Some weeks there are just too many interesting things to read, and my highlights this week were a report from Shelter on the use of viability assessments in housebuilding and a blog from the Resolution Foundation on impact of Help to Buy. Both show how poorly-designed policies are pushing up prices and making homes even less affordable.

The Shelter report, by Rose Grayston, ‘Slipping through the Loophole’, based on original research, looks at the ways in which the provision of affordable homes in new development has been undermined since new planning rules were introduced in 2012.

The rules allowed developers to reduce the amount of community benefit they are required to produce as part of a development scheme if their profits are estimated to fall below 20%. (Yes, 20%, sound like a good rake-in for anyone, but this is the minimum figure seen to be competitive in the 2012 rules). As Shelter says, the system ‘rewards developers who overpay for land to guarantee they win sites, safe in the knowledge they will be able to argue down community benefits to make their money back later’.

Shelter calls for the government to amend the national planning rules to limit such assessments to defined genuinely exceptional cases. Certainty about the required number of affordable homes will, they say, become part of the normal cost of doing business. Developers will still make good returns but there will be a downward pressure in the system on land prices. The change would not require any additional public money.

Between 2012-13 and 2015-16 so-called ‘section 106′ planning obligation agreements delivered 38% of the new affordable homes built in England, an average of 17,000 homes a year, around 10,000 homes a year fewer than the previous four years – a period which also included the global financial crash and recession.

Shelter’s research covered 11 council areas around the country. Where viability assessments were deployed, new sites produced just 7% affordable housing, on average 79% below the levels required by the policies of the councils concerned. Viability assessments were used in half of all the developments in the study – but they were skewed towards bigger developers on bigger sites, with small and medium sized developers much less likely to deploy the technique. Councils varied in their policies to resist viability assessments, and it is hard for councils to compete with the large resources some developers can muster to prepare the assessments in the first place. There are often lengthy and costly negotiations. Assessments have generally been confidential and therefore not open to scrutiny by bodies outside the council, especially campaigning groups.

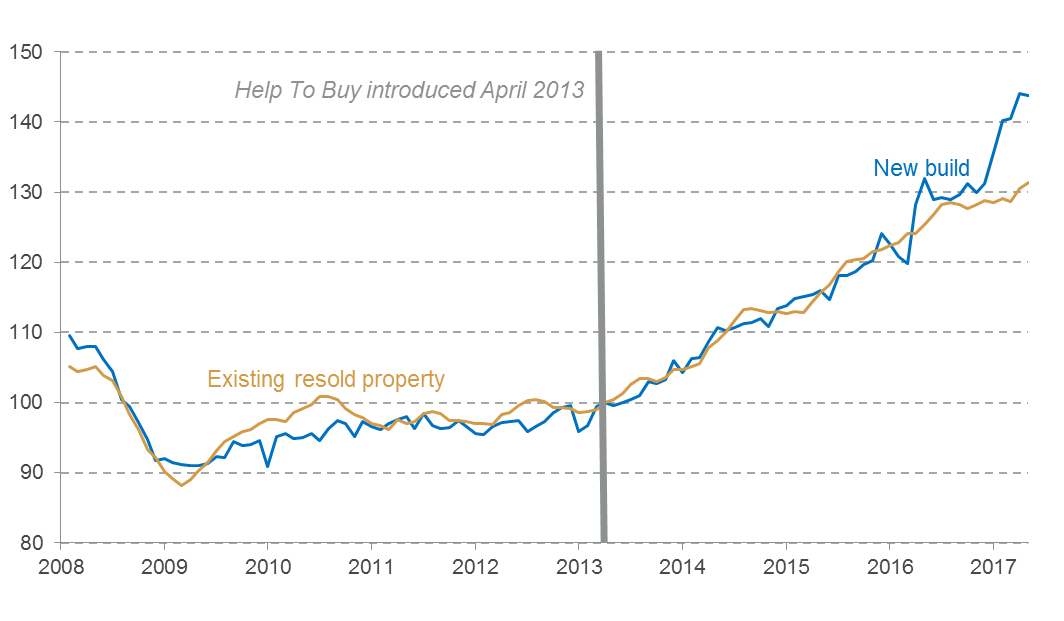

The Resolution Foundation blog, by Lindsay Judge, called ‘Helping or Hindering? The latest on Help to Buy’ assesses the impact of the ‘Help to Buy’ scheme following the government’s announcement that it would put another £10 billion into the scheme. Supposedly designed to help people fulfil their dream of home ownership. Lindsay asks ‘is this expensive policy really doing people any favours?

HTB was introduced in 2013 when the housing market was weak. By offering buyers additional help it was intended to bolster supply by more effectively guaranteeing that developers would be able to sell new homes to someone. ‘Four years on’, says Lindsay, ‘the real world effects…. are plain to see’. In particular, the risk that the policy would actually stoke prices ‘has come to pass’. Worse, ‘the HTB discount is being ‘baked in’ to the price of new properties by developers’. One indicator is that the price of new homes is inflating significantly faster than the price of existing homes when they are resold (see chart). The policy is also not well targeted and has a lot of ‘deadweight’ – that is, it is used by people who could have bought a home without the subsidy – estimated even by the DCLG to be 35%. Some people with incomes over £100k have used the scheme.

House price index by type of build (April 2013=100): England Source: RF analysis of ONS house price index (graph taken from Resolution Foundation Lindsay Judge blog) HTB now takes 45% of the national housing spend in 2016-17. So, why does government do this? HTB of course is not the same type of money as spending on housing grant for affordable homes. It is a loan not a grant. As Lindsay explains, just like student loans, it shows up in the government accounts as a debt but not as part of the deficit. It is a smoke and mirrors policy to be seen to be doing something about declining home ownership, offering people who are struggling to buy now some help – but at the expense of those following later who will have to pay more as a result.

HTB now takes 45% of the national housing spend in 2016-17. So, why does government do this? HTB of course is not the same type of money as spending on housing grant for affordable homes. It is a loan not a grant. As Lindsay explains, just like student loans, it shows up in the government accounts as a debt but not as part of the deficit. It is a smoke and mirrors policy to be seen to be doing something about declining home ownership, offering people who are struggling to buy now some help – but at the expense of those following later who will have to pay more as a result.

If HTB is not in the long term a subsidy for home owners, who have to repay, it is a subsidy for developers who get the sum in cash when a HTB home is bought. It directly enables them to put their prices up, so the policy itself become self-defeating in the medium term.

£10 billion would build something like 125,000 social homes. That option might be an evil in the eyes of the Treasury, says Lindsay, ‘but it would be a far greater good than HTB from a living standards point of view’.

Looking after developers and landowners is the underlying theme of both policies. But with the government now in retreat on many fronts, and even starting to concede the case on the importance of social housing, new campaigning opportunities are beginning to emerge.

(amended 4/11/2017 to correct bad link to Shelter report).

One reply on “Land and house prices – the Tories are getting it so wrong”

Reblogged this on nearlydead.