We don’t need to recite statistics to know that young people are struggling to afford to even rent the housing they need, let alone buy it. The root cause of the problem is that over the last thirty years house prices have risen faster than earnings. To break out of it we need a sustained period during which the cost of housing (to buy or rent) increases by less than people’s earnings.

The price of land

Land for housing ranges from between 47 times its agricultural value in the East Midlands to 163 times in the south-east, and more around major cities. What drives the price of land? There are two distinct factors. The first is its ‘existing use value’ based on the net revenues it generates. The second is known as the ‘hope value’ – the potential increase in value from any more profitable use it might have, dependent on potential changes in its planning status.

The combination of these gives its speculative value, driving the price at which developers compete to purchase it.

Prior to the early seventies compensation to landowners in a compulsory purchase was based on the land’s ‘existing use value’ plus an incentive to sell of typically between 15% and 20%. The judgement in a court case in 1970 entitled the landowner to the full benefit of the ‘hope value’.[i]

During the thirty years after the war New Town Corporations developed more than 30 ‘New Towns’, providing homes for 2.8 million people, and councils funded the replacement of bomb-damaged housing and slum clearance, using compulsory purchase. The developed housing was worth more than it cost to buy the land and build the homes, roads, schools and other infrastructure. It was done at no cost to the treasury beyond meeting the cash flow requirements through borrowing which the resultant revenues were more than sufficient to repay. The capture of ‘hope value’ by landowners brought that to a halt. The price of building sites and consequently the cost of new development spiralled upwards, while the number of new homes plummeted.

This was one of three factors that lead to a tripling of house prices during the seventies. The others were changes in the way property was taxed, aimed at promoting homeownership which was seen as aspirational, and the lifting of restrictions on borrowing.

Taxation of housing

Until the sixties homeowners were taxed each year on the notional rental value of their home.[ii] They could offset the interest on their mortgage against it, so those with a large loan paid little if any. The tax gradually increased as rents rose and loan repayments reduced the interest payments offset against it. The exclusion of an owner’s main residence introduced in 1963 meant rented housing became more heavily taxed than homeownership despite owners being generally better off than tenants.

A similar exemption was extended to Capital Gains Tax when that was introduced in 1965. When a home is sold the buyer pays stamp duty while the capital gain from the increase in its value is untaxed, unlike the sale of any other asset. That untaxed wealth either raises the inheritance we pass on to our beneficiaries, or inflates prices higher up the housing ladder. At the very least stamp duty which discourages mobility should be abolished, replacing it with capital gains tax which would be unaffected by how often properties are sold. While both taxes are triggered by a sale, no matter how many times a property changes hands the tax taken on the capital gain would stay the same, based on the rise in value, while the amount collected in stamp duty goes up with every change in ownership.

The enhanced financial benefits of owning over renting meant that my generation did anything we could to get onto the housing ladder. The struggle was worth it. In a competitive housing market, the only limitation on how much we paid was the amount we could borrow. Lending restrictions were eased at around the same time and house prices boomed. We became ‘the boomer generation’.

Finance for home ownership

Previously, the funds that building societies could lend were limited by the saving deposits they received. Mortgages were restricted to three times a husband’s earnings plus half a wife’s. They had to be married to get it. The most a household could borrow was 75% of a property’s value, with a retention against any major repairs required to ensure that it was in good condition. The growth in house prices was limited by the loan finance available.

At the end of the seventies, the mortgage market was opened up to banks which raised additional funding from the bond markets and were less restrained in their lending. Within a generation a couple buying for the first time could borrow 90% of the value of a home on more than four times their joint incomes.

Deregulation of banking in the ten years leading up to the financial crash of 2009 increased access to global capital enabling unprecedented growth in house prices relative to earnings.

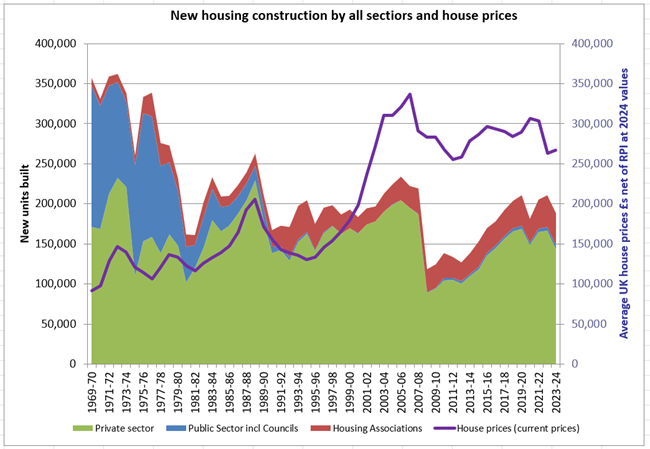

The housing market failed to respond as a healthy market should, by increasing the supply of housing to meet the growing demand. If more is invested in housing than is spent on construction and renovation, house prices inevitably rise. The volume of housing being built fell in the seventies and again following the banking crisis and has never recovered since.

ONS UK Housebuilding and Nationwide House Prices since 1952

My generation’s contribution

I am part of the baby boomer generation, living rent free in a home which I own outright, having paid off my mortgage. Our generation is living longer and hanging onto large family homes with spare bedrooms while our grandchildren live in overcrowded properties. The government taxes mobility through stamp duty, while discouraging us from downsizing by discounting up to £1 million in inheritance tax on the value of our homes when we die.

Very little of the wealth my generation enjoys came from savings on earned income. Most of it is in our homes, which increased in value by far more than we paid to buy them including every penny we spent in interest on our mortgages. Over the last fifty years house prices rose at 1.6% pa more than the rate of interest we paid.[iii]

Buying a home became a cashflow problem. It may have been a struggle meeting the costs but has been extraordinarily profitable for anyone who could raise enough to get onto the housing ladder. Homeowners profit by living rent free with an asset the value of which rises year by year.

By the time our children inherit from us they may be in their sixties with their own children becoming adults. It will arrive too late to help meet the growing housing needs of their family. For some, it will make sense to rent out a house they inherit and do not need rather than sell it.

A home is the only investment where the benefits are tax free. Tax should be levied in relation to our ability to pay. Yet the housing costs of anyone who has owned their home for a few years are far lower than those who are renting, and since the mid-sixties none of that additional consumer spending power has been taxed. Most would be outraged at the thought that it might be.

The value of housing for rent derives from future rental revenues making growth of the private rental market less depended on rising property prices. Stimulating a stronger rental sector while improving tenancy terms would take some of the heat out of the housing market.

The policies Labour is introducing are undoubtedly a step in the right direction but to tackle the fundamental problems making housing unaffordable to some whilst enormously profitable to others they need to go further. Developers will only build extra homes if there are sufficient buyers able to afford prices that make it profitable, and pause when prices fall. To achieve anything like the target of 1.5 million homes a large proportion of them will need to be for private rent supplying those unable to afford homeownership, and social housing funded by capturing hope value for the benefit of the community.

See https://redbrickblog.co.uk for informed debate on Labour’s housing policies. In particular see https://redbrickblog.co.uk/2019/03/evidence-to-affordable-housing-commission/ and https://redbrickblog.co.uk/2018/07/part-2-the-capture-of-hope/

[i] Under the 1961 Land Compensation Act. The case was brought be a landowner in a dispute over the compulsory purchase of land for the Milton Keynes New Town. 1970 Bernard Myers vs Milton Keynes Development Corporation

[ii] Schedule ‘A’ tax

[iii] House prices rose more than mortgage interest rates in 30 of the last 50 years, and by a median margin of 1.6% (Nationwide & BoE)