product at up to 80% of full market rents – impossibly unaffordable for most people and leading to a high dependency on housing benefit (which they then proceeded to cut, putting a vicious squeeze on tenants). Called ‘Orwellian’ by many commentators due to the ‘doublespeak’ of calling something that was unaffordable ‘affordable’, the policy shifted much of the burden of financing new affordable homes from the state to existing tenants.

Of course, the phrase ‘up to 80% of market’ left the door ajar for those who wanted to mitigate the worst impacts of the policy. Some housing associations tried to achieve rents at significantly less than 80% or applied different rates to different size homes to try to keep family homes within reach. Unforgivably, some chose to max their income. In London, even Mayor Johnson realised the policy was ridiculous and approved some schemes at 65%.

Associations were also encouraged or required to enhance their development funds by selling more homes on the open market and by ‘converting’ homes from social rent to ‘affordable rent’ when they became empty and were re-let. Some did as much of this as they could get away with, a few heroic associations refused to convert any social rents.

In a further series of muddled U-turns the government decided to end the ‘convergence policy’ and impose a national rate of rent increase instead. A supposed 10 year rent settlement – increases of CPI plus 1% every year – launched in 2015 was very short-lived and quickly replaced by an annual rent reduction policy of minus 1%, to the anguish of developing providers. Now under May, a new policy has been announced for after 2020 – it’s back to CPI plus 1%.

From the point of view of a new tenant, the system now resembles a roulette wheel played under rules invented by Mr Bean. A new tenant could by random selection get a home at the equivalent of 40% of local market rates or at 80%. The potential impact is obvious: rents for a similar home could range from genuinely affordable to absolutely unaffordable. And I haven’t even touched on the range of ‘intermediate’ tenure rent policies that can be added to the mix.

The new Mayor of London, Sadiq Khan, was left between a rock and a hard place. He was committed to social rents but also wanted to get the maximum funding out of government. Government would never agree to a wholesale return to social rents, so a principled stand would have led to much less overall funding for affordable homes. In the end, Khan and his housing deputy mayor James Murray negotiated a deal which would allow a new ‘London Affordable Rent’ to be charged, based on social rents but significantly less than the national ‘affordable rent’. At its core, Khan’s LAR is set at the target rent that all social rents would eventually move to, but without the long transition. Rents might (on some calculations) be up to 50% higher than normal council rents (but still much less than ‘affordable rent’).

Depending on your political view this is either a clever solution that preserves the principles of social rent or a sell out. I lean towards the former, partly because the Mayor has also ended the practice of ‘conversion’ in his funded schemes, which will keep many more homes in the real social rent bracket and control the activities of some of the more rapacious registered landlords. Whichever way, his is now the regime that underpins rent-setting for new social homes in London.

If you are still with me, the tale has one further twist, brought to light through a freedom of information request submitted by a north London housing activist. This concerns the Mayor’s laudable £1 billion programme of funding councils to build nearly 15,000 new council homes.

But at what rent? The FoI shows that London councils have gone in many different directions. The appalling Westminster did not even bother to apply for any of the money. Some have got funding for new homes which are mainly at social rent, including Newham, Greenwich, Hackney, Haringey and Southwark. Others have gone for rents predominantly at the mayor’s London Affordable Rent, like Brent, Ealing, Hounslow, Islington and Redbridge. And a few, Brent, Harrow, Tower Hamlets, Barking and Dagenham and Hammersmith and Fulham, have gone for some or all of their rents to be above the benchmark rents expected under the LAR scheme. Yet another rent bracket has been created – LAR plus it could be called.

So the outcome is an increasing mish-mash of rent policies which must be bewildering for any potential tenant waiting for a home. One neighbour could be paying twice as much as the other for the same home. In eight years we have gone from a centralised system that had its defects but which at least everyone understood to a system which is totally chaotic and almost random.

From order to chaos or, to adapt a phrase, from Stalin to Mr Bean via George Orwell.

(amended 12/12/18 to correct comment about current rent policy, which is an annual -1% not CPI -1%).

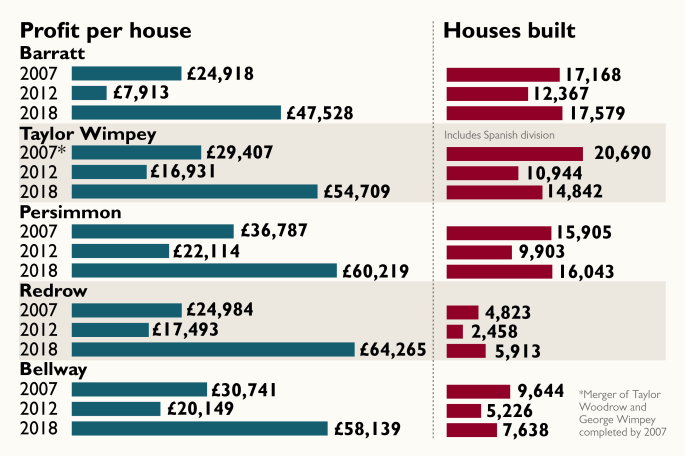

Source: The Times, 8 September 2018.

Source: The Times, 8 September 2018.