Around 53,400 older people chose to live in a retirement village in New Zealand, and 130 people move in each week. This is around 14% of the over-75 demographic nationally and retirement villages have moved from being boutique and misunderstood to a mainstream housing option for older people. For more information about the sector’s growth, market share and development pipeline, see Retirement Villages Market Review | 2024 | JLL Research

Why have villages been so successful? The village promise has four key components:

- A warm, dry, age-appropriate place to live (houses in NZ are often large and expensive to maintain);

- The opportunity to make new friends and try new activities;

- A high degree of financial security (residents know to the last dollar what they pay to move in, know exactly what they’ll get back at the end, and if they’re living in one of the 70% of villages that offer fixed weekly fees, the cost of living in the village will never increase while they’re living there); and

- A pathway to aged care if that’s required. 65% of villages have a care facility on the campus.

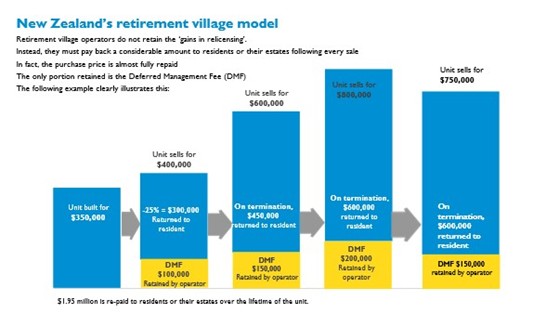

However, this promise isn’t free. The principal business model is called a “licence to occupy” (LTO) and consists of the payment of a capital sum to move in, the payment of a regular fee (often fixed for life) to cover village day-to-day costs, and when the resident dies or moves to care, the operator refurbishes their unit to bring it back to as-new and a new resident moves in. Once the operator has the incoming resident’s capital payment, the outgoing resident is re-paid their original capital sum less a Deferred Management Fee (DMF) that, amongst other things, is the operator’s return on investment.

This graphic illustrates the model. The resident’s capital sum is protected in the retirement villages legislation and their right to live in the village protected by contract. The consumer protection balances residents’ rights with operators’ duties and responsibilities. The key detail in this model, which enables the operator to make the promises outlined earlier, is that the resident has no ownership interest in their unit or the village, and is therefore protected from the vicissitudes of property ownership – insurance, taxes, repairs and maintenance, and so forth. For many older people, the release from the responsibilities of owning property is a major reason to move.

It’s worth noting that while 70% of villages fix their weekly fee that covers the overheads and day-to-day operation of the village, the costs the fee covers continue to increase even if the income from the fee doesn’t increase. This means that the operator directly cross-subsidizes the residents’ day-to-day overheads from the deferred management fee and any gains in re-licensing the units. Only a retirement village offers this level of financial security for older people.

Another important reason to move is the release of equity in their family home. Retirement villages charge around 70% of the average freehold selling price in the area where they’re built, which allows a resident to sell their home, move to a village and often have substantial amounts of equity to add to their retirement savings. This can make a substantial improvement in the quality of their retirement and allows them to do things they’ve always wanted to but couldn’t afford.

Where an aged care facility is part of the village, the residents get first call on a bed over someone in the community, should they need one. Over the last 10 years or so the only care facilities built have been part of a retirement village, and often the cost of providing care is cross-subsidised by the revenue (and profit) from the village. This pathway to care is another important consideration for older people, and is a key benefit offered by a village.

With the demographics on our side, the retirement village sector has a lot going for it. However, with the governing Act now 20 years old, there are calls for its review, and some stakeholders maintain there’s an imbalance of power; the operators call the shots and residents have to take it or leave it.

In fact, the regulations encourage the development of a very flexible business models that allow residents to chose from a variety of options – price, service levels, DMF rates, sharing capital gains, and so forth.

The government has been reviewing the legislation and recently announced that they would focus on just three issues – the treatment of repairs and maintenance, a review of the complaints and disputes regime, and encouraging operators to refund residents capital sums sooner once they move out.

Operators are relaxed about these reforms, provided the latter doesn’t result in mandatory buybacks and the financial risks that accompany such a move. However, the proposed changes reflect innovations the RVA has already led so most operators have them well in hand.

Possible learnings for the UK

The Older Peoples’ Housing Taskforce recently released their report into an extensive study of how older people might have more choice about where they live. Recommendation Five notes the need for homes that have good age-appropriate design, are affordable, are close to where the intending resident lives and yet are attractive to housing developers.

The Taskforce’s Recommendation Eight notes the importance of offering a range of different housing types with a clear understanding of fees and costs. Their “4 Key Messages” of “Think Housing, Address Ageing, Promote Well-being and provide Inclusive Communities” are at the heart of the NZ retirement village model.

You can access the Taskforce’s report here

Retirement villages are spread across the entire country – cities to provincial and rural towns. The business model works well anywhere, provided residents have the capital sum (and even that is negotiable). Retirement village operators are also the country’s largest home builders and the Retirement Villages Association estimates that around 5,500 family homes are released annually back into the housing market. Villages are significant contributors to easing the chronic housing shortage.

The financial security villages offer residents means a significant improvement in their well-being, general health, and personal sense of security. However, only villages can offer this because the operators continue to own the land and buildings and are responsible for their maintenance and upkeep. Specialist legislation to protect residents’ and operators’ interests is an effective way to allow villages to be built, but it’s essential that the legislation is sufficiently flexible to allow different business models to evolve as the market matures.

Appendix G in the Housing Taskforce’s report includes an outline of the consumer protections in the NZ retirement village-specific legislation. It’s worth noting that this legislation was passed by the Clark Labour Government in 2003 and has generally stood the test of time well.

The transition to care is incredibly stressful for both the resident and their family. If care is part of the village package, the stress can be much less and the transition to care is effectively seamless.

Ultimately, villages work because the residents themselves have a vested interest in making them work. Villages that are resident-led (residents manage and run the activities rather than activity co-ordinators employed by the operator) tend to be more successful, popular and encourage new people to move in.

For more detailed information about the NZ Retirement Villages sector, see the RVA’s response to the Retirement Commission’s White Paper for a legislative review.